ON DECK FOR MONDAY, JULY 28

KEY POINTS:

- Global markets in a very mildly constructive mood…

- ...on US-EU deal and expectations for a jam-packed week

- The US-EU deal: What’s in it, what’s not, and cautions

- The EU deal could’ve been worse, but is definitely not good for the world economy

- Why Japan’s investment commitment to the US is fake

- Deals with China, Canada and Mexico remain elusive

- Global Week Ahead—Return to Sender (reminder here)

A fresh, jam-packed week is so far off to a mildly positive start in financial markets. Equities are gently higher with N.A. futures up by ¼% to ½% in the US and less for TSX futures, and European cash markets are losing initial momentum they had earlier in the European session. The dollar is broadly higher against all major crosses especially the Euro and CHF that are underperforming all others. Sovereign yields are mixed with slight cheapening of the US long end and gilts front end and mild EGB rallies. Oil is up by 1%.

The catalysts may be two-fold. One is that the US-EU trade deal that was announced yesterday wasn’t as bad as it could have been but is still a dark day for global trade. Raising tariffs on US imports is not trade liberalization as the MAGA camp claimed they were out to achieve. What is impossible to disentangle from the deal’s effect on markets, however, is what markets are pricing for the broader week’s expected developments in terms of heavy calendars for earnings, central banks, data, and perhaps further trade deals.

There is nothing else on tap by way of meaningful calendar-based developments. Only the Dallas Fed’s manufacturing index is due out (10:30amET).

THE US-EU DEAL—WHAT’S IN IT, WHAT’S NOT, AND CAUTIONS

This is tentative in part because of conflicting accounts, but here is a list of what the US-EU trade deal appears to include. The EU as a whole is America’s biggest trade partner, but on an individual country basis Canada is the biggest.

- a 15% baseline tariff will apply on most EU goods exports to the US which is the same rate applied to Japan but higher than the 10% rate on the UK. It’s half the rate Trump had threatened by this Friday and much less than the 50% rate he had previously threatened. The lower than feared rate is welcome to markets, but still a negative development for global growth, US import prices, the Federal Reserve’s chances of cutting etc.

- That 15% tariff includes autos and parts that were previously faced with a 27.5% tariff. Since European manufacturers often make higher end luxury cars than American cars and trucks, they’ll likely have more pricing power to pass through tariffs to US consumers. If you’re in the market for, say, a Mercedes, you’re going to pay, or postpone, or prices for good used vehicles will rise.

- Pharmaceuticals and semiconductor chips were excluded for now. Subsequent comments by US officials indicated that the EU rate on pharmaceuticals exports could remain at 15%. The US has pledged to have 232 trade investigations ready by mid-August which will determine tariffs on those items.

- The EU secured 0% exemptions for aircraft and parts and select chemicals, semiconductor equipment, some agricultural items and critical raw materials with the pledge that more products will be added. The EU is pushing for alcohol and spirits to be exempt. We need to reserve judgement on the effective tariff rate being imposed on EU exports to the US until we see the full list of exemptions and details.

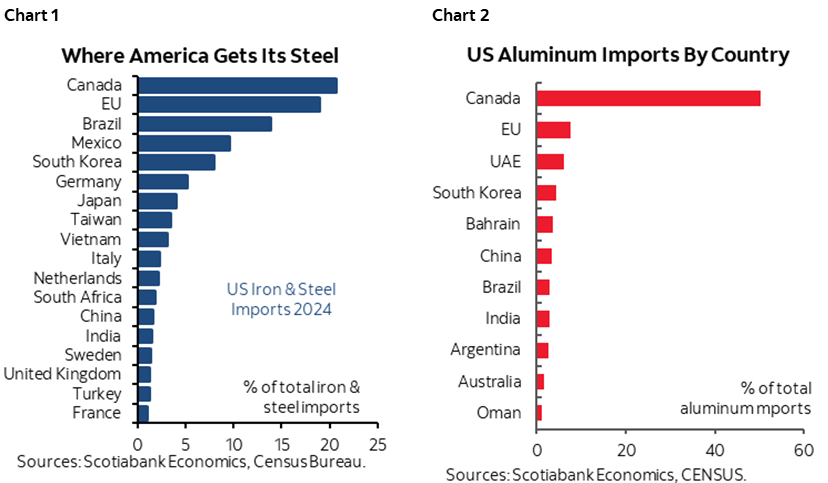

- Metals tariffs against the EU will be left at 50% but may be replaced by quotas later above which stiff tariffs would apply but we don’t have details. The EU is a close second to Canada as a source of US steel imports but a distant second to Canada on aluminum (charts 1, 2).

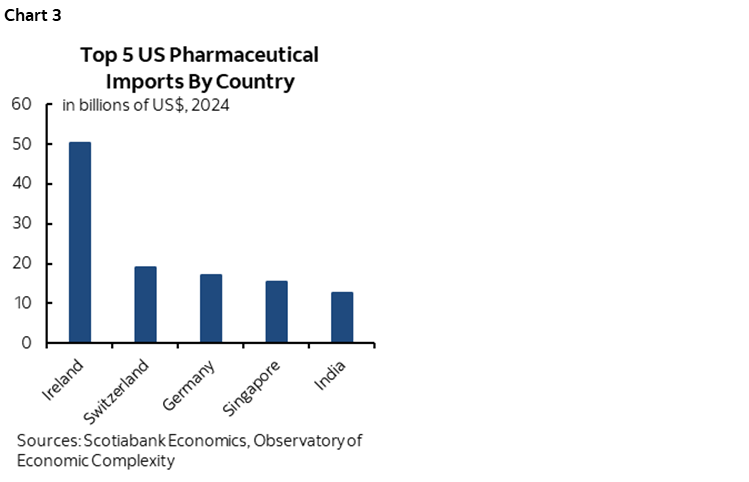

- Where US imports of pharmaceuticals come from is shown in chart 3.

- The EU will purchase US$750B of liquified natural gas, oil and nuclear fuels divided over three years as purchases will substitute away from Russian energy. Watch Russia’s response, such as into winter. And big deal. US$250B of purchases per year sounds big, but it’s from a US$30T US economy which is about 0.8% of US NGDP and it’s unclear what share of that is truly new and what the value-added component is compared to value-added GDP concepts.

- The EU will invest US$600B into the US. What this includes is highly unclear. Some reports say it’s in addition to current flows, while others say it includes private investments already in the pipeline. Some reports say it includes defence items from the US, while others leave the defence component uncertain. The time period, composition etc are all unclear. If it’s like Japan’s “investment” commitment, then it could prove to be as farcical (see Japan section below).

- The US pledge to impose a tariff of 15% relies on the EU lowering tariffs on US imports to 0% and “opening up their countries” as Trump put it, but with unclear details such as on what and the timeframe. The EU previously had very low tariffs on US imports anyway (here). The EU applied about a 1% tariff on most imports of US goods which was similar to the pre-existing US tariff on EU goods imports before Trump took office.

And here are some cautions:

- We don’t have legal text. Ursula von der Leyen said “Details have to be sorted out, and that will happen over the next few weeks.” We may never get formalized legal text with all necessary details.

- with that, we also don’t have implementation details.

- There does not appear to be anything on nontariff barriers that the EU could employ. They could substitute for the small EU tariff reductions on US imports. The EU might say sure we’ll lower your tariffs on US imports by a percentage point, but we’ll make it harder to sell to Europe in other ways such as through stricter health, safety and environmental restrictions.

- Also not mentioned are other US beefs, such as Europe’s VAT taxes, and US opposition to them never made sense anyway.

- What we don’t know is how Europe will respond in more passive terms over time. It may exclude or restrict US firms from procurement programs, for instance.

- Implementation risk may be significant. The EU member states need to approve the deal. The responses from across member states is deeply divided. French PM Bayrou said “It is a dark day when an alliance of free peoples, gathered to affirm their values and defence their interests, resolves to submission.” German chancellor Merz said the deal avoids “needless escalation” but German business groups flagged negative effects while expressing relief that higher tariffs such as 27.5% on auto exports were averted. The Italian left slammed the deal. Dutch foreign minister Boerma expressed the desire to keep negotiating with the US. Hungary’s Orban said von der Leyen was a “featherweight” and the deal amounted to “Donald Trump eating Ursula von der Leyen for breakfast.”

- The value of the US signature on its deals has clearly been eroded under Trump. This may not be the end of the tensions with significant probability that Trump could come after Europe again on something else. The US is a highly unreliable partner.

JAPAN’S INVESTMENT COMMITMENT TO THE U.S. IS A HOAX

Japan’s trade negotiator, Ryosei Akazawa, said today that the US$550 billion fund to invest in the US as part of last week’s trade deal wasn’t investment per se. He said that 1–2% of the amount would be actual investment with the vast bulk of the fund being in the form of loans on which Japan would make interest and fees. Akazawa said that if the loan guarantee components are not triggered, Japan just makes fees and said “For that part, Japan is just making money.” Akazawa also stated the following:

“It’s not that $550 billion in cash will be sent to the US. By letting the US have 90% of the profits rather than 50%, I think Japan’s loss will be at most a couple of tens of billions of yen. People are saying various things, such as ‘You sold out Japan,’ but they’re wrong.”

In other words, the US gained maybe about US$135 million on hypothetical profits as its share.

Akazawa also noted that the US$550B figure won’t only apply to Japanese and US firms and could include companies from other countries.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.