ON DECK FOR MONDAY, JULY 14

KEY POINTS:

- Mild risk-off sentiment has multiple catalysts

- Trump threatens 30% tariffs on Mexico, EU…

- …that markets are largely fading due to a credibility problem…

- …and instead of retaliating, why not just walk away in unison?

- Chinese financing surges on government bond issuance, weak private credit

- Chinese trade beats expectations…

- …but rolling waves of pushed out tariffs also push out the pain

- Markets cautious into a packed week

- Global Week Ahead — Cage Match

Mild risk-off sentiment could have multiple drivers into a packed week. N.A. equity futures are down by about a quarter point (US) or less (Canada) while European equities are off by as much as 1% except London that’s up. Currencies are mixed as it’s not just the dollar that is resilient; the yen, euro and related crosses, plus CAD are holding their own. CAD is firm likely as continued aftermath of Friday’s jobs report. Sovereign yields are mixed with slight cheapening in US Ts and Canadian yields and bull steepening in gilts and EGBs. BoE Governor Bailey’s remarks were selectively interpreted as dovish as he pointed to gradual moves in light of inflation, but potentially bigger moves if slack opens up at a quicker pace.

TRUMP HITS EU, MEXICO WITH 30% TARIFFS

One catalyst is that Trump sent two more letters Saturday morning that announced 30% tariffs would be imposed upon Mexico and the EU by August 1st. We’ve gone from tiny players in US trade to now Canada, Mexico and the EU facing steep rates. Why isn’t the sell off grander? Moves like these are fairly trivial. It could be because few believe Trump’s threats as he has lost credibility by constantly pushing out deadlines, going far too high on tariff threats, and backing off while nobody understands the shifting goals of the Trump administration in trade talks. Trump fatigue is settling in.

WHY NEGOTIATE??

And so on that note, my advice would be not to retaliate and to simply refuse to negotiate. You could retaliate against politically sensitive regions in Trump’s base, but it may not be needed. The inclusion of so many major trading partners that are facing steep tariff rates is a tax on American businesses and consumers that will bring pain and divert trade. They hurt everyone, but let the US administration harm the US economy, its workers, and the prices they pay—all into midterm elections. There would clearly be a price to pay for America’s trading partners if Trump stuck to such tariffs, but it’s never clear that he will, and the price of being pushed into bad agreements could be steeper over time. Further, Trump keeps changing the goalposts and then violating his own agreements which severely impairs trust in any negotiations in the first place. Knock it off, and then we’ll talk. A challenge to this approach, however, is that it requires unity and a coordinated approach by trading partners. Many countries are balking at US demands.

UNCERTAINTY INTO A PACKED WEEK

A second catalyst for risk-off sentiment is likely the uncertainty into this week’s developments. One is what Fed Chair Powell’s response to Russ Vought’s letter on behalf of the administration may be given the one-week window for a response by Thursday. Another catalyst could be cautious expectations into the Q2 US earnings season that begins in earnest tomorrow. Another could be data, mainly in the form of US CPI and a whole range of global readings. Please see the Global Week Ahead—Cage Match (here).

- Inflation updates to pit “Too Late” against “Too Early”

- US CPI: could this be the start of pass-through pressures?

- Canadian core inflation’s firm trend enters tariff uncertainties

- Why the BoC is likely to extend its policy hold

- Chair Powell’s response to Vought and the grey area around ‘for cause’

- US Q2 earnings season begins in earnest...

- ...and could inform tariff debates

- China to provide damage assessments of early tariff effects

- US also updates retail sales, industrial output, consumer sentiment

- Will Aussie jobs restore momentum?

- UK CPI, jobs and wages unlikely to sway the BoE from its gradual easing path

- Bank Indonesia to trade off tariff threat versus rupiah stability

- Indian CPI the last reading before the RBI’s next decision

CHINESE FINANCING IS WEAK, FADE EXPORTS

Overnight data was light and focused on China and was mixed.

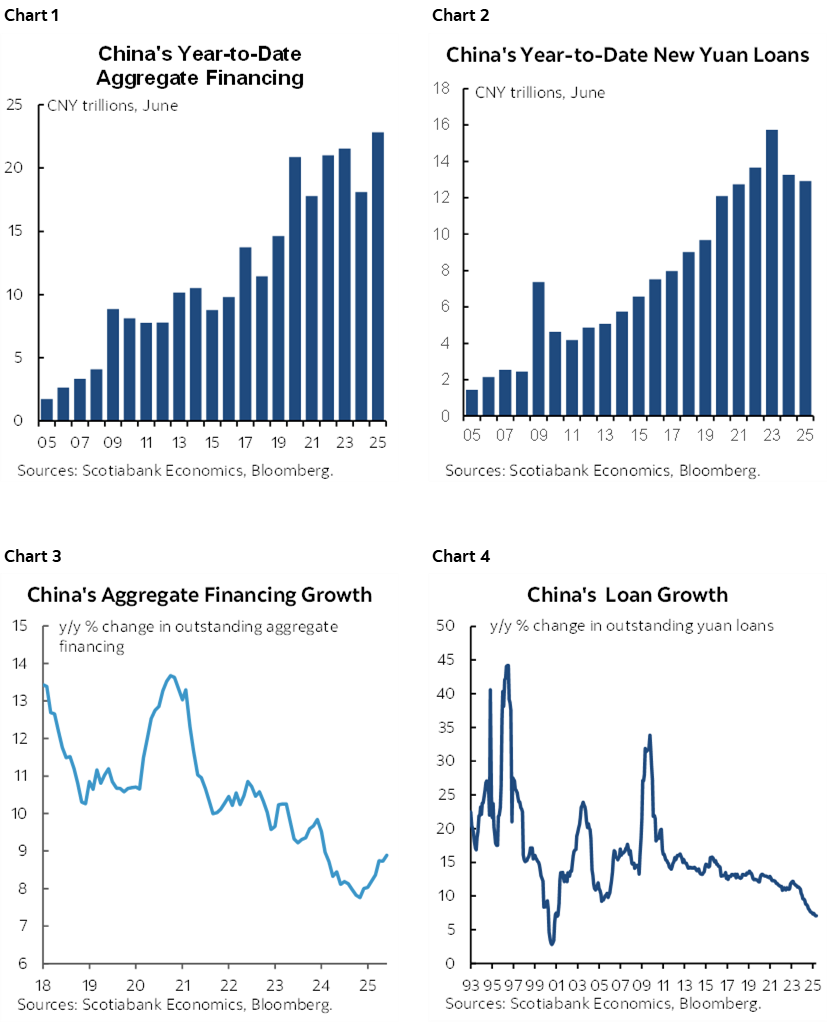

China’s financing figures are indicating softness in the private economy. While aggregate financing was a touch above expectations for year-to-date readings (chart 1), this is occurring because of government bond issuance. Domestic currency loan originations, however, are at their slowest pace since 2021 when the pandemic’s effects were being felt (chart 2). Growth in aggregate financing outstanding is accelerating (chart 3) for the same government bond reason, while growth in yuan loans outstanding is at its slowest since 2001 (chart 4). Monetary policy is encumbered by relatively inelastic demand for money in a climate of economic uncertainty and still falling property prices.

China’s trade figures beat expectations for June, with a strong caveat. Exports were up 5.8% y/y in dollar terms, and 7.2% in yuan terms, while imports were up 1.1% and 2.3% in dollar and yuan terms respectively. The caveat is that the constant pattern of pushing out Trump’s tariffs and staggering their application over time has driven companies to try to beat them before stiffer ones may apply. That makes it too soon to evaluate an effect on trade.

INDIAN INFLATION BOLSTERS RBI CUT PRICING

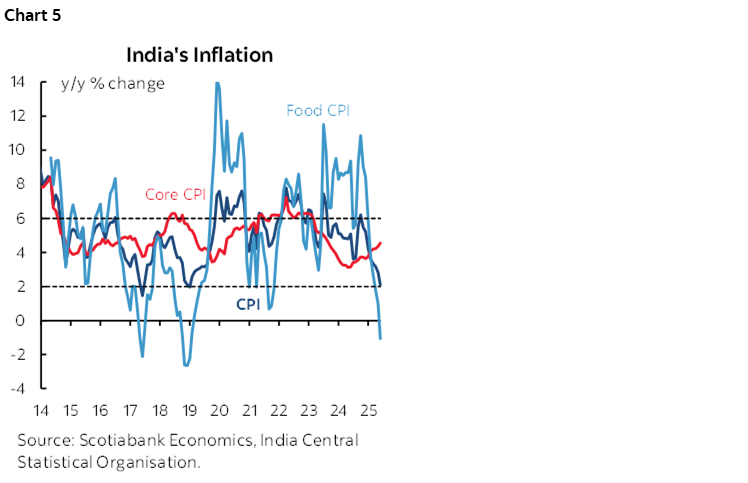

RBI watchers were a bit taken aback by weak CPI (2.1% y/y, 2.25% consensus). That’s the weakest reading since early 2019 and significantly due to food prices. Core CPI, however, has continued to accelerate toward 4½% y/y (chart 5). The rupee had already weakened before the figures along with several other Asian crosses on trade worries.

There is nothing material on deck for Canada or the US today with just Canadian wholesale trade expected to have declined in May (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.