ON DECK FOR TUESDAY, JULY 22

KEY POINTS:

- Mild risk-off tone amid a lack of fresh material developments

- Fed’s Powell to open a conference on regulatory capital

- Advice for Chair Powell to resign is just bonkers

- Fed’s Bowman—dove—to speak

- Canadian First Ministers retreat to plot strategy to deal with Trump

- Stale BoC surveys offered nothing useful—despite the biased coverage

- RBA minutes repeated the same message

- Brazil’s President threatens trade war in response to Trump’s 50% tariffs

We have very dull markets this morning. There is little movement across any of the global asset classes that have a tinge of a risk-off feel to them, no unifying themes behind them, and very little by way of regional developments. We just have ridiculous narratives to contemplate, like El-Erian’s advice for Chair Powell to resign to protect the Fed which is bonkers in my opinion; resigning would damage the Fed, capitulate to political interference, and threaten its independence while dramatically amplifying uncertainty.

RBA minutes told us the same thing a second time with respect to why the RBA held at its last decision on July 8th and both the A$ and rates complex shook them off.

Brazilian President Lula threatened a trade war would begin with his response when Trump’s 50% tariff on Brazilian imports goes into effect on August 1st if Trump doesn’t change course. Watch the real.

Federal Reserve Chair Powell delivers opening remarks at a Fed conference on the regulatory capital framework (8:30amET). Governor Bowman delivers an interview at 1pmET mainly on regulatory issues but she has also opined that a cut in July may be feasible so watch for any further dissenting signals. Otherwise, the FOMC is in blackout until one day after the July 30th decision. The Richmond Fed’s manufacturing index will be refreshed for July (10amET) and regional surveys to date are constructive for the month of July.

Canadian First Ministers are gathering at Deerhurst Resort in Huntsville, Ontario to discuss trade tactics. There may be developments around opening remarks or subsequently (10amET).

Mexico updates some readings for back in May, including retail sales and the GDP proxy aka economic activity index (8amET).

STALE BOC SURVEYS SETTLED NOTHING

Why all the fuss yesterday in several articles about the Bank of Canada’s surveys (here and here)? Good heavens, doves, you’re really desperate for something to hang your hats on. Consider the following points:

- First, the surveys are stale on arrival. Ridiculously so. The Canadian Survey of Consumer Expectations was conducted from April 24th to May 15th and there were follow up phone interviews from May 20th to 26th. Why on earth does it take any other consumer polling company little time to turn around in-month or in-week surveys, but it takes the BoC 2–3 months?! That’s just unacceptable folks especially these days when rolling on and off tariff threats have coincided with the election aftermath in Canada plus early fiscal stimulus and speculation toward how much more lies ahead. The Business Outlook Survey was conducted from May 8th to May 28th and the companion Business Leaders’ Pulse was conducted in each month of April, May and June but not July yet. Again, stale on arrival when the world’s fast paced developments require timeliness.

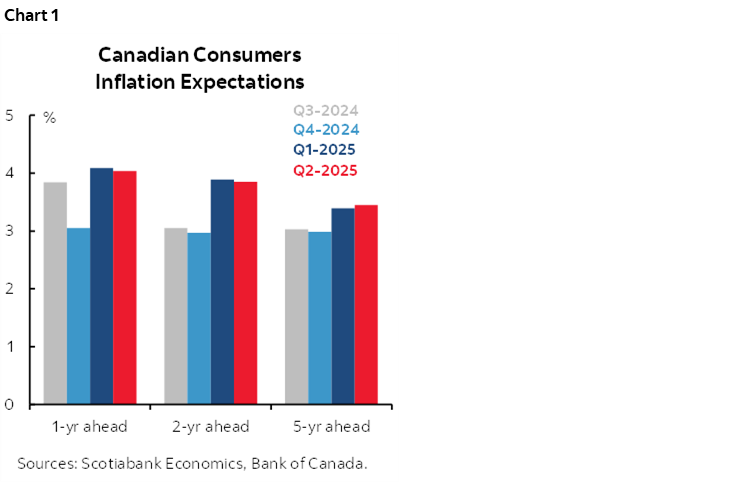

- Second, even though just as stale or more so, why did all the articles choose to ignore that consumers’ inflation expectations were unchanged at elevated levels (chart 1)? That seems like an unhealthy bias to me.

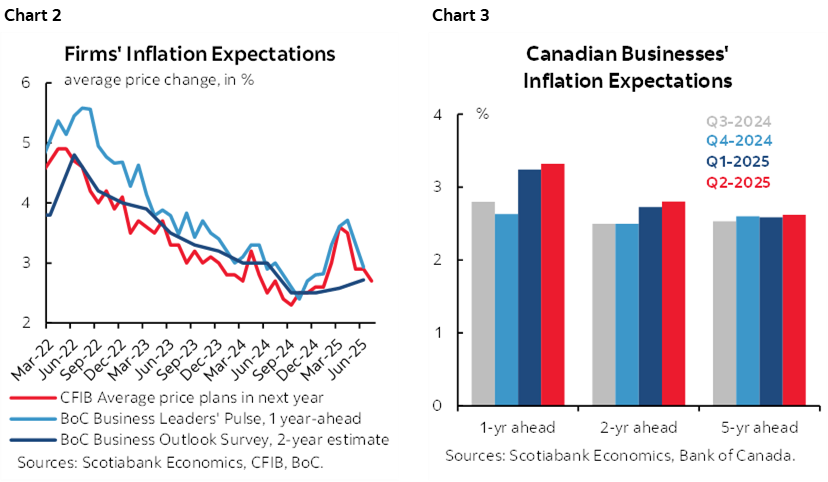

- Third, on the business surveys, there was nothing new that we didn’t already know from the CFIB’s survey of small businesses that had already shown the decline in inflation expectations on a monthly basis (chart 2). Across other business measures of inflation expectations over varying time periods the results were largely unchanged (chart 3).

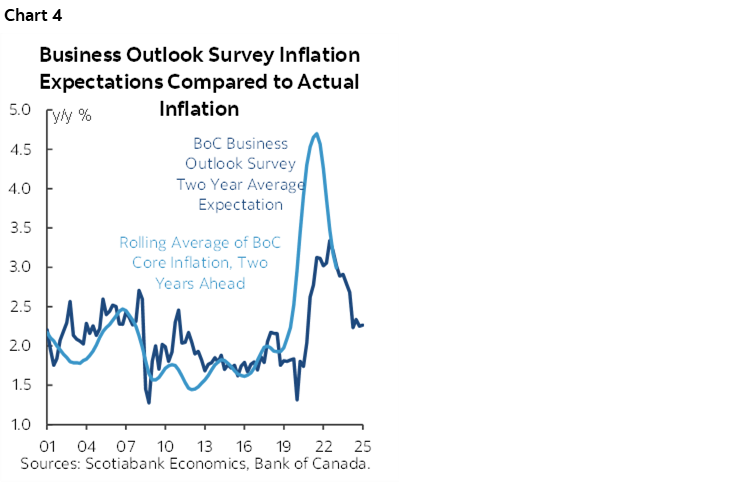

- Fourth, who cares anyway. The BOS survey has a small sample of about 100 firms with questions posed to ‘senior management,’ whatever that means, but it’s unclear whether they’re close enough to the consequences of tariffs on pricing and ordering. At a certain exalted level the attachment to the core front line business becomes more and more remote. And the BOS survey’s measure of inflation expectations two-years ahead performs poorly as a measure of actual reported inflation two years ahead (chart 4); businesses tend to react to inflation bursts, rather than lead it and are no better at formulating expectations for their pricing plans than markets are at expecting inflation outbursts. Inflation is a complex beast and I’ve always found that neither businesses or consumers really have much understanding of the concept and when they form expectations it’s based on the price they just paid to fill up their gas tanks or grocery carts.

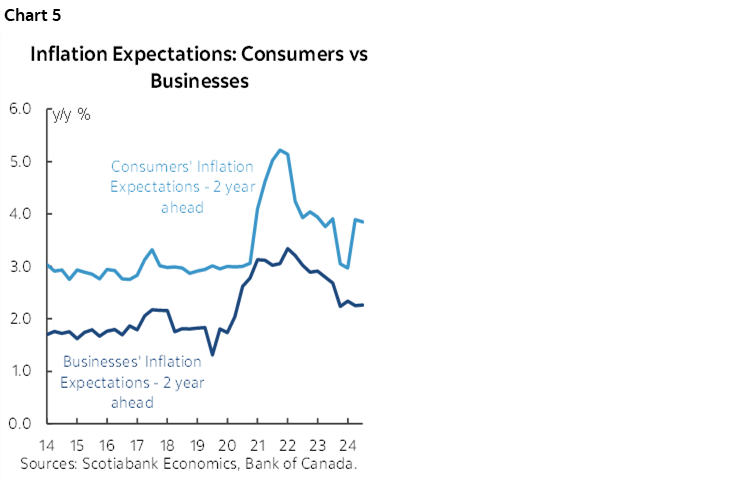

- Fifth, consumers aren’t any better than businesses (chart 5) and arguably a touch slower.

So all told, there is vast room for improvement of these surveys, and I wouldn’t attach much if any significance to them at least until they are much more timely and probably not really that much even then. The core issues affecting the BoC remain very little economic slack to date, inflation that has multiple drivers beyond output gaps that themselves involve a lot of guesswork, core inflation that remains far too hot in smoothed m/m SAAR terms to be contemplating easing any time soon, and high uncertainty surrounding the path forward for trade the fiscal policies. And that’s only a partial list.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.