ON DECK FOR FRIDAY, JULY 18

KEY POINTS:

- Dollar continues to weaken into the end of the week

- Often-wrong Governor Waller drives a mild market response

- Powell responds to Vought’s letter—and should have sent a bill with it!

- Yen softens, JGBs rally for three reasons

- German PPI masks rise of consumer prices, like US PPI did

- Politicized UofM sentiment on tap

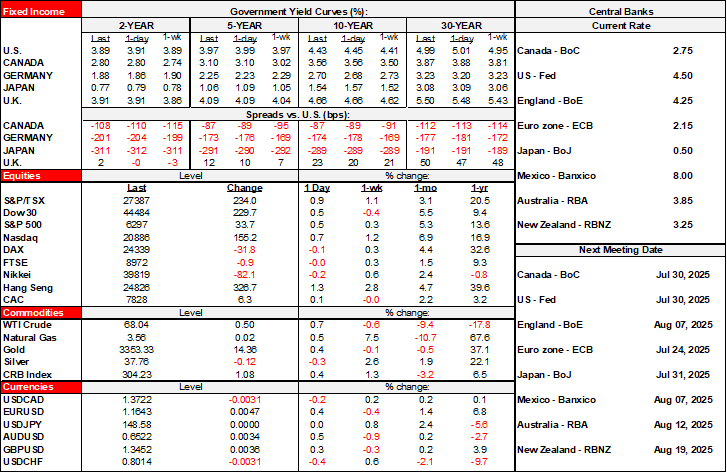

A slight risk-on bias is marking the end of the week. Equities are broadly higher. The dollar is broadly in retreat. US Ts are mildly outperforming European yields.

OFTEN-WRONG WALLER LEADS MARKETS ASTRAY ON THE FED’S JULY DECISION

One consideration is that Fed Governor Waller said last night at about 6:30pmET that the Fed should cut by 25bps on July 30th. The dollar slightly weakened on the headlines and this is probably why the US front-end has mildly rallied.

His reason is to save the labour market. Nothing to date would create a sense of alarm over the state of the labour market in my view but Waller has been an inflation dove all along so—while contestable—his views are at least consistent. That contrasts with Trump who says his ‘big beautiful bill’ will supercharge growth and do such wonderful things, but that the Fed should cut to 1% from 4½% now which would only happen if a true crisis was around the corner.

Waller is likely to dissent on July 30th and may either be alone in dissenting or perhaps joined by Governor Bowman.

A big caution is that Waller has a habit of being wrong. He has previously driven premature pricing of Fed rate cuts like in late 2023 when he advised the Fed could cut within a few months as soon as March but the FOMC didn’t cut until September. Or take his dissenting vote against tapering Treasury QT at the March meeting earlier this year which in retrospect has looked like he was in the wrong. I feel he’s jumping the gun on easing when we don’t have evidence on which part of the dual mandate may deteriorate more than the other, when, and by how much in the face of the unique shocks presented by Trump administration policies.

Waller also stands accused of being somewhat opportunistic in the battle to succeed Chair Powell.

POWELL SENDS RESPONSE TO VOUGHT; SHOULD HAVE SENT A BILL TOO

Chair Powell responded to OMB director Vought’s accusatory letter with this letter sent last night. He should have also sent Vought a bill. Think of all the management time that has been wasted at the Fed responding to this politicized nonsense instead of thinking about monetary policy!

YEN SOFTENS, JGB YIELDS RALLY ON THREE DRIVERS

The yen softened a touch and JGBs are a touch richer across the curve after national core inflation decelerated by a little more than consensus expected. CPI ex-fresh food landed at 3.3% y/y (3.7% prior, 3.4% consensus). Markets are also focused upon the weekend election in Japan’s upper house with less fear that the outcome will drive a spending splurge financed by more debt. There is also a piece out from Reuters this morning about how the BoJ might indicate upgrade its near-term outlook at the July 31st decision.

GERMAN PPI REFLECTS CONSUMER PRICE PRESSURES LIKE US PPI

German producer prices landed on the screws in June at 0.1% m/m. Consumers goods prices were up by 0.3% led by non-durable goods which is similar to what happened to the US PPI figures the other day. US PPI was flat, core PPI was also flat, but come categories may have revealed tariff pressures such as big-ticket durable consumer goods prices that were up 0.4% m/m after a 0.5% jump the prior month.

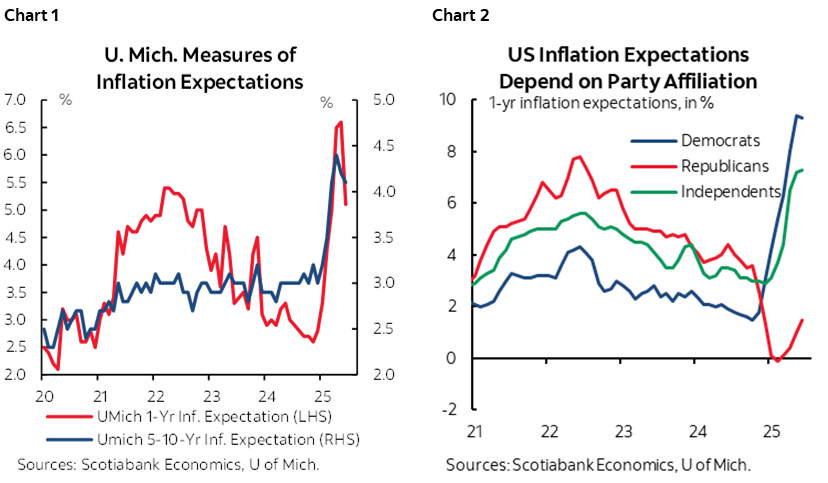

POLITICIZED UMICH SENTIMENT TO BE REFRESHED

Light readings are on tap into the N.A. session. The US updates UMich consumer sentiment and its politicized measures of inflation expectations (charts 1, 2) where Republican respondents say there is no inflation risk whatsoever and Democrats say it’s going to the moon. What isn’t disturbingly politicized in America these days. Housing starts are expected to post a mild rebound in June’s release (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.