ON DECK FOR FRIDAY, JULY 11

KEY POINTS:

- Risk off sentiment driven by Trump’s protectionism

- US threatens 35% tariffs on Canadian exports in addition to sectoral tariffs…

- …but would only apply to the falling share not CUSMA/USMCA compliant…

- …which lowers the effective tariff hit to a still meaningful risk

- Trump’s rationale for Canadian tariffs remains based upon lies

- PM Carney keeps calm, talks on toward a revised August 1st target. Good luck.

- Canada jobs update pending

- UK markets little affected by weak data

- BCRP holds as expected

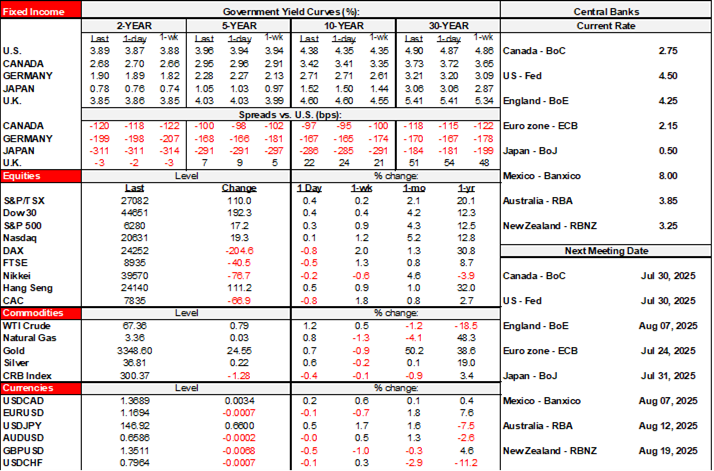

Risk off sentiment is sweeping through global markets but in generally contained fashion and in well functioning markets. N.A. equity futures are off by about ½% with European cash markets down by around 1% across most bourses. The dollar is slightly firmer against multiple crosses with the Swiss franc outperforming that will be problematic for the SNB. Sovereign yields are broadly higher but gently so, except for a very slightly richer front-end in Canada.

The aftermath of Trump’s tariff letter to Canada will combine with fresh job market readings from Canada to drive local markets today. Overnight developments were otherwise light including weak UK data nobody much cared about, plus BCRP’s hold.

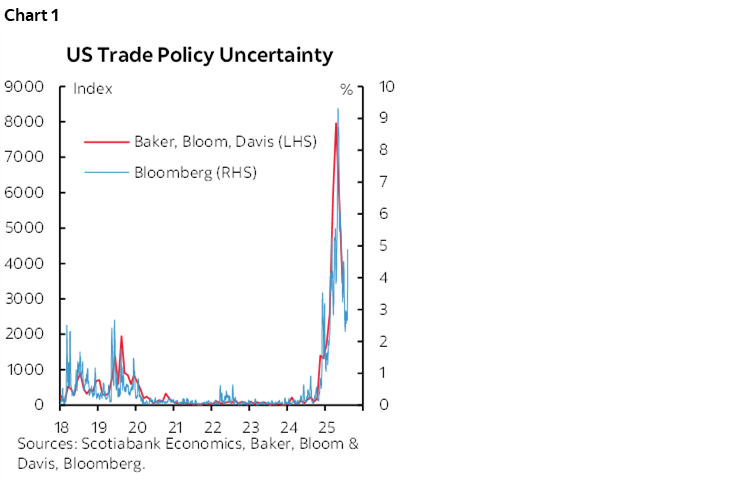

The bigger issue here is that uncertainty is on the rise again as indicated in chart 1 that plots two measures of US trade policy uncertainty, one being a lower frequency index and the other being Bloomberg’s daily measure which is sure to spike even higher when it’s updated for today. This historic uncertainty surrounding the rules of commerce will damage confidence to spend, hire, and invest in the world economy including in America. It is a total own-goal by a US administration whose policies are needlessly damaging the US and world economies.

TRUMP’S TARIFFS ON CANADA

US President Trump assaulted Canada out of the blue last night in this post on his social media account. It threatens tariffs of 35% on Canadian exports by August 1st that a US official later confirmed to apply only to goods that are not USMCA compliant which I’ll return to in a moment. They are in addition to sectoral tariffs primarily on metals (aluminum, steel, copper). For now, the response in local markets is fairly muted with CAD slightly weaker by about a third of a cent to 1.3690 (73 cents US) and TSX futures off by about ½%, both of which are in line or less significant moves than across other currencies and equity benchmarks.

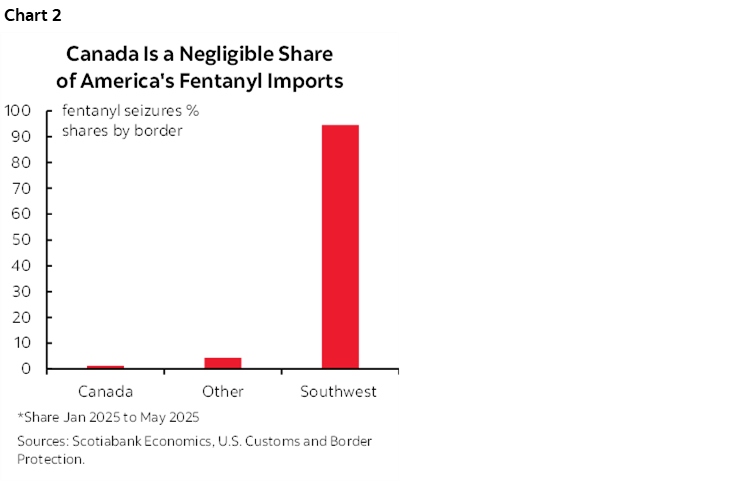

First, the letter is replete with the usual lies about my country and they need to be rebutted every single time they are advanced. Trump repeated his false claim that Canada is the source of America’s fentanyl drug problem, and that Canada protects its dairy farmers with 400% tariffs which is also not true, and he got the sign on the trade balance that matters wrong again.

Canada is a miniscule share of US fentanyl (chart 2) and America’s drug problem is caused by its own policies including lax control over opioids and doctors’ prescriptions and domestic surveillance with imports an issue with China and Mexico, not Canada. Extreme income inequality in the US relative to other advanced nations certainly doesn’t help.

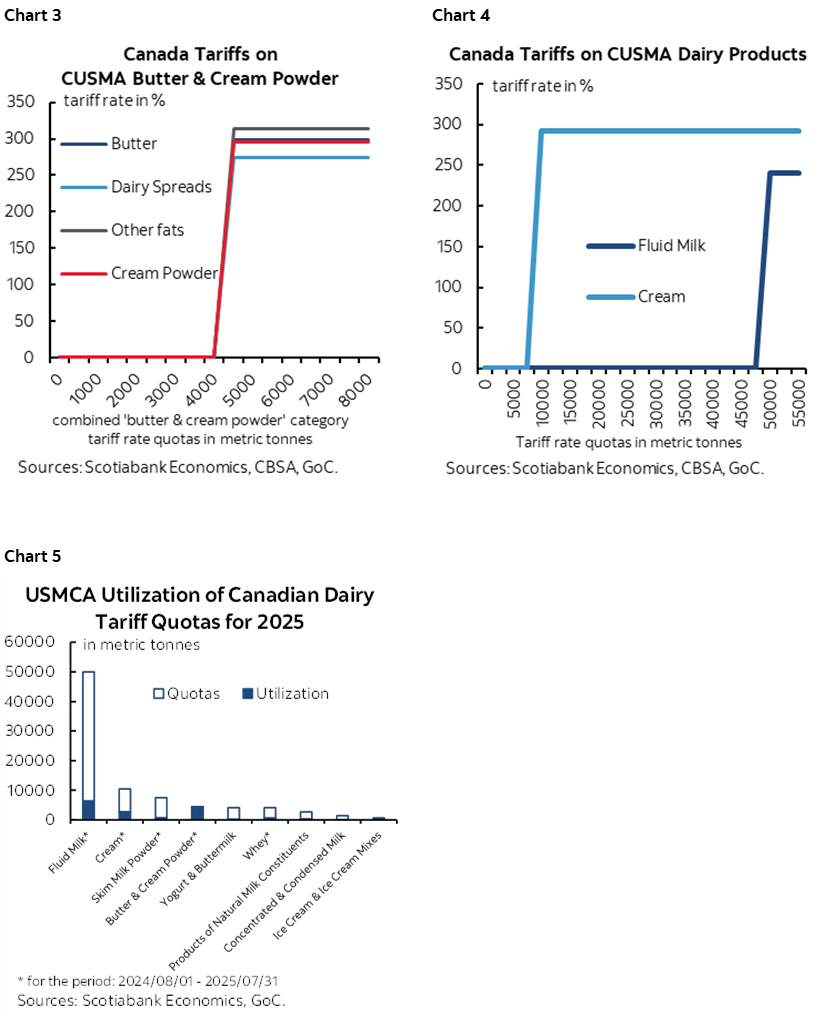

Canada imposes tariffs above a dairy import threshold from the US (charts 3, 4) that US dairy producers never hit (chart 5) and the US does the exact same thing to Canadian dairy exports under Trump’s own USMCA agreement that he called the best ever! Furthermore, the US Farm Bill is a massive collection of hundreds of billions of dollars worth of distorting subsidies to American farmers that distorts world agricultural trade alongside Europe’s Common Agricultural Policy. The US and EU apply agricultural sector trade policies that keep developing countries poor, force consumers across developed and developing nations to pay too much for food, and that serve narrow yet politically influential groups.

Trump flags America’s trade deficit with Canada as a driver of his concern when it’s well known that Canada runs a trade deficit with the US after removing energy exports that America needs particularly given its lack of heavy bitumen reserves that go into producing various distillates. Besides, the White House’s understanding of what causes trade deficits is woefully deficient while deflecting accountability for domestic policy drivers, like constantly encouraging high consumption and big fiscal deficits in highly regressive fashion.

All of this says that negotiating with the US may be entirely pointless as Trump keeps shifting the goal posts, nothing done to address his false claims resonates, and he keeps reverting to the same nonsense.

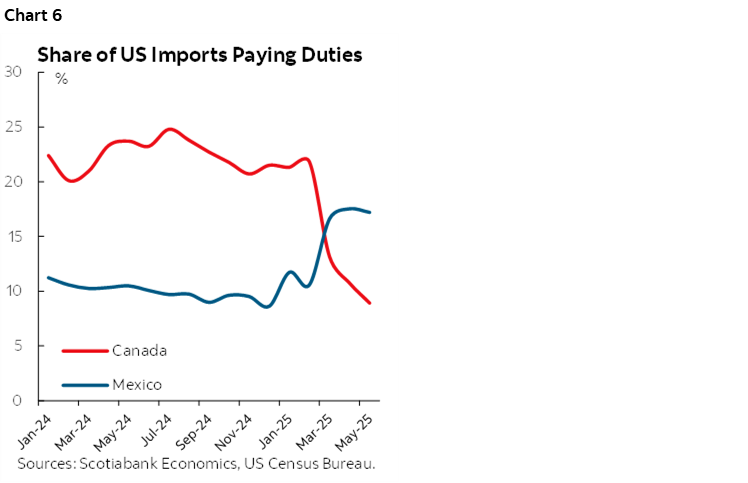

What’s the likely impact? Well, that depends on what sticks and what happens between now and August 1st or by whatever date gets punted again. Right now, around half of Canadian exports to the US are USMCA compliant. That share has been rising quickly. Estimates indicate that this share could be easily raised to 80% to 90%. Most of the issue in becoming compliant is just about filing necessary paperwork which hasn’t been worth it to many companies relative to the very low tariff rates that apply under MFN status if they are not compliant to this point. The share of US imports from Canada paying duties has been rapidly falling with rising CUSMA/USMCA compliance (chart 6), but full compliance is likely to be difficult especially for smaller firms. A 35% tariff on the 10% to 20% share of Canadian exports to the US that would be difficult to be made US MCA compliant would amount to an effective tariff rate of between about 4% and 7% and likely on the lower end of that scale. This is in addition to sectoral tariffs (primarily metals). Therefore, if he were to go ahead, it could still be a meaningful hit.

PM Carney’s response on Twitter is here. He said Canada will continue to work toward a new trade and security arrangement with the US on a revised timeline of August 1st instead of July 21st.

I wish the PM luck. Trump is a died in the wool protectionist with a terrible understanding of Economics 101 and advised by “economists” that most economists don’t view as being credible. Trump wants tariff revenues as a tax on ordinary Americans in order to fund some of his tax cut to relatively wealthy individuals which makes no sense. US tariff revenues in the short-term face a self-destructing path over the longer term by crushing trade if Trump carries through on his threats against various countries. It’s Americans who will pay the tariffs and suffer higher prices, reduced employment prospects, and a weaker economy as a result. That’s not a recipe for attracting investment.

CANADIAN JOBS UPDATE

Canada updates the Labour Force Survey for June this morning (8:30amET). My guesstimate is for a gain of 15k and unchanged unemployment rate of 7% with consensus at 0% and 7.1%. It’s hardly a high conviction call.

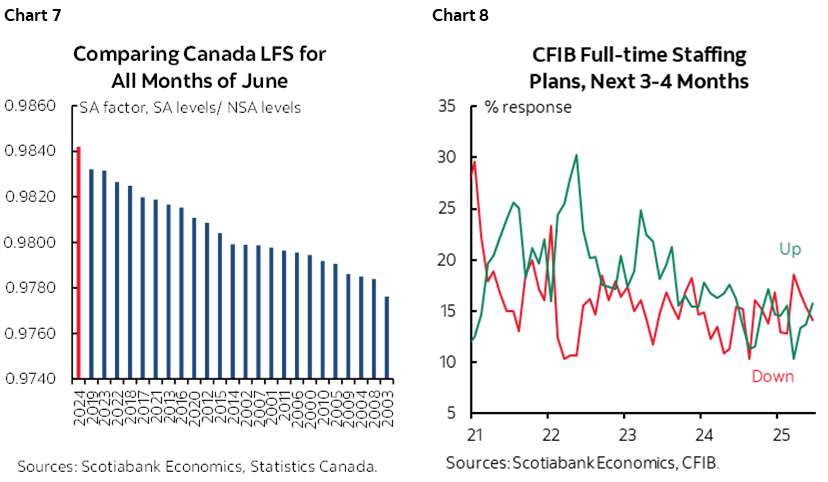

Seasonal adjustment factors are likely to bias the estimated change higher all else equal (chart 7). May was a miserable month for Spring weather and that may have been partly responsible for holding back categories like construction and hotel and food services, so weather effects might drive a rebound in June. Small business hiring attitudes have improved somewhat of late (chart 8). The lost election jobs in May after the surge in April will shake out as an influence; excluding election jobs that aren’t real jobs anyway (versus temporary employment for folks who at best are marginally attached to the workforce), employment was up 41k in May against fears of a tariff hit as services hiring carried the day which could repeat. As for the unemployment rate, timing the effects of tighter immigration policy on labour force expansion is difficult but on a trend basis should be a moderating effect.

This is the last set of job market readings before the July 30th BoC decision. When Macklem has emphasized data risk, it has been more about the next two CPI reports before the July decision more than other readings. Cue CPI next week that I’ll preview in my week ahead later today.

LITTLE MARKET REACTION TO WEAK UK DATA

UK data was generally weaker than expected but had little impact on local markets perhaps because they are stale readings and because Trump’s renewed tariff threats against multiple countries and sectors is dominating market interest. GDP fell -0.1% m/m in May (+0.1% consensus). Industrial output fell 0.9% m/m (-0.1% consensus) due to a 1% drop in manufacturing output. The services index grew 0.1% m/m as expected and was revised to be a little better in April (-0.3% instead of -0.4%). Construction output declined by 0.6% m/m (+0.2% consensus) with a small negative revision. The trade deficit narrowed with positive revisions as exports climbed but imports slipped.

Peru’s central bank held its reference rate unchanged at 4.5% as widely expected by most.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.