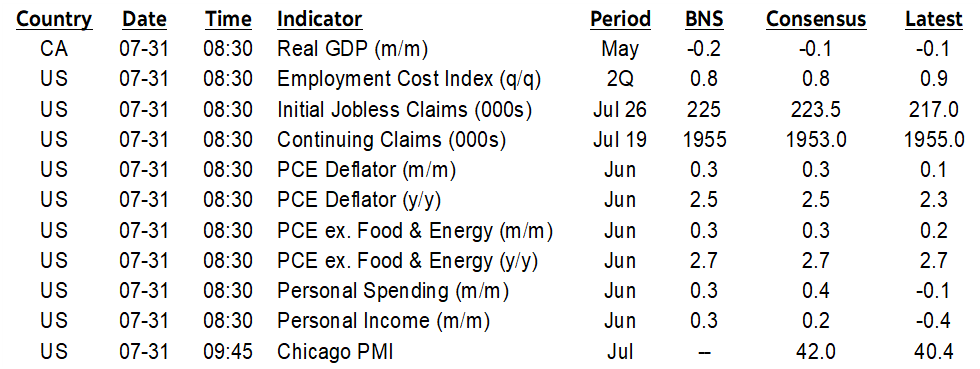

ON DECK FOR THURSDAY, JULY 31

KEY POINTS:

- US equities power ahead as earnings matter more than the Fed

- Carney, Trump downplay trade deal prospects

- Another day, another Trump deal that hits Americans in the pocketbook

- Canadian GDP: Did a soft Q2 end on a firmer note?

- US core PCE could be a warm one

- 62k US layoffs in July are not a nonfarm killer

- Eurozone inflation faces upside risk

- BoJ stands pat, let’s forecasts do the talking

- BCB on indefinite hold

- China’s PMIs indicate softer growth

- US to update ECI, claims

- BanRep and SARB to cut

US equity futures are leading the way with a gain of nearly 1% by the S&P and over 1% for Nasdaq futures partly due to after-market earnings from companies like Microsoft and Meta. Canadian equity futures are flat and European cash markets are mixed but flat on average. There is little follow-through on yesterday’s FOMC and BoC decision as global sovereign yield benchmarks are little changed and the USD is mixed. Frankly, Chair Powell is spot on in terms of conducting monetary policy and is the consummate professional against extraordinarily unprofessional attacks.

This morning’s markets are digesting some firmness in Eurozone inflation readings and BoJ forecasts that hardly abandoned a hike bias at some point distant from current turmoil. The main items on tap for today are GDP figures from Canada and the Fed’s preferred inflation reading for June.

TRUMP AND CARNEY DOWNPLAY ODDS OF A CANADA DEAL

Trump is weaponizing tariffs and trade policy for political purposes again. This time it’s Canada. Again. His overnight social media post said “Wow! Canada has just announced that it is backing statehood for Palestine. That will make it very hard for us to make a Trade Deal with them. Oh’ Canada!!!” Whatever one thinks of Middle East politics—and I’ll keep my views to myself—this is a matter for a sovereign nation like Canada to decide. Canada isn’t alone either, as it has joined the UK and France in recognizing a Palestinian state in September at the UN General Assembly.

Canadian PM Carney’s other recent comments have generally doused expectations for a trade deal with the US by tomorrow’s US-imposed deadline even before the Palestinian issue. Did statehood recognition scuttle a trade deal or did a scuttled trade deal lose support of an ally on a matter of foreign relations?

TRUMP’S ‘DEAL’ WITH SOUTH KOREA HITS AMERICAN POCKETBOOKS

The US and South Korea announced a deal yesterday that imposes a 15% tariff on South Korean imports to the US excluding metals. That will hit American consumers and businesses the same way as other tariffs. The ‘deal’ also sets up a US$350B fund that the US said will be directed by Trump with the US retaining 90% of the profits. Korea’s interpretation is that $150 billion of that fund will be earmarked for shipbuilding, what happens depends upon whether there are attractive investment opportunities which indicates it’s a soft target, and that much of the fund is comprised of loans and guarantees like the Japanese deal. A Korean official said “If the fund delivers promising returns, Korean companies are likely to join as key partners, offering significant opportunities for those looking to enter the U.S. market," all of which makes this investment deal sound like the same loose, over-hyped pledge as the others.

CANADA’S ECONOMY MAY HAVE ENDED Q2 ON A FIRMER NOTE

Canada releases GDP figures this morning (8:30amET). May GDP is estimated to decline by -0.2% m/m SA. Consensus reflects Statcan’s initial guidance of -0.1% m/m SA that was provided a month ago. More important will be the initial flash reading for June that only provides the headline estimate sans details. Limited readings suggest June may have rebounded. Hours worked were up by a large 0.5% m/m and since GDP is hours times labour productivity this gives a bit of a running head start at the estimate. While not based on value-added GDP concepts, other readings also point to strength. Housing starts were slightly higher. Retail sales rebounded with volumes probably up by around 1% m/m or more. Manufacturing volumes were probably flat. The election distortions in April and May will have shaken out of the June figures, while weather was likely more of a support to seasonal activities in June than in May.

US CORE PCE COULD BE WARM

We get the June PCE estimates of US inflation this morning (8:30amET). Most forecasters had estimated a rise of 0.3% m/m SA for core PCE before yesterday’s Q2 figures that landed at 2.5% q/q SAAR. Some shops that were lower than consensus for June submitted higher forecast revisions yesterday after seeing the Q2 figures. Why? Because if there are no revisions to prior months, then 2.5% core PCE in Q2 implies June core PCE at about +0.4% m/m SA. There may, however, be revisions to prior months such that June might not be as high as that. So, some combination of revisions and/or firmer core PCE than core CPI may reveal warmer monthly readings.

US consumption may have outpaced incomes in June, pushing the saving rate lower in this morning’s June refresh (8:30amET).

Challenger mass layoffs landed at 62k in July, up from 48k in June but the figures are not seasonally adjusted. They remain well off the unadjusted peaks earlier in the year when 275k layoffs occurred in March (chart 1).

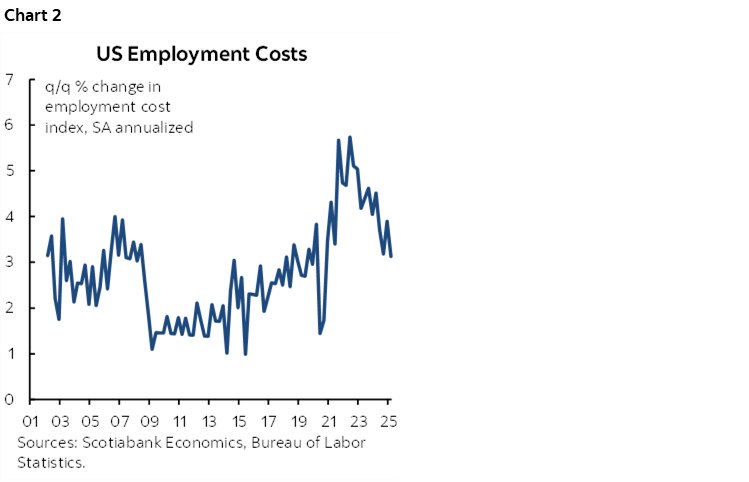

The Employment Cost Index for Q2 (8:30amET) could continue to hover around sub-1% q/q SA gains and hence extend the pattern (chart 2), and initial jobless claims will also be refreshed (8:30amET).

EUROZONE CPI IS LOOKING FIRMER THAN EXPECTED

Eurozone inflation readings are motivating slight underperformance across shorter-dated EGBs and mild outperformance of the euro. They suggest there may be upside risk to the -0.1% m/m consensus estimate for tomorrow’s Eurozone CPI reading.

- German states registered inflation readings that suggest upside risk to the national print that arrives a little later this morning (8amET). The individual states reported CPI to be up by 0.2 –0.4% m/m with most at 0.3% compared to the non-harmonized consensus estimate of 0.2% for the national total and the EU-harmonized estimates of 0.4%.

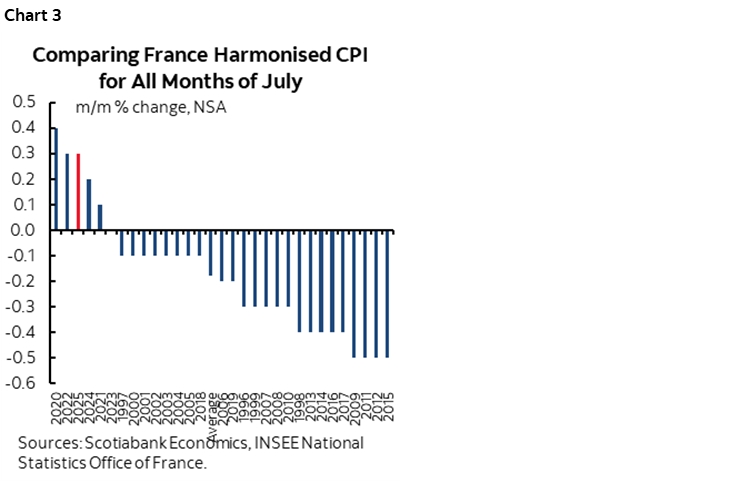

- French CPI was up 0.3% m/m (0.2% consensus) on an EU-harmonized basis. The seasonally unadjusted m/m change was among the hottest in history comparing like months of July (since it’s unadjusted) as shown in chart 3.

- Italian CPI registered a slightly softer drop than expected at -1% m/m (-1.1% consensus) on a harmonized basis.

- Recall that Spain had already released yesterday and reported CPI at -0.1% m/m NSA (-0.4% consensus) with core CPI hotter than a usual month of July when comparing like months for seasonally unadjusted data.

CHINA’S PMIS INDICATE A SLIGHTLY SOFTER ECONOMY

China’s state PMIs were little changed. The composite slipped half a point to 50.2 because both the manufacturing (49.3, 49.7 prior) and non-manufacturing (50.1, 50.5 prior) PMIs declined a touch.

BOJ HELD, LET’S FORECASTS DO THE TALKING

The Bank of Japan held its target rate unchanged at 0.5% as widely expected but let its forecasts do the talking by way of staying on track for eventually further tightening. The core CPI forecast was raised half a point for this year to 2.7%, a tenth to 1.8% for next year and a tenth to 2% for the year after.

BCB SIGNALS INDEFINITE HOLD

Brazil’s central bank held its Selic Rate unchanged at 15% as widely expected last night. The statement referenced a potential hold for “a very prolonged period” as the bank also addresses the consequences of the trade war with the US that is interfering in domestic politics.

TWO MORE RATE CUTS COMING TODAY

Both SARB (9amET) and BanRep (2pmET) are expected to cut by 25bps today. See my week ahead for more on them and the rest.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.