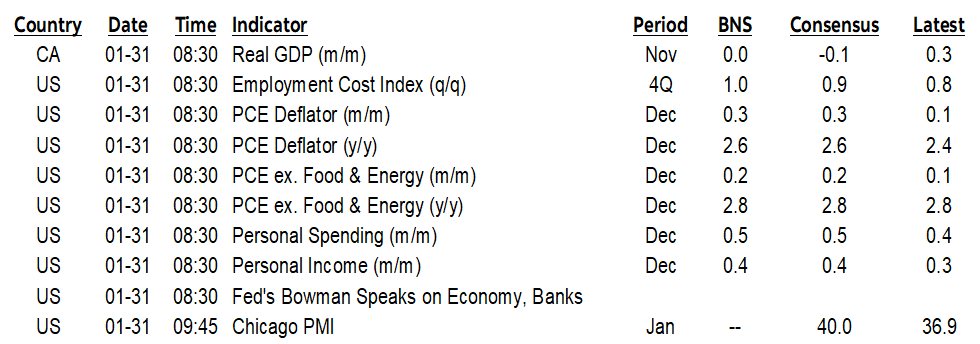

ON DECK FOR FRIDAY, JANUARY 31

KEY POINTS:

- CAD, MXN hit by reinforced tariff threat

- There is extremely high support for retaliatory tariffs in Canada…

- ...and it’s political suicide in an election year to ignore that…

- ...making retaliatory tariffs and support packages highly likely…

- ...as negotiations against the US administration’s motives are looking pointless

- Eurozone inflation is tracking softly, bolstering further ECB easing

- Tokyo core inflation was firm, but a mere placeholder

- Canadian GDP: Soft November, possible upside in December?

- US core PCE: a second soft month proves nothing to the Fed

- US consumer spending and income gains were probably decent to end 2024

- US employment costs probably climbed significantly in Q4

- Will BanRep cut? Consensus is divided

You made it. It’s month-end, which sometimes in markets is a big deal for portfolio rebalancing effects. Only a month? It felt like a year in some respects. This month-end coincides with significant calendar-based and off-calendar risk.

There are big moves in some markets to consider and a lot of data on tap into the N.A. session. CAD instantly depreciated by almost a cent when the headline hit just before yesterday’s close that Trump was going to go ahead with tariffs on Canada and Mexico on Saturday and is working on China tariffs. MXN also depreciated. Neither currency is close to fully incorporating tariff effects including retaliation. USDCAD has been largely sleepwalking since mid-December around the 1.44 zone in the hope that tariffs can be avoided and now that looks unlikely.

Further, EGB yields are pushing lower across the board after soft data on inflation and activity readings.

Stocks are rising across the board. Apple’s earnings helped out after the close. Stocks are nominal price gauges and so inflationary tariffs help pricing power in some industries and some countries—at least until the consequences shine through.

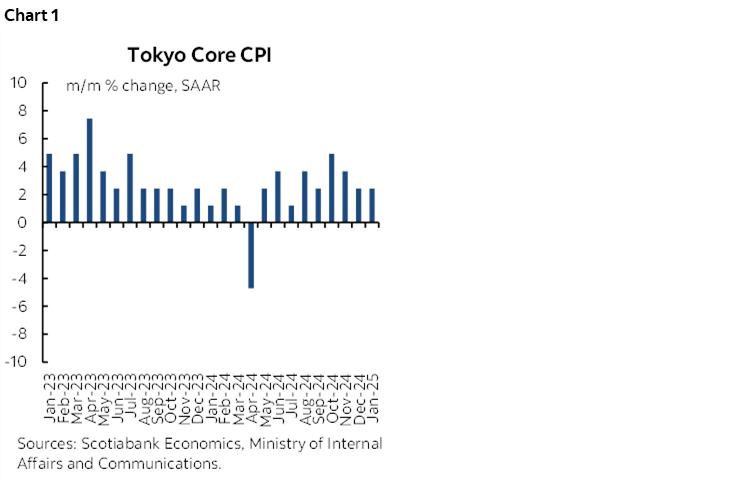

Tokyo Core CPI—Scorekeeping

Tokyo CPI climbed to 3.4% y/y in January from 3.1% (consensus 3%), CPI ex-fresh food was up 2.5% y/y (2.4% prior, 2.5% consensus) and ex-food and energy was up by 1.9% (1.8% prior), matching consensus. At the margin, CPI ex-food and energy was up 0.2% m/m and 2.4% m/m SAAR for a second straight month (chart 1).

There are no direct implications for the Bank of Japan with another possible hike likely several meetings away and data merely keeping score in the meantime.

Eurozone CPI—More Disinflationary Evidence

We don’t get the Eurozone tally until Monday along with Italy’s component, but this morning, Germany and France delivered dovish readings that fanned a rally in EGB yields.

French EU-harmonized CPI slipped -0.2% m/m (-0.1% consensus).

German states’ CPI readings were already pointing to a soft national release before it landed at –0.2% m/m SA, matching consensus on an EU-harmonized basis. Of the six states that released, four saw CPI decline in m/m terms, one was flat, and the other was up a tick. Consensus is for national EU-harmonized CPI to be -0.2% m/m.

Other data also fanned lower yields. Germany retail sales volumes fell 1.6% m/m in December (consensus 0%) with most of that being a surprise and part being due to an upward revision to the prior month (0% m/m instead of -0.6%).

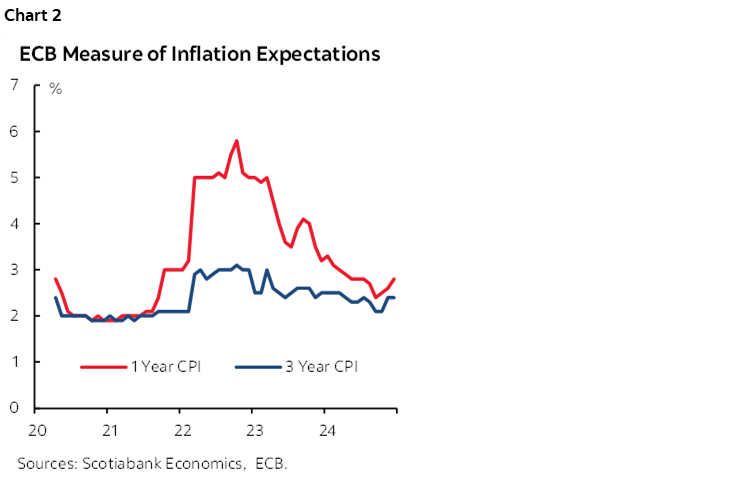

Further, the ECB’s measures of CPI expectations inched a little higher in the short-term. The 1-year measure was up two-tenths to 2.8% and the 3-year measure was flat at 2.4% (chart 2).

Markets are priced for another cut and then some at the March 6th ECB meeting and on the fence between 75–100bps of cuts by year-end.

Canadian GDP—Did Canada End the Year on a Higher Note?

We’ll get GDP for November and December this morning (8:30amET). Who cares with tariffs and retaliation looming. November was initially guided by Statcan to be down -0.1% m/m back on December 23rd. Most economists are at -0.1% m/m or 0% and I’m in the latter camp. The bigger issue may be early guidance for December. Gains in hours worked and a variety of indicators including consumer spending point to a healthy gain but with many unobservable components. The BoC’s revised Q4 GDP forecast of 1.8% q/q SAAR on an expenditure basis may be low compared to monthly production-side GDP account tracking.

US Core Inflation—A Mere Footnote to a Fed on Hold

Headline PCE is expected to rise by 0.3% m/m SA and 2.6% y/y (2.4% prior) and core PCE is forecast to be up by 0.2% m/m SA and an unchanged 2.8% y/y (8:30amET). I went over the estimates in the weekly including conversion of CPI to PCE weights and incorporation of the PPI components that matter to PCE. Too bad this reading doesn’t matter, at least not for the foreseeable future with the Fed saying it’s on hold for a while.

US Consumer Spending and Incomes—How Good Was the Holiday Season?

Solid consumption and income gains are expected this morning (8:30amET). December’s readings are expected to post 0.4% m/m income growth and 0.5% m/m spending growth. The 0.7% m/m SA rise in the retail sales control group that month is the ingredient for the consumer spending call along with an expected decent services gain. Consumption estimates range from 0.4% m/m to 0.7%. Given what we may know about inflation, this could translate into a modest real consumption gain.

US Employment Cost Index—Upside Risk?

The ECI for Q4 (8:30amET) is expected to accelerate again with consensus at 0.9% q/q SA nonannualized and several of us are at 1% (Scotia) or higher. Firmer wage growth in q/q terms might support such a call.

BanRep—Cut, Or Maybe Not

24 out of 32 economists in the Bloomberg consensus expect Colombia’s central bank to cut its overnight rate by 25bps today (1pmET). Scotia’s Jackeline Pirajan Diaz is in the hold camp.

When it Comes to US Tariffs, Expect Retaliation

And tariffs will be met with retaliation. Have the debate, but be pragmatic.

For starters, there is extremely high support for retaliatory tariffs across Canadian businesses—including in Alberta (here). The survey questions indicate that businesses are aware of the consequences and support strong fiscal policy supports. This adds to an earlier poll by Ipsos-Reid of Canadians in general that showed 82% support for retaliatory tariffs (here).

It’s an election year in Canada. Ontario goes to the polls in about a month. A Federal election beckons in May. The NDP is saying they’ll hold off on bringing down the government in a confidence vote when Parliament returns on March 24th long enough to pass a stimulus support package. Canadian politics will not cripple the ability to respond. The stimulus and support package is probably ready to hit ‘send’ on. The dark positive of the pandemic, if you can call it that, is that it made Canada ready for a future shock like this. The experience of rolling out whatever it takes from job and income supports to targeted stimulus to households and businesses to supporting facilities is still fresh on the minds of the politicians and bureaucrats who enacted it all.

Reality may also be starting to sink in across the US audience. On that note, it was refreshing to see an American economist speaking candidly about how bad the effects of tariffs and retaliation would be on the US itself compared to a lot of the indifference and pollyannaish nonsense. Most Americans don’t even seem to know their most important trade partners are in NAFTA. Adam Posen—President of the Peterson Institute and past external member of the BoE’s MPC among other accolades—correctly highlighted for Bloomberg TV viewers two concerns. One is that he noted it’s not just a one-off price hike via tariffs as he emphasized deep ripple effects of tariffs throughout highly integrated supply chains that could well cause pandemic-style shortages; this is what I’ve been arguing. Two is he expressed the fear that the Trump administration is moving toward incorporating tariffs into a budget as a permanent source of targeted revenue which is a game changer that reveals what this US administration is all about. Maybe the American audience is started to wake up to the consequences.

Navarro made the same point this morning on CNBC, saying that the goal of the US administration is to replace revenue sources with tariffs which signals moving toward incorporation into budget proposals as a broader package.

In that case, Canada has to take the fight to US consumers and US businesses and bypass the US administration. Raise awareness of the costs to American businesses, American consumers and American voters. There is no choice when all the signals from this US administration are indicating a highly insular, protectionist and isolationist stance on everything to do with international relations from trade to climate policy to healthy policy and immigration. The ideology guiding this US administration will not be swayed by facts, by jumping through hoops on the alleged reasons for tariffs. Canada, Mexico, China, Europe, and whomever else have to make it clear to Americans what the costs to this approach will be.

And enough with humiliating ourselves by running around hopelessly trying to appease this US administration. Trump’s latest malleable justification for tariffs goes like this:

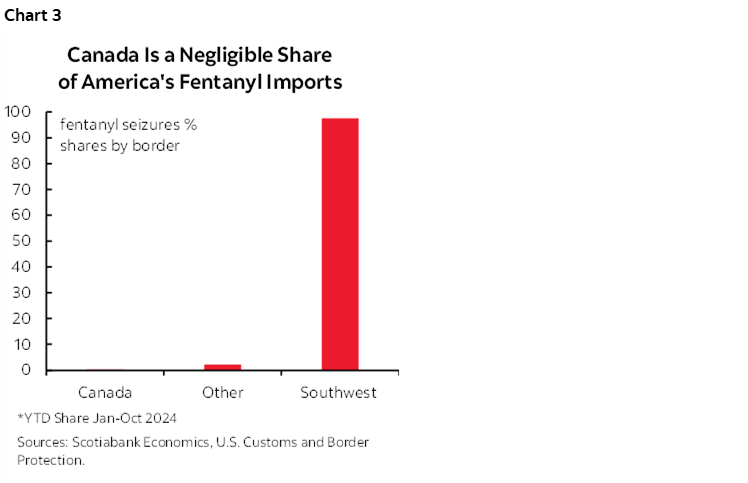

- To make Canada address its fentanyl export problem. This is a lie, backed by US data itself (chart 3). When Canada finds a fentanyl plant, it shuts it down, and the plural of anecdote last I checked isn’t data. It’s a small issue on the Canadian side and instead of confronting its domestic drivers and doing something about it, the US administration is sloping off blame onto Canada. Blame is the one thing that is in abundant supply in Washington.

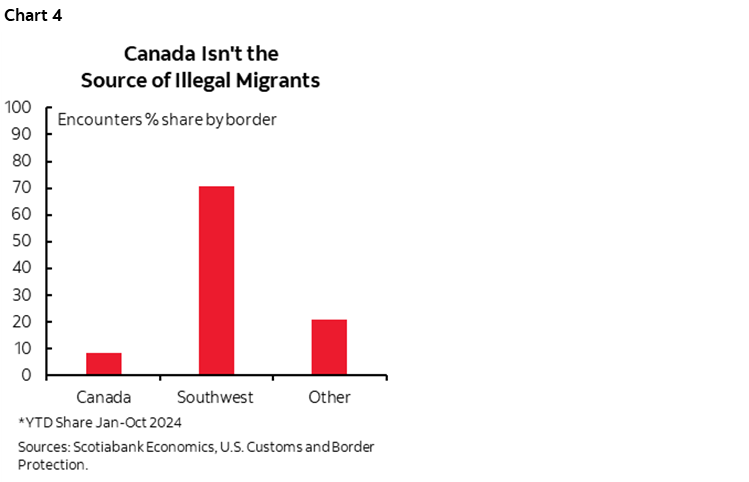

- To make Canada address its cross-border migrant problem. This too is a lie, backed again by US data (chart 4). CBC cameras that spot a half dozen scurrying across the prairie border in the dark of night are not data. Anecdotes don’t prove a large problem. And the bigger problem is likely to be in the other direction if the US fails to properly secure its side of the border against what could be a rush of migrants hopping across as the US tightens immigration policy. Canada also has concerns about lax US border controls around the issue of illegal gun exports to Canada that every policy association in the country pinpoints as the source of guns used in crimes.

- To address Canada’s trade imbalance with the US. Lie #3. Trump claims a $200–$250 billion Canadian trade surplus with the US (the number changes all the time). Try more like $50–60B zone. Take energy out, and Canada runs a trade deficit with the US. And I would say the US administration needs to understand what drives trade balances and causes them but that falls on deaf ears.

I’ll write about the case for retaliation in my weekly as a reminder of my views. The case remains strong.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.