ON DECK FOR WEDNESDAY, JANUARY 8

KEY POINTS:

- Risk appetite sours after another tariff tape bomb

- Trump adviser indicates using national security provisions to justify universal tariffs

- FOMC minutes may pit staff economists against FOMC members

- Fed’s Waller sounded somewhat unrealistic

- Fade US initial jobless claims that fell to their lowest since last February

- ADP offered nothing of use to nonfarm expectations

- The economic case for why six million Danes should just laugh at Trump

- My core Trumponomics 2.0 market narrative is proving to be bang on

- US tariffs against Canada seem more probable by the day...

- ...and Canada has to be prepared to respond in kind

- Supply worries keep hammering gilts

- Chilean CPI keeps BCCh cut risk alive

- Australian trimmed mean CPI reinforces market pricing for the RBA to cut next month

- Germany’s economy is stumbling as Scholz’s polling suffers ahead of February’s vote

- Riksbank watchers keep leaning to –50bps after Swedish CPI

- Canada to auction 2s

- US to auction 30s

Data and headline tape bombs continue to drive high volatility in financial markets. Key this morning was this piece that quoted a Trump adviser saying that the administration is leaning toward using the International Economic Emergency Powers Act and Section 301 provisions to justify widespread “universal” application of tariffs across all countries. This is exactly what I had been saying they could wind up doing in writings since last Fall. The headline prompted lower equities and higher Treasury yields until a dubious combination of data (ADP, claims) and Fed-speak (Waller) came in. Canadian government bonds are broadly underperforming US Ts likely on retaliation concerns and effects on inflation but ahead of a key 2s auction. Gilts are selling off again largely on supply concerns and following another weak auction for 5s; the gilts curve is bear steepening with yields from 5s through 30s up by 6–10bps.

FOMC Minutes May Pit Staff Economists Against FOMC Members

Minutes to the December 17th–18th FOMC meeting arrive at 2pmET. A recap of the hawkish sounding 25bps cut that was delivered at that meeting is here.

Key may be whether the Fed staffers call bogus on the FOMC members as they issue their own forecasts. Staff economist projections are always included in the minutes versus the game day SEP that contains the views of Committee participants. We heard back on December 18th and through comments from officials afterward that some of them incorporated their own assumptions on likely US policy risks surrounding the incoming administration, some didn’t, and some did so only partially. There have been times in the past when staff economists went further and so we could get meaningful differences in projections versus the somewhat more politicized views of FOMC officials. During Trump 1.0, for example, staff economists went further than the Committee in terms of incorporating tariff assumptions. If they do that again, then there could be some headline grabbing forecast differences this afternoon.

Other than that, expect more of the content we got in December around the reasona for a hawkish cut and less future easing and perhaps a bit more colour around why they adjusted the O/N RRP rate at that meeting instead of January (or later) as many had anticipated.

Fed’s Waller Sounded Somewhat Unrealistic

Fed Governor Waller gave this speech economic outlook this morning just before ADP. He said more Fed rate cuts will be appropriate, the US economy is on solid footings, and that tariffs won’t have a significant impact on inflation and monetary policy. Uh huh.

On more Fed cuts, he didn’t indicate how much more other than to indicate data dependency. But the key is that he’s among the dots that reset the rate path higher (ie: less cutting) in December as the median projection only has 50bps of cuts over all of this year. Waller may be among the 10 officials in the 50bps cut camp but all we can definitively say about his comment is that obviously he’s not the one dot that expects no further easing this year. More Fed cuts being advocated by Waller is guidance provided after he and others significantly tamped down projected easing.

On the US economy being on solid footings, we’ll just see about that. He’s emphasizing lagging backward data rather than the lagging effects of soaring yields and a soaring dollar along with the possibility of pulled-forward demand ahead of tariffs and what lies in the aftermath.

On the tariff effects, if the US imposes widespread tariffs on multiple countries, which seems likely, then Waller may be seriously underestimating the pass through effects in the context of an economy operating in excess aggregate demand that could result in severe supply chain disruptions and unmoored inflation expectations. Let’s please hope the FOMC learned a little more about the disruptive effects of damaged supply chains than when they ignored inflation’s rise until it was too late!

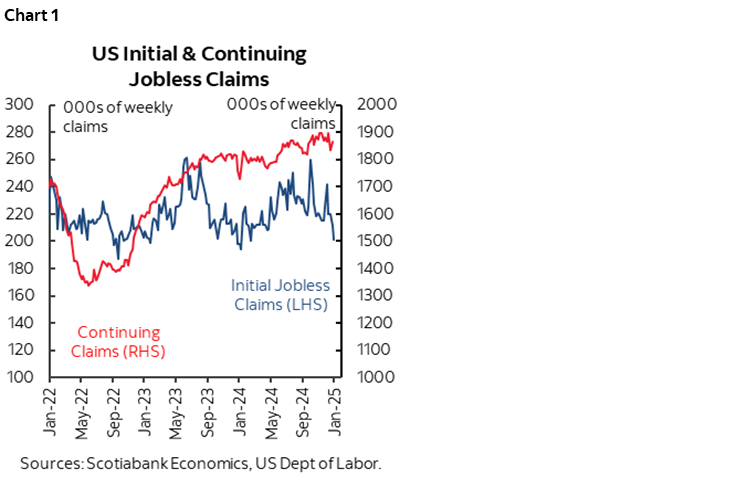

Treat the Drop in US Jobless Claims with Caution

US weekly initial jobless claims fell to 201k last week for the lowest reading since last February (chart 1). The modest drop seems genuine. Only Washington and Kansas were estimated and their movements don't explain the mild decline in overall claims. The figures are seasonally adjusted, but storms and shifting holiday timing from year to year still counsel caution in reading too much into the data.

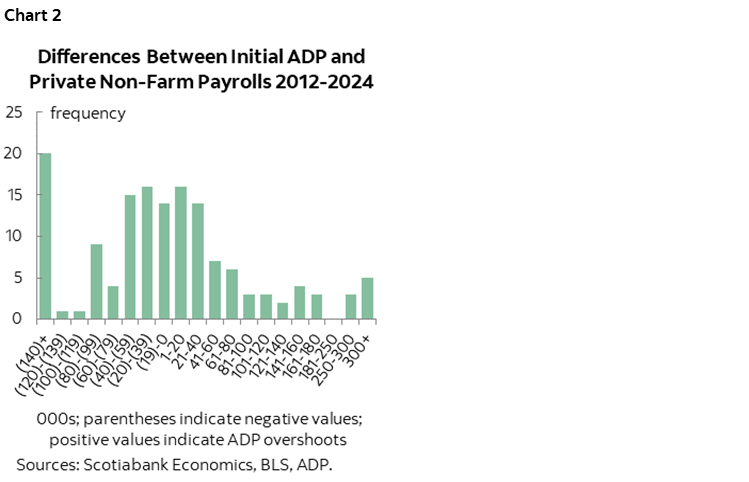

Fade ADP Payrolls

US ADP private payrolls were up by 122k in December which was a touch shy of consensus (140k) and my guesstimate (150k). Based on historical differences between initial ADP and initial private nonfarm payroll estimates, all we can say is there is about a 50–50 balanced chance whether private nonfarm payrolls land higher or lower than the consensus estimate of 140k for private nonfarm payrolls. Chart 2 shows the spreads and frequency of occurrences over time. ADP merely offers something to help pass the time as markets await Friday’s nonfarm payrolls. They often don’t line up with the private component of nonfarm payrolls and are a weak advance indicator. There can be times when sharp surprises by ADP can make it statistically improbable to hit consensus estimates for nonfarm, but even then, it’s often not the case.

Canada to Test Appetite for its Bonds

Canada auctions C$5.5B of 2s at noon today. The 2s bid-to-cover has risen in recent auctions and yesterday's mild cheapening makes them a touch more attractive and with nothing else on the domestic calendar. That said, the tariff threat makes strong conviction hard to come by imo. US tariffs for a meaningful period of time and in the absence of retaliation make it more likely the BoC eases more aggressively, but meaningful retaliation would not and could conceivably pivot the risk in the other direction. Right now, 2s are priced in the ballpark of neutral without much of a term premium if any which may be about where they should be for now until we know more and probably fairly soon.

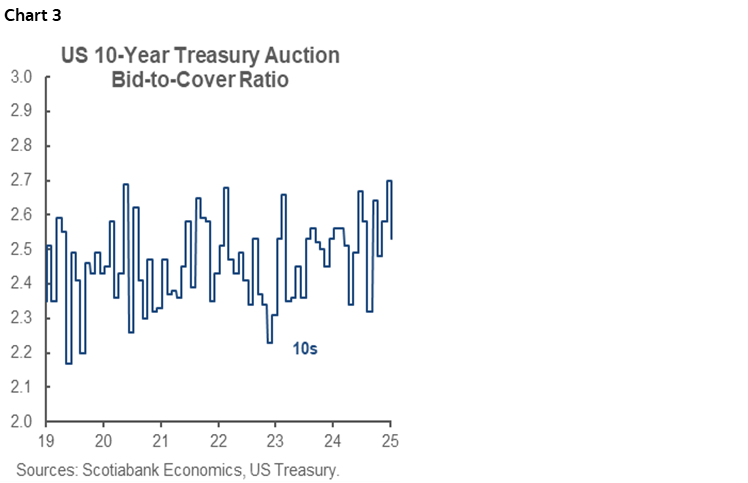

US 30s Auction on Tap

The US will auction US$22B of 30s in a reopening at 1pmET today. This follows yesterday’s 10s reopening that had little effect on yields after a combination of solid US data (ISM-services, JOLTS) and Trump’s presser drove higher yields and despite a weaker bid-to-cover (chart 3).

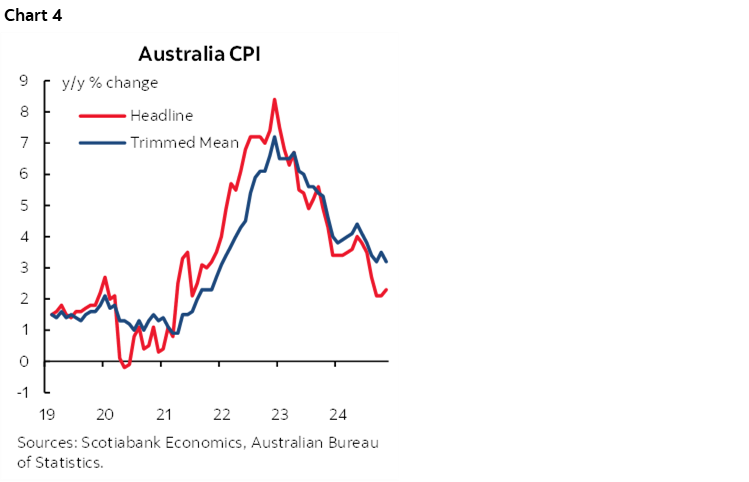

Australian Inflation Reinforces RBA Easing

Aussie core CPI cooled a touch to 3.2% y/y in November from 3.5% previously even while headline inflation was up by 2.3% y/y (2.1% prior, 2.2% consensus) as total prices were up by 0.5% m/m SA. What drove the m/m total CPI rise was a 22.4% m/m jump in electricity prices that were previously falling at a rapid pace for four months. What drove this jump in electricity prices was a return to one rebate installment per household in several territories in November instead of two the prior month. Ergo, fade the headline number and focus more upon trimmed mean that in y/y terms is inching closer to the RBA’s 2–3% headline inflation target range (chart 4). That’s what markets did while putting a bid the Aussie front end.

Germany’s Economy Is Stumbling Into the Election

German macro data was soft ahead of next month’s election that has Chancellor Scholz’s party on the run. Factory order volumes plunged by -5.4% m/m. It's lagging data for November and so maybe any pulled-forward ordering before tariff wars will show up later. Retail sales volumes fell by less than a expected net of revisions. They fell by -0.6% m/m in November and by an upwardly revised -0.5% in October (previously -1.5%).

Riksbank Pricing Continues to Lean Toward a –50bps Cut

Riksbank watchers liked what they saw in Swedish inflation that surprised a little lower than expected. Headline CPI was 0% m/m (0.2 consensus), underlying CPI was 0.3% (0.4 consensus) and underlying ex-energy was 0.4% (0.5 consensus). The 2a yield fell below 2% and markets are leaning further toward a 50bps cut on January 29th.

Chilean Inflation May Extend BCCh Easing

BCCh watchers digested a weaker than expected CPI report that saw prices fall by -0.2% m/m in December (0% consensus). CPI ex-fruits, vegetables and energy also fell by -0.1% m/m. Last month’s hawkish sounding 25bps cut by BCCh may have made a pause more likely on January 28th but this could be called further into question now.

Six Million Danes Should Just Laugh off Trump’s Threats

Who picks on Denmark?? Of all the places in the world with whom to pick a bun fight, you couldn’t have chosen a worse target if you tried. But Trump did just that with his threat to impose tariffs on Denmark if it doesn’t hack up Greenland. Talk about blackmail, minus the need for it to be a credible threat. The US wants Greenland for its critical minerals and for strategic reasons that mostly mean having China and Russia keeping their mitts off it.

If I were Denmark, then I'd just laugh off Trump’s threats. Ditto for Greenland.

That’s because tariffs wouldn’t do much to Denmark for two broad reasons. One is minimal trade exposure to the US. Denmark only exports about 5% of its total exports to the US and the US accounts for a similar share of Denmark's total imports. That’s not at all like Canada's exposure to the US, or Mexico’s. European countries dominate Denmark’s trade account. The US ranks high among Denmark’s trade partners in dollar terms but is a minimal share of overall Danish trade.

A second reason is that Denmark has an independent central bank with its own currency. I’m sure when they opted into the EU but not to the Eurozone that it wasn’t because they were clairvoyant and foresaw Trump coming at them, but rather something more to do with optimal currency areas and independence. The krone has already depreciated by about 6–7% to the dollar since early October as a middle of the pack performer amid broad dollar strength. It's weakening again today.

The Core Trump Thesis Is On Track

One of my core theses has been that expansionist fiscal and regulatory policies by the incoming Trump administration would likely be sterilized by a combination of the Fed and markets through bond yields and FX. Applying fiscal and regulatory stimulus to an economy in excess aggregate demand would aggravate inflation and supply worries and in a way that could short circuit future growth while large spending cuts to offset tax cuts are highly unlikely to be delivered. Tariffs would raise US inflation risk.

I didn't think it would happen quite this rapidly though. The 10s yield is up by 110bps from September, some of which through higher inflation expectations, some through the term premium that in 10s is at about a ten-year high. The DXY has appreciated by about 9%. The S&P is about 3% off the peak to now being roughly flat to the Nov 5th election date. Cumulative easing by the Fed by the end of 2025 has been scaled back by about 120bps compared to September.

The question now is whether all of this has gone far enough, too far, or just about right. I think it has more room to run as reality sets in on Trumponomics 2.0 and can see a march to 5% before the picture becomes complicated when the debt ceiling becomes binding with effects on supply scarcity and abundant liquidity, and data possibly begins to sour in lagging response to tightened financial conditions and the aftermath of what may be pulled-forward demand.

On the latter, I’m not totally sure that’s what is behind some of the recent data. The theory is that to get ahead of tariffs, consumers and businesses may be buying more now before prices jump and this may be evident in measures like PMIs and auto sales. That may be more likely to be happening among purchasing managers (hence going to inventories) than consumers since I think US consumers are largely clueless toward the prospects of higher prices through tariffs. Further, they’d be financing this brought-forward demand at higher borrowing costs both because of scaled back Fed easing and higher term borrowing costs. If it’s just a purchasing manager effect to stockpile inventories at today’s prices, then inventory depletion later on could weigh on growth—or they’ll be stuck with inventories that are costly to finance and store.

US Tariffs Against Canada Seem Very Likely as the Alleged Justification Keeps Changing

The fact that Trump keeps changing the reasons for applying tariffs against Canada is as sure a sign as any that he’s determined to do so. One minute it’s because of border security concerns that I’ve argued from day one to be a ruse given the facts on fentanyl and migrants. The next minute it’s because of the US trade deficit with Canada with factually incorrect and inflated numbers that he keeps changing and that ignore the fact the deficit with Canada doesn’t exist if oil is taken out and the US needs Canada’s oil. Then it’s because he has odd dreams of annexing Canada by economic force as the 51st state that is plain and simple hubris to the nines. Fat chance buddy.

At the heart of Trump’s tariff beliefs are two more consistent, but unreasonable arguments, and quite possibly a more realistic third one. One is that he wants a narrower US trade deficit, but he doesn’t understand what is driving the US trade deficit and the dangers associated with policy measures that seek to narrow it. Two is that he mistakenly argues that tariff revenues can replace income taxes. Three is that he’s just playing victim politics with little regard for the economic consequences to America and the world.

On the US trade or broader current account deficit, it exists a) because of the attractiveness of investment in the US that drives outflows of investment returns, and b) because the US spends a lot, both in terms of consumers and governments. Don't want as big a current account deficit? It’s simple, just don't spend as much, or raise taxes. Reduce bloated fiscal deficits and keep going by addressing the time bomb that is the unfunded social security obligations that Canada fixed with the CPP in the 1990s while preserving small deficits as a share of GDP and a AAA credit rating one notch above the US today. Those are problems of America's own making and not anybody else's fault. Sooner or later America will be forced to address its profligacy but that appears unlikely in the near-term.

If through tariffs of quotas or other tools the US tries to close the trade deficit, then other things in the system will adjust and break. Like the effects of trade diversion and substitution with less product choice and at higher prices particularly since the US economy is already operating in excess aggregate demand with a positive output gap which means domestic business has little to no ability to crowd in the costlier imports. For another, the flip side of the current account deficit is the capital account surplus to fund it. ie: foreign buying of US securities, namely Treasuries. Mess with one side of the ledger, mess with the other and accept the consequences to US financial markets.

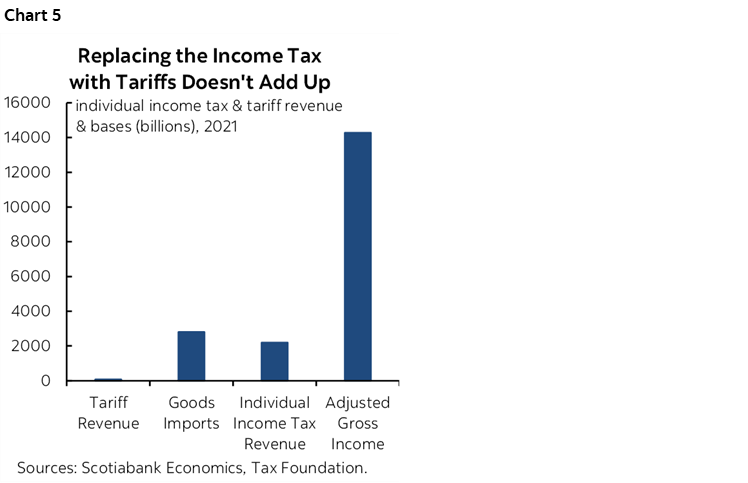

And on using tariffs to fund the replacement of income taxes, the math comes absolutely nowhere close. Imports are a vastly smaller tax base than domestic incomes. Even if you hiked tariffs to 100% and wrongly assumed imports wouldn't decline then you would still not come anywhere close in the math to funding replacement of income taxes. Good luck replacing over US$2T of income tax revenue with tariffs (chart 5).

And on the third possible argument, it is my firm belief that Trump requires victims and a blame game regardless of the merits of the arguments. It’s also feasible that the strategy is to create maximum geopolitical risk across multiple theaters by bringing in Canada, Mexico, Panama, Denmark, Greenland etc in order to lessen the focus upon Russia, Ukraine and Iran. Putin’s just loving the collapse of the GOP.

The most stunning thing about Trump’s threats, however, is how deathly quiet American business has been about it. Either they’re afraid to speak out, or they support the measures without understanding how potentially devastating the effects could be them. Either way, to date, free trade appears to have few if any allies in the US. That also makes the tariff threat more likely to be delivered upon in the absence of significant domestic opposition.

Canada Needs to be Prepared to Escalate Its Game Against Trump

So what should Canada do about tariffs given that they are very likely to hit? I'll give two answers and remind folks of where I lean.

The traditional economist response is to just take it. Don't retaliate. You'll make things worse. Tariffs on US imports into Canada will drive prices higher, squeezing purchasing power, imposing further damage on consumption, business investment, growth, unemployment, etc. An ugly situation would be made uglier.

Now go to the local playground. Spot the kid being picked on the most each and every day and who does nothing about it. That picked on kid’s gonna be an economist one day. That's what this traditional take basically says.

And it’s not what I believe, nor how I think a sovereign nation should deal with an administration like the one taking power in the US. Just taking it might be more appropriate if this is a one-off occurrence for a short time that allows CAD and other effects to adjust and then it all goes away. That’s not what I think we’re facing here.

So what to do? In a multi-sequenced game theory sense with years of this ahead of us and being played against a seemingly highly irrational regime, you have to dig in and play the longer game. If you don't stand up now, you'll get your lunch stolen from you each and every single day. Pushed down in the playground over and over. Tariffs ad nauseam and other punitive measures. The goal is to destroy the attractiveness of investment in Canada for the long haul through successive punitive measures without thinking through the consequences for the US because the US administration thinks that it will get the spoils. That cannot be allowed to happen for the sake of longer-run generational prosperity.

Canada stood up in Trump 1.0 with retaliatory tariffs. Canada stood its ground in NAFTA 2.0 negotiations. Trump backed down almost entirely from his original demands and went out with a whimper as Freeland’s team competently stood its ground. It was made clear that Canada would punch back. It worked.

The stakes are far higher now. Trump 1.0 was mostly about metals tariffs and Canada retaliated with proportionate targeted tariffs starting on Canada Day and lasting until the next May. This time it’s not about just targeting Kentucky bourbon or yogurt made at a plant in Paul Ryan’s home state.

You've got to make it very, very clear to US businesses that Canada will not roll over and to raise awareness of the consequences to what is so far a checked-out US business community. Bourbon won’t cut it this time. That requires causing maximum upheaval across US supply chains and turmoil into US mid-terms, waking up US businesses, and forcing the GOP senators and representatives in all the states that declare Canada to be their #1 trade partner to explain the turmoil to voters as shifts potentially get suspended, plants shut, layoffs occur etc. The incumbent always suffers a setback into mid-terms. Make it more so this time. A lame duck President into the second half of this mandate if not before as the GOP spends 2026 on the run.

Then sit back and let US domestic pressure reawaken and be applied against the administration with US businesses, workers and consumers leading the charge. That’s also what happened the last time around as the US business lobby took over Washington’s hotels including Trump’s. Otherwise, it will be four years of this over and over and over at much greater longer-run cost to the economy and the welfare of Canadians. Make yourself someone who is easy to pick on and you'll be picked on over and over.

Strong retaliation would add to the pain of US tariffs against Canadian exports in the short-term which is hugely unfortunate and hopefully we find another way as the best option to avoid all of this. I haven’t given up all hope that a better way can be achieved if not by avoiding tariffs, then by only having them for a short period, but it’s looking more likely that the threat is larger and longer in nature. If so, then you've got to dig in and play the longer game. Mexico the same. And be prepared with a bevy of support measures ready to roll out immediately across provinces and the feds.

All of this is just my personal opinion but I’m much less convinced that the way to go is with the traditional economist's advice in this instance because of the nature of the threat and the danger of the threats becoming serial in nature at much greater long-run than short-run cost. I also don’t think it’s politically realistic to assume that Canadian governments—federal and provincial—will not respond which makes it practical to consider the risk of bigger retaliation. They may well turn the other cheek, but not that one…

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.