ON DECK FOR WEDNESDAY, JULY 23

KEY POINTS:

- Markets rejoice over US-Japan trade deal…

- ...perhaps out of relief and a sense of lowered uncertainty...

- …but despite its sharply unattractive features

- What the ‘deal’ seems to (tentatively) include

- US consumers and businesses will get hit by tariffs…

- …as a Trump-run investment fund applies capital controls…

- …and Japan appeared to give very little ground beyond accepting tariffs

- US Mag-7 earnings releases start in the after-market

- US existing home sales on tap

Global markets are in risk-on mode following the announcement of a deal between the US and Japan last evening and with some details made available in piecemeal fashion overnight. The fuller ramifications to the US and Japanese economies and markets may take time to be digested by everyone including market participants, but the impulsive response of financial markets is constructive at first. Count me skeptical. Deeply skeptical. It’s possible that the first-round market response is merely a relief trade that at least we might have the new rules of the game if they prove to be durable in the hands of an impulsive and volatile US President which reduces uncertainty for now, while leaving the toll upon global commerce yet to be paid over time.

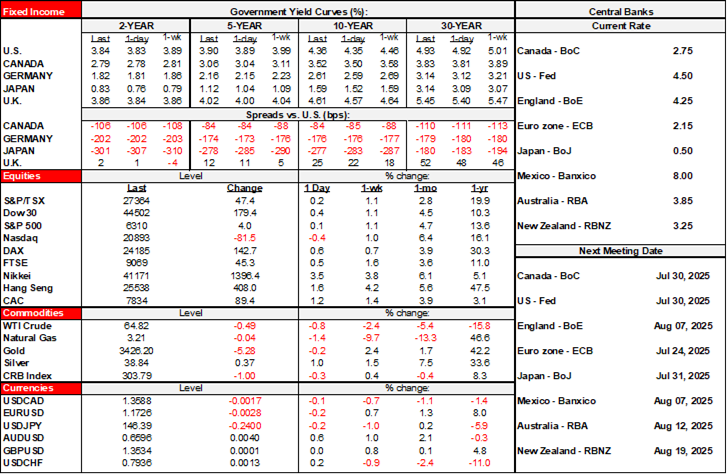

Stocks are higher and led by the Nikkei’s 3½% rise with milder gains elsewhere including US and Canadian equity futures that are up to ½% higher and gains in European cash markets of between ½% and 1½%. Sovereign bonds are taking it on the chin somewhat, with JGBs underperforming as yields climbed by 7–9bps across most of the curve and a little less at the very long end. US Ts, Canadian yields and EGB yields are gently higher with gilts underperforming. Asia-Pacific crosses including the yen, A$/NZ$/ TWD and won are outperforming. Oil prices are slightly lower.

I’ll get to the ‘deal’ in a moment, but otherwise, the calendar is very light today at least until the after-market. The US will release existing home sales for June (10amET). The ‘Mag7’ earnings releases kick off in today’s after-market and will include reports from Alphabet and Tesla.

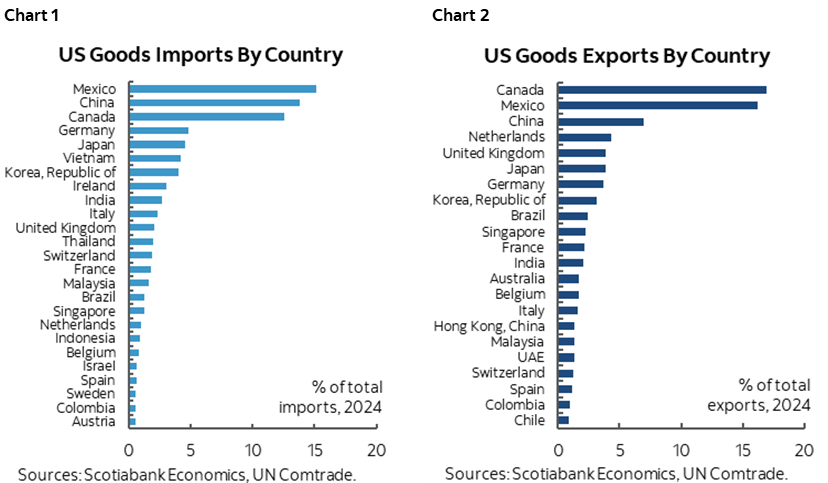

Also note that the EU is reportedly working on a no-deal plan to match 30% US tariffs. With next Friday’s US tariff deadline looming, we still don’t appear to have any traction toward trade deals with the most important US trade partners—Canada, Mexico, China, and the EU. Those countries/regions dominate US imports and exports (charts 1, 2). Tariffs against products from minor sources of US imports from Indonesia and Philippines were set at 19%. This article does a decent job of reflecting my initial thoughts about the US-UK ‘deal.’

THE US-JAPAN ‘DEAL’

We’re supposed to celebrate the US-Japan trade ‘deal’ that was announced last evening at first by Trump’s social media post and then through subsequent remarks pieced together from officials in media reports. US consumers and businesses will get hit by tariffs on Japanese imports, the investment pledge seems loose and lacking important details and is like a set of capital controls, and there appears to be very little else to celebrate. I’ll share aspects of the arrangement that I’ve pieced together below.

A strong caution is that details and a formal agreement still need to be worked out, just like the UK case. This could just be a de-escalation from higher tariffs and restrictions that were set for next Friday August 1st with uncertainties that still lie ahead in terms of the viability of a deal.

It all started with Trump’s social media post:

“We just completed a massive Deal with Japan, perhaps the largest Deal ever made. Japan will invest, at my direction, $550 Billion Dollars into the United States, which will receive 90% of the Profits. This Deal will create Hundreds of Thousands of Jobs — There has never been anything like it. Perhaps most importantly, Japan will open their Country to Trade including Cars and Trucks, Rice and certain other Agricultural Products, and other things. Japan will pay Reciprocal Tariffs to the United States of 15%. This is a very exciting time for the United States of America, and especially for the fact that we will continue to always have a great relationship with the Country of Japan. Thank you for your attention to this matter!”

Overnight media articles and comments by Japanese officials added a bit more to our understanding of the deal as follows.

- The US will impose a 15% tariff on Japanese imports that, while lower than the 25% that was threatened to kick in next Friday, still sticks it to American businesses and consumers unless you somehow believe that Japanese automakers will sell at a loss in the US market and their shareholders will tolerate it.

- Tariffs on Japanese exports of autos and parts to the US are to be lowered to 15% instead of 27.5% that would have included the pre-existing 2½% tariff plus an additional 25%. There appear to be no volume limits, unlike the UK trade deal that imposed quotas at 2024 levels. There also appear to be no US auto content requirements. The 15% tariff rate could allow Japanese automakers to gain import market share if higher tariff rates on EU auto exports and non-CUSMA/USMCA compliant auto exports from Canada-Mexico go ahead but that remains to be seen.

- Japan pledged a combination of investments, loans and guarantees totalling US$550 billion into the US. We need details. It’s unknown what the split is between the three components. Trump claimed that the US would retain 90% of any profits. Trump said the investments would be “at my direction” which suggests state-motivated projects and overnight anonymous remarks from a US official indicated it would be like a fund directed by Trump with Lutnick’s fingerprints all over it. That smells like capital controls, pork barrel politics and grift issues galore to me. It might be called the “Friends of Trump” fund. It seems that targeted sectors may include semiconductors, steel, shipbuilding, aviation, energy and AI. No specifics were provided and it’s not clear what the time period for such investments may be, whether they are truly new investments that wouldn’t have occurred otherwise, and whether there are enforcement and tracking provisions.

- There is nothing substantive on defence spending. Japan merely agreed to increase defence spending with American companies by an extra $3B per year to $17B/year which is a token gesture. Japan did pledge to raise defence spending at the recent NATO summit but it doesn’t look like there is any commitment to spend that increase on US defence companies.

- Japan will still face 50% tariffs on Japanese exports of steel and aluminum to the US.

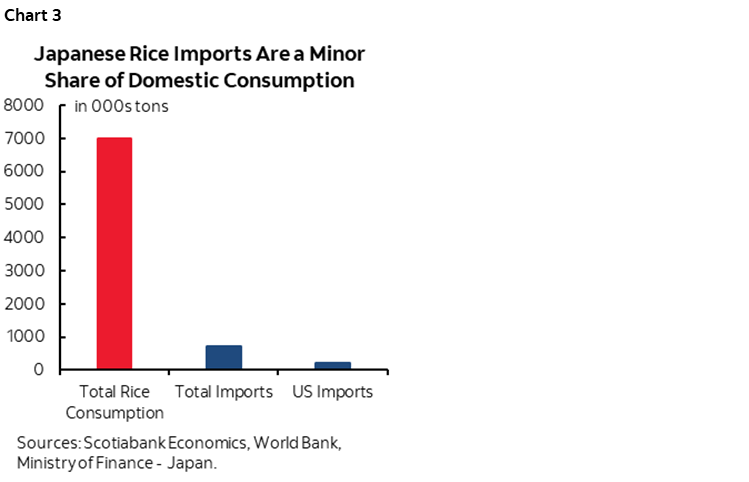

- Japan is to deliver token increases of purchases of US agricultural products such as rice but changed nothing in Japanese agriculture. Japan will increase rice purchases by 75% which will remain small in terms of levels. Reuters reports that the overall Japanese quotas on rice imports will remain unchanged and so import-substitution toward the US will come at the expense of other countries (here). Chart 3 shows that Japan’s rice market is basically closed anyway and so a 75% increase of basically nothing from the US is still basically nothing and doing anything else would have been political suicide for the government. Japan will also buy US$8 billion of agricultural and other products.

- Japan will drop additional safety tests on autos imported from the US that the US claimed hindered sales in Japan as opposed to different tastes and preferences compared to the types of US vehicles produced. Japan will apply lower US safety standards. It’s unclear to what extent if any that this was a barrier to US vehicle sales in Japan relative to safety standards for Japanese made vehicles in Japan but it appears to be the sole reason for why Trump claims Japan has now become more open to US vehicle imports.

- Japan may form a joint venture with the US to support a natural gas pipeline in Alaska for LNG exports. This project has been held up for an extended period.

- Japanese tariffs on US goods—while low going into all of this—will not be reduced any further.

- Japan pledged to buy 100 Boeing aircraft but it’s not clear whether its airlines would have done so anyway given rising global demand for air travel and capacity constraints.

- Japan appeared to secure a pledge from the US that any further sectoral tariffs imposed by the US on semiconductors, pharmaceuticals etc won’t treat Japan worse than other countries. That could still be very unfavourable, just not more so for Japan than others.

- Japan’s PM Shigeru Ishiba has for now denied widespread reporting that he is on the cusp of tendering his resignation following the loss of his coalition’s majorities in the upper house this past weekend and lower house last October. It’s unclear what effect this would have upon seeing the deal through to fruition.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.