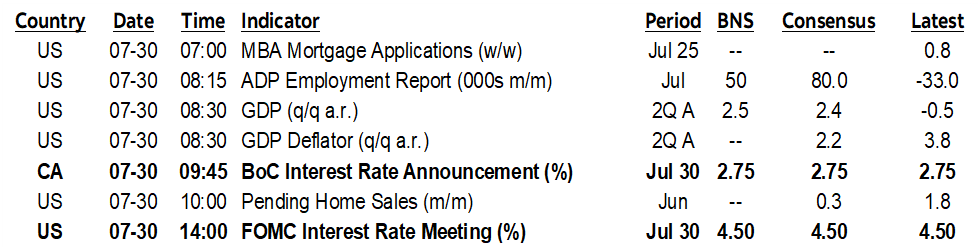

ON DECK FOR WEDNESDAY, JULY 30

KEY POINTS:

- Markets brace for tariffs, key central banks, top shelf data

- Trump may react to China briefing today

- BoC to hold, remain agnostic on its four key issues

- FOMC to hold, don’t expect a September tee-up

- ADP payrolls unlikely to sway nonfarm expectations

- US Q2 GDP growth likely to be resilient, watch domestic demand

- RBA cut in August cemented by soft Q2 CPI

- BCCh cut, guided more to come

- Eurozone economy slows, averts a worse outcome for now…

- ...while consumer spending ended the quarter solidly in Germany, France

- Spain’s core inflation was much firmer than usual

- Mexico’s economy may have accelerated in Q2

- Brazil’s central bank expected to remain on hold—and bewildered

Buckle up! Macro risk kicks into high gear today. Potential tariff headlines, key indicators and key central banks all chime in to shape a potentially volatile market session.

Current market positioning may be meaningless by the time we get through it all, but at present, the mood across asset classes is cautious. Stocks are mixed with US and Canadian futures up a bit, while European cash markets are split between a dip in London and Spain, but gains elsewhere. Sovereign bonds are mostly little changed with notable exceptions including outperformance of gilts following a solid 2052 auction and strong bid-to-cover, and the Australian and NZ curves after Aussie CPI was softer than expected. The dollar is mixed against the majors.

TRUMP’S REACTION TO CHINA NEGOTIATIONS

Off-calendar risk may include Trump’s response to the proposed 90-day tariff extension for China that Bessent advocates once he’s fully briefed. Will he accept it or will risk flare? Rationality would suggest not escalating tariff risks before a Fed decision, but...

The main events, however, will be the BoC and then the FOMC previewed here.

BANK OF CANADA—JURY STILL OUT ON THEIR TOP FOUR ISSUES

The BoC offers a full suite of communications this morning. The statement appears at 9:45amET along with the July Monetary Policy Report. Governor Macklem and SDG Rogers deliver their press conference forty-five minutes later that will last for up to about an hour.

Key for the BoC will be whether they have any confidence to tip toe back toward the forecasting business and hence implied guidance of some form or stick to scenarios with an ongoing lack of confidence on core issues like the evolution of trade and fiscal policies. I think the latter is more likely.

The statement is likely to repeat the following paragraph that outlines the four things the BoC is focusing upon and their interpretation of how these matters are tracking is likely to remain cautious:

“Governing Council is proceeding carefully, with particular attention to the risks and uncertainties facing the Canadian economy. These include: the extent to which higher US tariffs reduce demand for Canadian exports; how much this spills over into business investment, employment and household spending; how much and how quickly cost increases are passed on to consumer prices; and how inflation expectations evolve.”

On #1 (whether higher tariffs have reduced demand for Canadian exports), the jury is somewhat out thus far. Export volumes are tracking a large 33% q/q SAAR drop in Q2 after gains of about 10% in each of 2024Q4 and 2025Q1. It’s entirely plausible that exports will suffer, but the pulled forward tariff-avoiding behaviour and the ensuing payback requires more data in a cleaner period in order to assess the pattern.

On #2, it’s certainly not spilling over negatively into employment especially given the blow out June reading. Household spending measured by the higher frequent retail sales report is tracking a volume gain of over 2% q/q SAAR which isn’t fantastic but is hardly collapsing and excludes services that are probably performing better. Investment measured by capital goods imports that dominate investment spending was up by 29% q/q SAAR in Q1 and is tracking a similar decline in Q2 on pulled forward effects; more data is needed here too in order to be comfortable with the trend as opposed to the distorted tariff-avoidance effects.

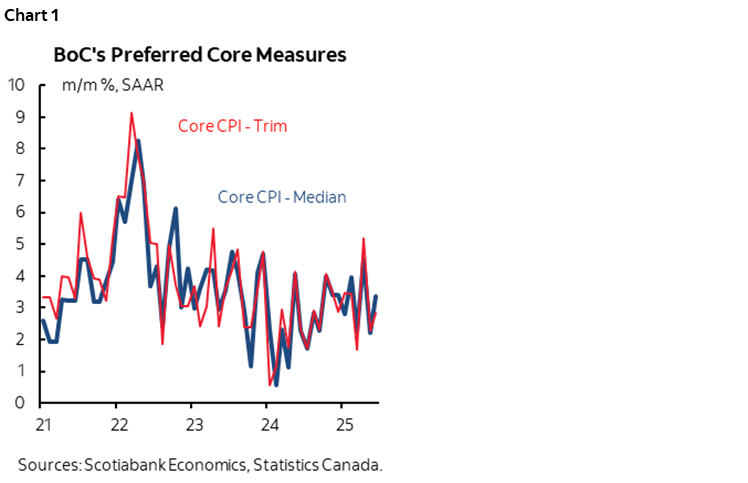

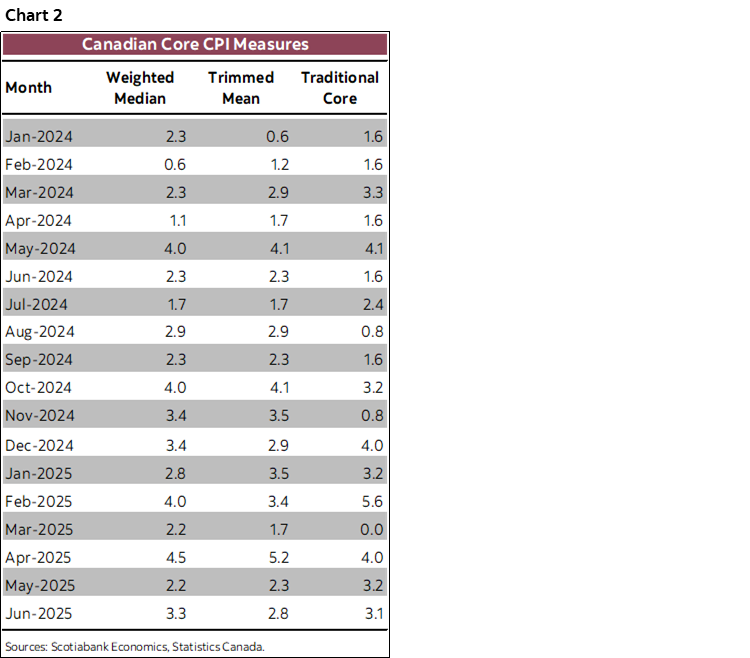

On #3 that flags the speed and magnitude of cost increases being passed on to consumer prices, I think they’ll remain concerned about the trend in core inflation readings (chart 1). Chart 2 shows the numbers for core inflation readings in m/m SAAR terms. Disaggregating the influences upon prices is difficult, but the BoC has been faced with sticky, high core inflation readings on a m/m SAAR basis for a year-and-a-half despite the emergence of a negative output gap 8–10 quarters ago (depending upon the measure that is used).

On #4, the evidence is mixed and the data is woefully stale. The BoC’s surveys showed some improvement in business expectations of future inflation, but no improvement among consumers.

FOMC TO REMAIN PATIENT

The FOMC is a statement-only affair at 2pmET with Chair Powell’s press conference at 2:30pmET. A hold is universally expected and priced. There will be no Summary of Economic Projections and dot plot with this one as they were provided at the June meeting and Chair Powell is likely to remain comfortable with how those views are tracking now.

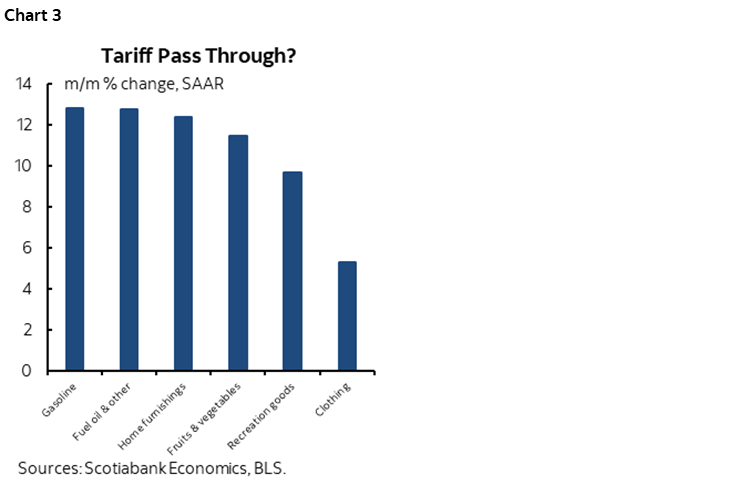

Watch for possible dissenters (Waller, Bowman?), and gauge how patient sounding Powell is during his presser. I doubt very much that we’ll hear any hint of a tee-up for September with language such as how it may be appropriate to ease somewhat soon, or soon, not least of which given that there are seven weeks before the next decision on September 17th and hence a lot of potential developments and key data. Instead, expect Powell to remain patient, hopefully referencing solid GDP growth this morning, resilient payrolls, and early signs of tariff pass through in some CPI components (chart 3).

Further, the debate over how trade, fiscal, immigration and regulatory policies may affect the Fed’s dual mandate going forward remains open. The nature of these shocks creates a potential quandary for the Fed in that, for instance, protectionist policies may raise unemployment and inflation simultaneously. Easier monetary policy may be appropriate if growth and the job market sag, but not necessarily if inflation surges. The balance between the two effects and how durable the effects may be will determine appropriate policy actions. Until we have the data over an extended period it may not be advisable to alter course.

That pivots toward the September 17th FOMC meeting and subsequent ones. Multiple rounds of inflation and job market data may be required alongside greater policy clarity and more consistency from the Trump administration. Should tariff pass-through into inflation increase over coming months, then the optics of easing in that environment may be too much to allow the Fed to ease unless payrolls begin falling. The FOMC could easily say that it may take much longer than ‘months’ to be comfortable with the evidence.

RBA CUT CEMENTED BY SOFTER CPI

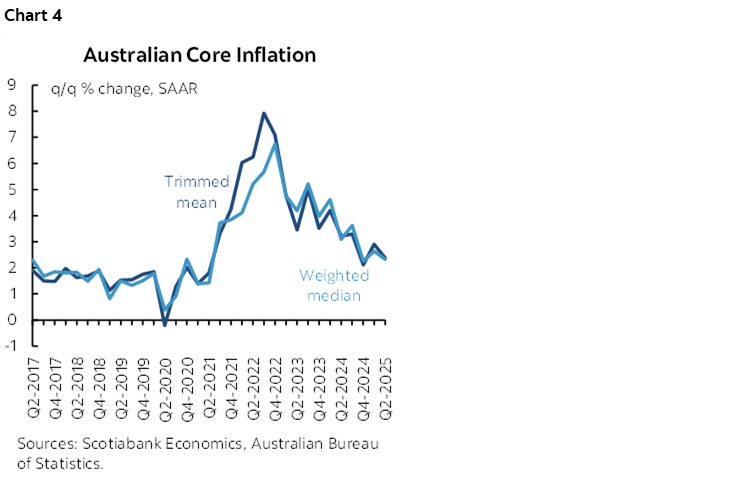

The A$ is underperforming all other majors and the Aussie rates curve is outperforming all other global curves after CPI came in weaker than expected. Headline CPI landed a tick beneath expectations at 0.7% q/q SA nonannualized with trimmed mean at 0.6% (0.7% consensus) and weighted median CPI on the screws at 0.6% (chart 4). June’s monthly measures decelerated even more to 1.9% y/y with trimmed mean down three-tenths to 2.1%. Markets are fully pricing an RBA cut on August 12th and over 75bps of cuts by about this time next year.

BCCH CUT 25BPS

Chile’s central bank cut by 25bps as widely expected last evening. The decision was unanimous and guidance noted that the overnight rate is expected to approach neutral over coming quarters.

EUROZONE GDP AVERTS A WORSE OUTCOME

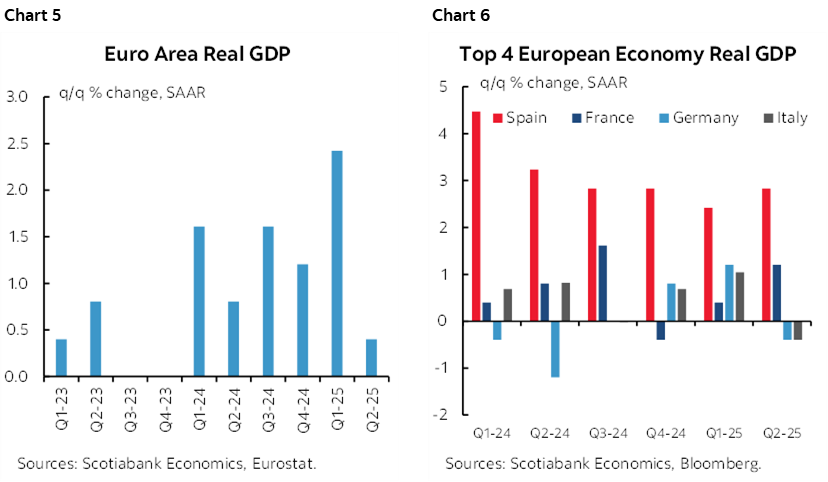

Eurozone GDP barely stayed on the plus side at 0.1% q/q SA nonannualized in Q2 (0% consensus). Germany’s economy shrank by -0.1% and so did Italy’s, but France beat expectations at 0.3% and so did Spain at 0.7%. Still, Eurozone GDP growth was its weakest since 2023Q3 (charts 5, 6).

Also note the evidence on European consumers that signalled a strong running head start into Q3 GDP that nevertheless faces higher risks from uncertainty and tariffs. French consumer spending volumes smashed expectations with a gain of 0.6% m/m SA in June (-0.3% consensus) and German retail sales volumes did likewise in June (+1.0% m/m SA, 0.5% consensus). German figures were extra impressive because of upward revisions that took May’s drop of -1.6% up to just -0.6%, posing what should have been a higher jumping off point making growth in June harder to achieve.

SPAIN FIRST OUT WITH EUROZONE INFLATION SIGNAL

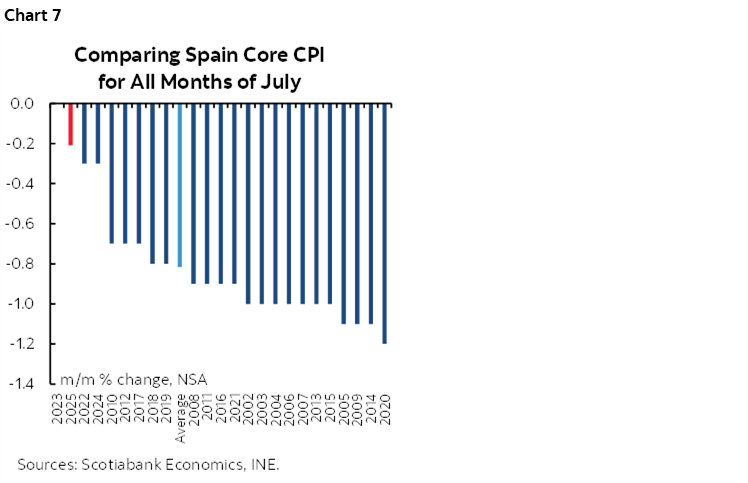

Spain was first out among Eurozone economies with CPI figures for July. On an EU-harmonized basis, CPI matched expectations at -0.4% m/m NSA. However, on the reported seasonally unadjusted basis, core Spanish CPI put in its strongest performance on record comparing all like months of July (chart 7).

US ADP AN UNHELPFUL WARM-UP TO NONFARM

US ADP private payrolls (8:15amET) are expected to be fairly soft again, which may drive a market response even though you’d never use ADP to forecast nonfarm. I went with +50k and consensus is at +76k.

US GDP LIKELY TO BE SOLID

US Q2 GDP (8:30amET) is expected to be resilient this morning but key will be final domestic demand that removes possibly ongoing distortions from imports and inventories and gets at the momentum in the domestic economy. Consensus expects growth at 2.6% q/q SAAR, I’m at 2.5%, and the Atlanta Fed’s nowcast was revised up to 2.9% yesterday on the back of improved goods trade data. Anything even close to those figures—depending on details—would lean against any need for rate cuts by way of input into developments across dual mandate variables.

MEXICO’S ECONOMY COULD ACCELERATE

Mexico’s economy is expected to post mild growth but here too we’ll have to get at underlying details. Consensus expects 0.4% q/q SA nonannualized growth for Q2 (8amET) that would be double the prior quarter’s rate.

BCB TO HOLD

Brazil’s central bank then chimes in with an expected hold this evening (5:30pmET) and a sense of bewilderment ahead of Trump’s 50% tariff threat and potential retaliation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.