ON DECK FOR WEDNESDAY, JULY 16

KEY POINTS:

- Cautious mood reflects more Trump warnings

- Trump warns tariffs on pharma, chips and small countries are coming shortly

- Pharma tariffs are regressive and will add to soaring US prices

- Trump says renovations controversy is a “fireable” offence for Powell

- UK core CPI jolts gilts

- Will US PPI showcase additional tariff effects after CPI did?

- BoE’s Bailey launched into global imbalances and US tariffs in an excellent speech

- More Fed-speak on tap

- US bank earnings continue to beat

- How could Canada retaliate against US tariffs? By ghosting, Canadian style.

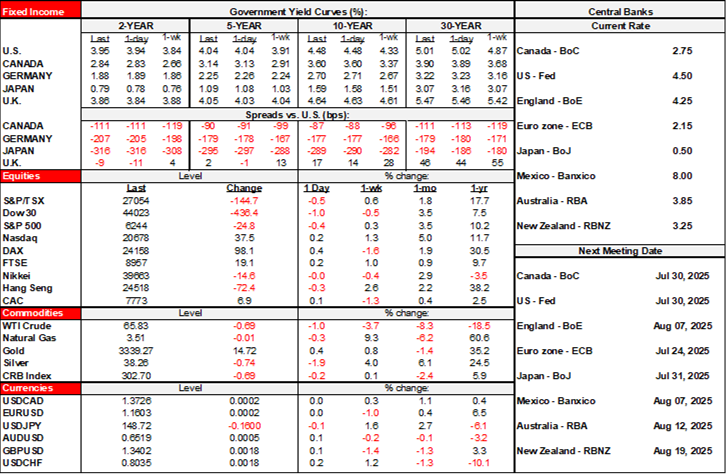

Risk appetite in markets is on cautious footings after Trump went off the rails with a bevy of additional tariff threats and an unwise warning about Chair Powell’s “fireable” offence last evening. Equities are little changed across US and Canadian futures and European cash markets. Sovereign bonds have a slight richening bias outside of the UK post CPI (recap below). The dollar is mixed with other crosses like the euro, yen, sterling, the A$ and CAD outperforming it a touch despite—or because of—Trump’s behaviour.

TRUMP ADDS MORE TARIFF THREATS, WARNS POWELL

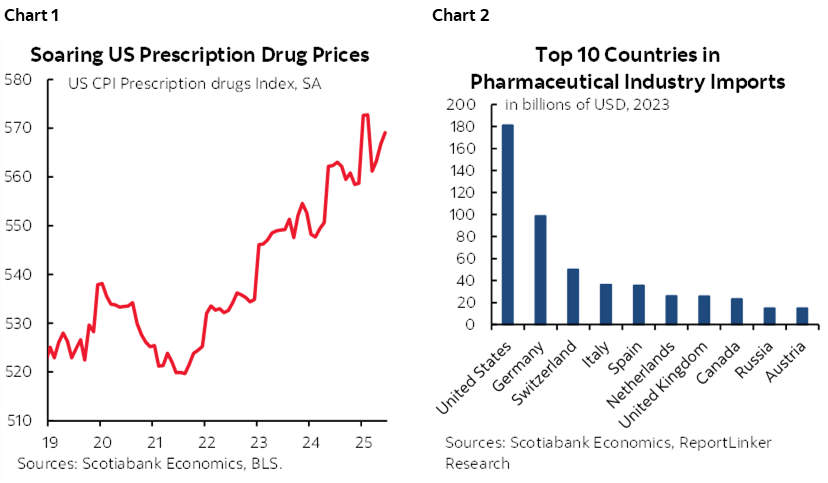

Trump said last evening that pharma and chips tariffs would probably be coming by month’s end. He said pharma tariffs would “start off with a low tariff and give the pharmaceutical companies a year or so to build, and then we’re going to make it a very high tariff.” The US already faces soaring pharmaceuticals prices (chart 1) that would become further inflamed by protectionist tariffs. This makes zero sense and is another highly regressive policy move by the US administration. The US is the world’s biggest importing nation (chart 2) and there are many reasons for this, including over-prescribing.

Trump also said that “small” nation’s tariffs would be set in one letter and likely at a blanket rate of over 10%, hence less than for larger countries. The market reactions are relatively muted because a) tariffs were expected eventually given his prior remarks, and b) because markets have adopted a ‘show me the proof’ posture over his rhetoric.

Trump also said “I think it sort of is” when asked if allegations surrounding the Fed’s renovations and Chair Powell’s involvement were a fireable offence. Technically the Fed Chair can be fired for cause in certain instances, but this one is very unlikely to tick that box and the Fed is coming out swinging which indicates it would take any fight as far as it needs to go including to the Supreme Court. One way the Fed is pushing back is through this post last weekend. I wonder how Trump would feel if his lavish White House renovations including to the Oval Office had to deal with asbestos!

Personally, I think it’s all just a bunch of performative stunts by the administration that, while dangerously undermining the Fed as part of the MAGA base’s efforts to undermine all institutions in favour of one person’s supreme powers, seeks to offload onto it any accountability for the effects of terribly unsound macroeconomic policy being pursued by the administration. The Fed shouldn’t be easing until it has comfort with the uncertain and competing effects of tariffs on the dual mandate and because it has to be wary of the moral hazard issues should it bail out unwise trade and fiscal policies only to embolden more unwise steps.

UK INFLATION JOLTS GILTS

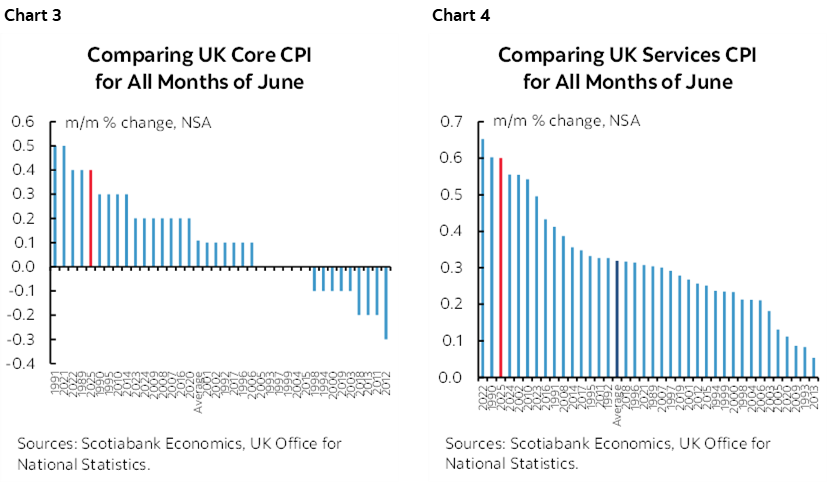

UK core CPI landed at 0.4% m/m NSA in June which is among the hottest readings on record (chart 3) when comparing like months of June (since it’s NSA data). That was enough to pop the year-over-year core CPI rate to 3.7% from 3.5% previously and surpassing consensus expectations for an unchanged reading. The core CPI surprise was behind the up tick in headline CPI to 3.6% y/y from 3.4%. Stickier than expected core services CPI was a driver (chart 4).

The gilts curve is accordingly underperforming everywhere else this morning, but not alarmingly so. Yields are up by about a couple of points across the curve and sterling is among the relative outperformers to the USD but with plenty of company. Pricing for the BoE’s August 7th decision was marginally affected and still solidly leans toward a 25bps cut.

Why was BoE pricing hardly impacted? Because the real side of the UK economy is deteriorating and that’s more likely to capture the BoE’s attention. GDP continues to shrink along with industrial output with services weakening and ditto for the job market. Besides, an August cut would extend the ‘gradual’ approach the BoE uses that involves an oscillating pattern of cuts and skips.

US PPI TARIFF WATCH

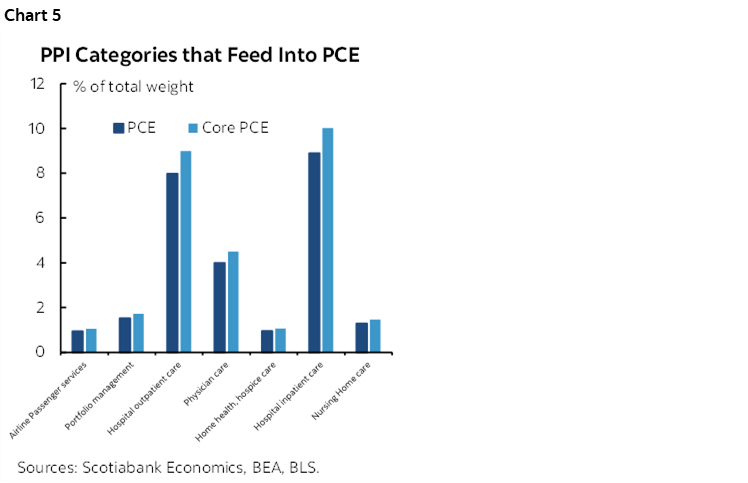

US core PPI may reflect tariff effects more than CPI which is a further step removed from pass through, but the PCE-relevant categories wouldn’t be likely to be affected by tariffs (chart 5). Consensus expects a 0.2% m/m rise with several at 0.3%.

MORE FED-SPEAK ON TAP

Several Fed-speakers will continue to respond to US inflation figures today. Dallas President Logan said last evening that the tariff impact won’t be clear at least until Fall and supports a continued patient stance. Richmond’s Barking (8amET), Cleveland’s Hammack (9:15amET), Governor Barr (10amET), Atlanta’s Bostic (3:30pmET), NY’s Williams (5:30pmET) are all on tap along with the Fed’s Beige Book of regional conditions at 2pmET.

US EARNINGS CONTINUE TO ROLL OUT

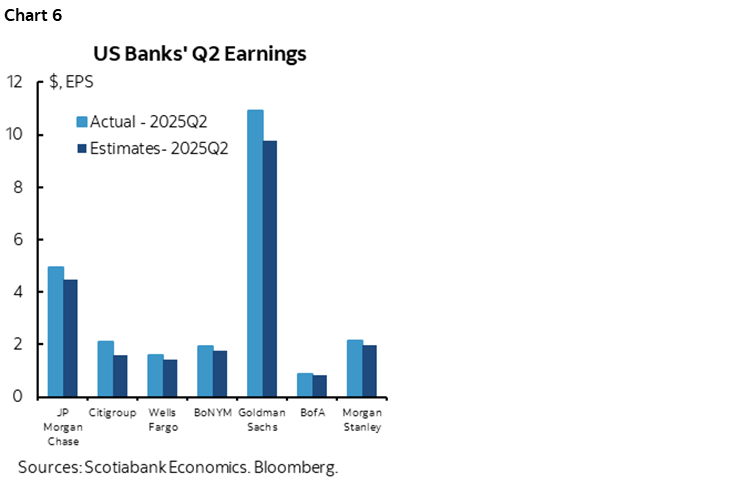

More major US banks are issuing earnings reports this morning. Results were solid from each of Goldman Sachs, Morgan Stanley, and BofA but market reactions were somewhat mixed (chart 6).

BOE’S BAILEY ATTACKS US TARIFFS

The quote of the day goes to Bank of England Governor Bailey who warned of misguided US trade policy and “dangerous” US tariffs in this speech. He said this:

“There is ... a common interest globally in tackling excess imbalances before dangerous levels of trade restrictions come into play, and before we face the prospect of difficult adjustment with macroeconomic volatility and financial instability.”

“The US does need to explain how it can regard its internal imbalance as sustainable and its external imbalance as not so, and how it envisages the internal balance responding to an adjustment of the external balance flowing from tariffs taking effect.”

IMPLICATIONS OF BEING STUCK WITH TARIFFS AGAINST CANADA

Trump isn’t playing smart politics with Canada. His best chance at a collaborative trade and security arrangement on its northern border is with Mr. Carney’s administration that he is undermining. Remember, Carney heads a minority government. Any trade deal has to get majority support in Parliament when it comes to a bill. There would probably be strong push back against a deal involving persistent US tariffs against Canada, let alone anything to do with supply management that the BQ would vote against and perhaps with support from others. Minority governments tend to have limited shelf lives in Canada. The US stands the best chance of a meaningful trade and security arrangement with Carney who has bent over backward to appease Trump and arguably at significant political risk should appeasement fail in the end. If Trump continues to overplay his hand, then US companies with exposure to Canada and security cooperation would be among the things most at risk along with the stability of the Canadian administration.

How could Canada respond? Keep trying to negotiate as the best option, but so far it seems to be largely fruitless because Trump is fundamentally a protectionist. There is a high bar set again retaliatory tariffs. Canada's retaliatory tariffs have tended to fall well shy of dollar-for-dollar to date and the bias has changed. The bias has been to apply limited measures against politically sensitive sectors/regions in the US and particularly where there are substitute products available and without causing undue harm in Canada.

A more passive approach could ensue in lieu of retaliatory tariffs. How very Canadian to avoid direct confrontation while choosing an alternate path. One path could entail excluding US firms from Canadian procurement and participation in defence and infrastructure projects when the government's Fall budget is likely to set up hundreds of billions if not well over a trillion dollars of such activity. And/or exclude them from access to resources, particularly critical minerals. Get that additional pipeline built to sell more to Asia rather than the US that needs Canada’s heavy crude. The US is risking Canada becoming more open to foreign investment from other nation states with incompatible interests to the US. The DST may come back just as Europe contemplates applying its secret weapon against US tech. And/or Canada may exclude US firms from sectors that may become more open.

There are lots of tools at Canada's disposal in a more passive set of tactics rather than locking horns over tariffs and that could be more painful to US companies than tariffs over the long haul by excluding them from the market and emergent opportunities. A ticked off consumer base that continues to substitute toward domestic and non-US foreign options is already a factor. I for one am loving my new made-in-Canada bbq.

Or simply wait it all out and let US voters see the mounting harm if Trump doesn't back down, which his history suggests he may well do. Let Trump go into midterms explaining how his massive tariffs against all major trading partners have impacted the economy while risking the GOP’s thin majorities in Congress.

In essence, Canada could adopt the strategy of ghosting the US, rather than confronting the Trump administration outright. You want to limit Canada’s access to the US, then Canada will do likewise through alternative means. Canada has plenty of firms who could serve its infrastructure goals and there are plenty of firms in Europe, Asia and Latin America that are chomping at the bit to have access to emergent opportunities in resources, infrastructure and defence. Canadians can buy smartphones, vehicles and capital goods from many other companies at home and companies across other countries in Asia and Europe which represents the risk of lost opportunity for American firms exporting to Canada which is America’s largest export destination by country.

The best option of course is for Canada and the US to remain tightly integrated in a sensible agreement. Failing that, political uncertainty and alternative arrangements are at risk. It is not in America’s best interests to have instability across the Americas in its own backyard.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.