ON DECK FOR THURSDAY, JULY 24

KEY POINTS:

- Soft equity tone into the ECB, post-PMIs and tech earnings

- Global PMIs signal divergent growth risks

- Canadian retail sales: May was hit by weather, June rebound?

- ‘Mag7’s’ earnings not as magnificent as their collective share prices

- Trump talks up trade ‘deals’ that apply a century-high tax on Americans

- Industry guidance points to a strong gain in US vehicle sales, weak prices

- Fed to come under fire again today

- Won outperforms on GDP beat

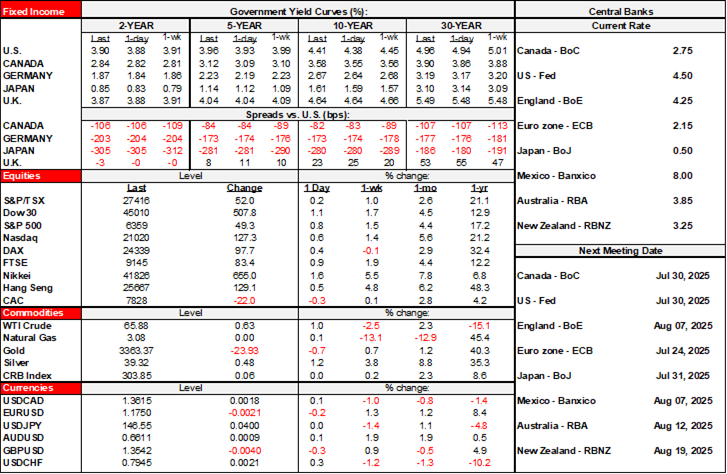

The biggest day of the week for calendar-based risk is upon us but markets are putting in divergent responses thus far. N.A. equity futures are flat, versus mild rallies in most of Europe. Sovereign bonds are slightly cheaper across all global benchmarks. The dollar is mixed as it gains on European crosses but loses ground on some Asia-Pacific benchmarks. Oil is up by a few dimes. PMIs, the ECB, and Canadian consumers are the main highlights by way of fresh developments while ‘Mag7’ earnings were mixed last evening (Alphabet gaining, Tesla not) and Intel releases this evening.

THE LIES ABOUT TRADE LIBERALIZATION

On tariffs, Trump was talking up negotiations with Europe last evening and issued the fact sheet (here) for the US-Japan trade deal that offered no real additional details as my take on it remains unchanged from yesterday morning’s note (here). He also seemed to set 15% as the floor for any country’s tariff rate by saying “We’ll have a straight, simple tariff of anywhere between 15% and 50%” across countries with Brazil at the top end for now.

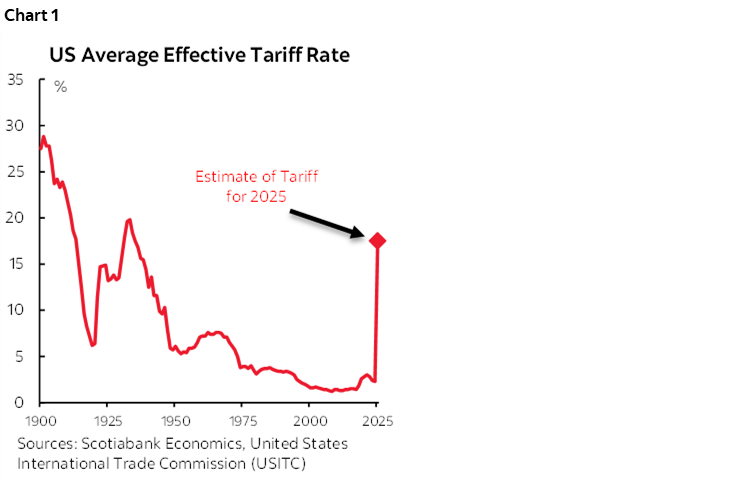

Estimates vary depending upon what you assume by way of further deals, but based on info to date we're figuring that the US effective tariff rate on its own imports now stands at 14.3% on all goods and services, or 17.5% on just goods. That's up from 2.3% on goods before Trump took office in January.

It's a total MAGA lie that this is trade liberalization. Trump has erected a significant protectionist tariff wall around the US economy with complex effects that will unfold over time and that in my opinion markets are not fathoming. The effective tariff rate is at its highest since 1935 (chart 1). It’s a tax on American businesses and American consumers that is designed to pay for income tax cuts that disproportionately go to the relatively wealthy which is regressive economic policy that is bad for long-run growth and living standards.

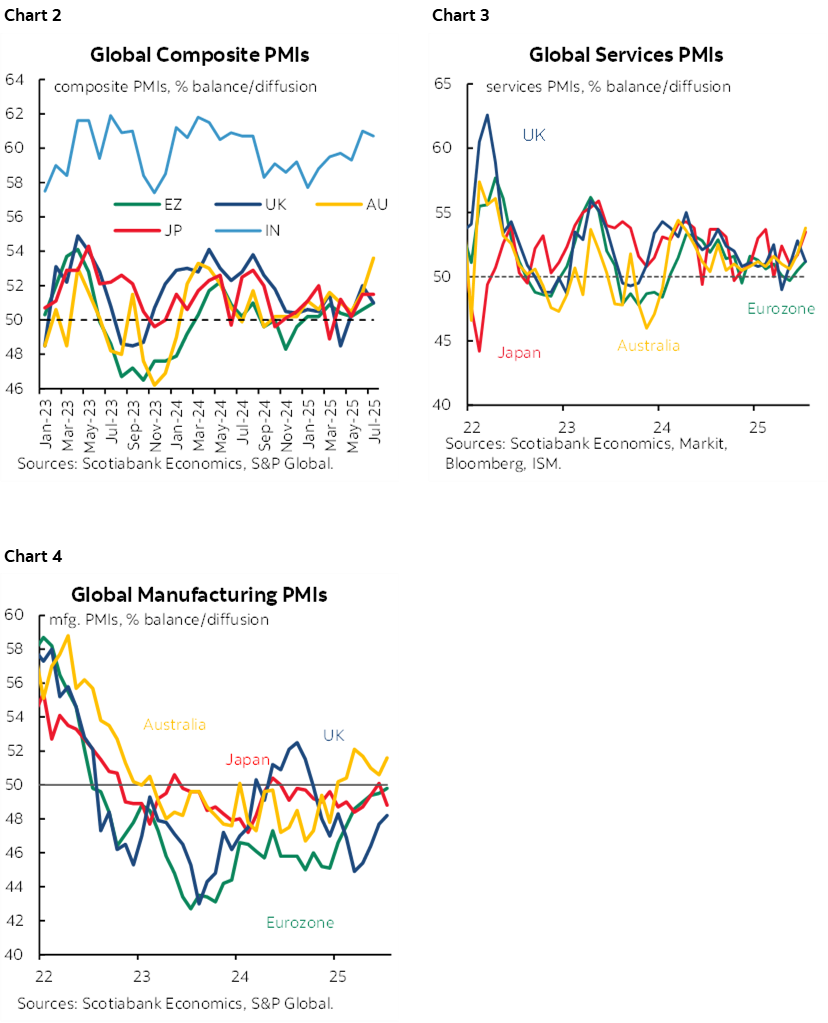

GLOBAL PMIS SIGNAL DIVERGENT GROWTH RISKS

Global purchasing managers indices showcased quicker growth in Australia, slower growth in the UK, and little change in the Eurozone, Japan and India. Charts 2–4 shows the relative patterns.

- Australia: The composite PMI gained two full points to 53.6, furthering the distance from the 50 divide between expansion and contraction. Quicker growth was spread between both services (53.8, 51.8 prior) and manufacturing (51.6, 50.6 prior).

- Japan: There was no change in the mild growth composite reading of 51.5. A gain in services (53.5, 51.7 prior) was offset by a deceleration in manufacturing (48.8, 50.1 prior).

- India: There was no meaningful change in the composite PMI that still signals fairly rapid growth (60.7, 61.0 prior) as services decelerated a touch (59.8, 60.4 prior) and manufacturing picked up a bit (59.2, 58.4 prior).

- Eurozone: The composite was little changed (51.0, 50.6 prior) as services accelerated (51.2, 50.5 prior) and manufacturing was little changed (49.8, 49.5 prior). France remains in slight contraction with Germany in slight expansion.

- UK: The UK composite fell, signalling cooler growth (51.0, 52.0 prior) driven by weaker services (51.2, 52.8 prior) as manufacturing picked up by half a point to 48.2 but remains in contraction.

- US: The US gauges arrive at 9:45amET. They have been signalling moderate growth in the US economy. The US also releases new home sales for June (10amET) that are expected to post a modest rebound from the steep drop in May.

WON OUTPERFORMS ON SOUTH KOREAN GROWTH

South Korea’s Q2 GDP beat expectations (0.6% q/q SA, 0.5% consensus) in a firm rebound from the -0.2% prior contraction. Manufacturing led the way as utilities and construction were drags on growth and services posted moderate growth. The won is the star pupil this morning but the Korean rates curve isn’t performing in a materially different way to other curves.

ECB TO HOLD

Markets are priced for the ECB to hold the deposit rate this morning (8:15amET) and only see most of another cut priced by either the December or February meeting. Consensus also expects a hold. President Lagarde’s guidance may be key in her press conference (8:45amET). She said on June 5th after cutting by 25bps that “We are getting to the end of a monetary-policy cycle that was responding to compounded shocks—including Covid, the illegitimate war in Ukraine and the energy crisis. At the current level of interest rates, we believe that we are in a good position to navigate the uncertain conditions that will be coming up.”

Since then, GDP growth exceeded expectations at 0.6% q/q SA nonannualized (0.4% consensus) and core inflation has held firm at 2.3% y/y. The policy rate lies within the ECB’s estimated 1.75–2.25% neutral rate range. As defence spending plans across Europe ramp up and trade tensions with the US pose uncertain risks to inflation, the ECB’s best course of action for now is to hold.

TURKEY’S CENTRAL BANK

Turkey’s central bank cut its one-week repo rate by 300bps to 43% (43.5% consensus). The 1-week repo rate had been reduced from 50% in December to 42.5% by March before a 350bps hike the next month. Erratic you might say. Inflation has ebbed but remains elevated at 35% y/y and ongoing weakness of the lira that poses consistent upward pressure on import prices. The central bank noted it expects July inflation to pick up on temporary factors, but that demand shocks will ultimately prove to be disinflationary.

UPDATED STATUS OF CANADIAN CONSUMERS

Canada refreshes retail sales (8:30amET) that probably fell in May with the lousy start to Spring, but key may be June when weather generally improved and which can affect seasonal categories. A caution is that they exclude anything related to services and hence provide a very incomplete picture of the consumer.

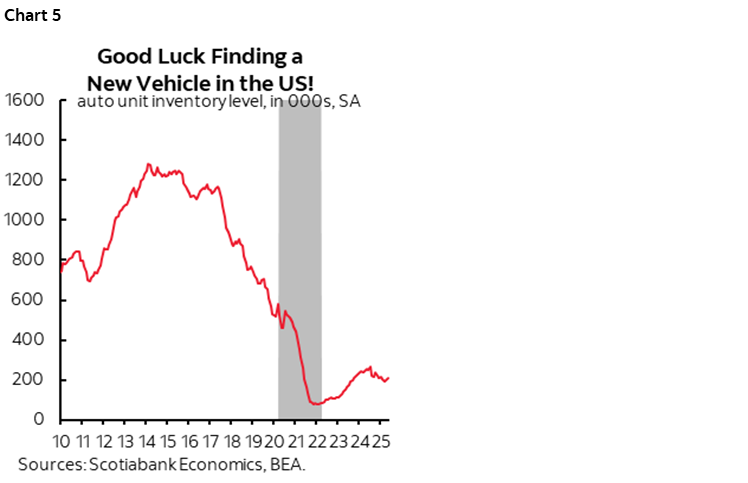

SURGING U.S. AUTO SALES, WEAK PRICES

Industry figures point to next week's US vehicle sales in July rising to about 16.4 million SAAR from 15.3 last month, for a 7.2% m/m SA rise. I think the rise is because the unwinding effect from tariff front-running as sales peaked in March and then slipped for the next three months got a stay of execution by postponed tariffs which sent more folks into dealers to buy even though the tariff effects operate with a lag.

It also looks like US new vehicle prices slipped by 2.6% m/m SA with used vehicle prices down -0.76% m/m SA in July. In weighted terms, this could suggest that vehicle prices combined will drag about -0.12% m/m SA off of headline CPI and with generous rounding up as much as -0.2% m/m SA off of core CPI in weighted terms. There are different samples and methodologies so these are just guides to expect somewhat of a weighted drag on July CPI from vehicles.

Industry sources estimate that tariffs will add US$4,275 to vehicle prices and there is caution into August, but the industry warns:

“Additional price adjustments are expected through the fall season, especially as new model-year vehicles launch, but final pricing strategies may not emerge until after year-end sales events."

That speaks to the point that markets are putting too much emphasis upon each individual inflation report in the very short-term to settle much of anything when the tariff effects are likely to unfold over months, quarters, even years. Old inventory and models are still working through the system. The industry had been in the process of rebuilding its inventory somewhat and is now selling it down ahead of tariff effects (chart 5). No inventory into tariff effects isn't a great combination if you plan on shopping for a new shiny set of wheels, or used, for that matter, as tariff arbitrage could easily spill over into that category.

FED TO BE UNDER ATTACK AGAIN

President Trump, the deeply critical FHFA head and homebuilder Pulte, and an entourage of administration officials will tour the Federal Reserve’s Eccles building after the market close today. It’s a performative stunt designed to showcase long overdue renovations including asbestos removal before the cameras. Perhaps Chair Powell should tour the gold-laden renovations to the Rose Garden, Oval Office and the rest of the White House at the same time. It’s clearly a diversionary stunt designed to divert away from the administration’s other policies and the President’s political problems. It’s also consistent with Trump’s general efforts to undermine all American institutions in populist fashion. I remain of the view that US monetary policy is appropriate and that danger lurks in efforts to undermine central bank independence (here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.