ON DECK FOR FRIDAY, JULY 25

KEY POINTS:

- Markets on cautious footings ahead of jam-packed week

- Tech earnings are not helping

- Soft Tokyo core CPI complicates the BoJ’s stance next week

- UK retail sales disappoint

- Russian central bank cut 200bps

- US core durable goods orders have stalled since inauguration day

Markets are ending the week and transitioning toward a jam-packed coming week on cautious footings. Stocks are mixed but on average little changed. Sovereign yields are up a bit across major global benchmarks. The dollar is gaining against most crosses. There are at best very light developments to consider like Tokyo CPI and UK retail sales that markets didn’t much pay attention to.

WEAK TECH

One is that Intel’s earnings and guidance in yesterday’s after-market went over like a lead balloon. The stock is down by about 6% compared to just before the release and into this morning’s pre-market. Concerns center around the viability of a multi-year turnaround plan that continues to slash payrolls.

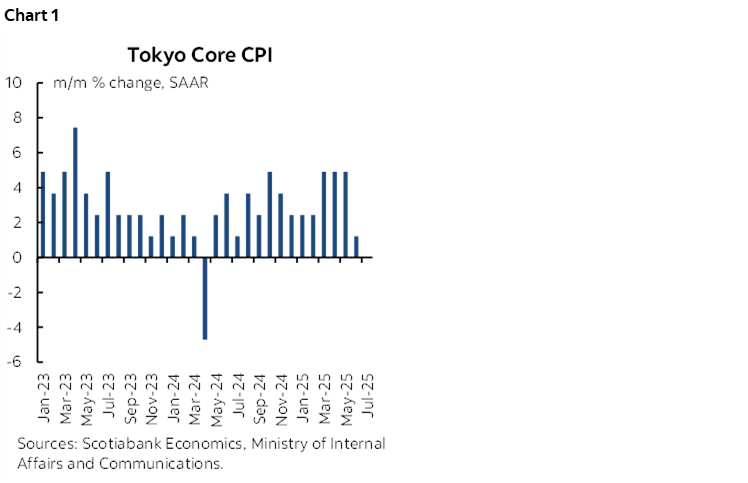

SOFT TOKYO CORE CPI COMPLICATES THE BOJ’S STANCE

The fresh Tokyo measure of core CPI inflation was weak again. July’s reading was flat at 0% m/m SA. That follows a reading of only 0.1% m/m SA in June (chart 1). Is the surge over? Was it temporarily fed by prior peaks in oil prices in 2023–24 plus peak weakness of the yen in 2024? Are Shunto wage gains not really filtering through to more of the workforce than the under 20% of workers who benefit from the union agreement? Perhaps, but the BoJ will need more evidence than two reports as it refreshes forecasts and guidance at next week’s decision when it is expected to remain on hold.

LIGHT EUROPEAN DEVELOPMENTS

UK retail sales disappointed expectations. June’s rise of 0.9% m/m SA was ok, but fell shy of the 1.2% consensus mark and didn’t claw back much of the 2.8% decline the prior month. Sales ex-fuel were up by only 0.6% m/m—half of consensus—and after a 2.9% prior drop.

German IFO business confidence was little changed in July. Nothing to see there.

Russia’s central bank cut its key rate by 200bps in line with consensus expectations.

US EQUIPMENT ORDERS STALLING?

The US updates durable goods orders for the month of June this morning. The volatile headline is expected to drop as the prior surge of aircraft orders won’t repeat. Key, however, will be core orders (ex-defence and air) as a proxy for underlying equipment investment. They too have been hard to read of late with an oscillating pattern of ups and downs since February. To smooth through the noise, we need to look at seasonally adjusted levels. The level of orders had increased in later 2024 into January but has been bobbing along a flat trend since then perhaps as policy uncertainty escalated. There is little cost to postponing investment decisions at least until there is some clarity surrounding erratic and protectionist US trade policies.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.