ON DECK FOR THURSDAY, JANUARY 30

KEY POINTS:

- EGB yields fall on weak GDP ahead of ECB

- ECB to cut, and stay on easing path amid uncertainties

- Eurozone GDP disappointed across all major economies

- The key to Lutnick’s remarks was to offer Trump a face-saving offramp…

- ...though ‘show us some respect’ was rather rich!

- Spanish core CPI signalled warmer pressures at the margin

- Macklem held his punches yesterday to avoid disrupting Canada’s tariff response

- US GDP may face downside risk, but key will be final domestic demand

- US core PCE inflation probably picked up in Q4 ahead of December’s reading

- Mexico’s economy shrank more than expected in Q4

- Canadian small businesses signal resilient hiring and inflation expectations

- More ‘Magnificent 7’ earnings on tap

EGB yields are lower and outperforming US Treasuries as they fell in the wake of disappointing Eurozone GDP figures but be careful with Spain’s core CPI that kicked off Eurozone estimates. The euro is underperforming most other major crosses as well and ahead of the ECB’s expected cut. Stocks are resilient and posting gains everywhere despite mixed but generally soft results from US ‘Magnificent 7’ stocks in yesterday’s aftermarket. There is no follow through from yesterday's FOMC and BoC decisions but I think Macklem held his punches for political reasons (see below).

Today’s heavy line up is going to be dominated by the ECB’s expected cut and forward guidance, US Q4 GDP that is likely to be strong, US Q4 core PCE that is expected to pick up ahead of the next day’s December reading, Mexican GDP and more ‘Magnificent 7’ earnings from Apple, but also with Intel out.

The Eurozone Economy Stalled Out in Q4

Eurozone GDP disappointed by coming in flat in Q4 (0% q/q SA, 0.1% consensus). Chart 1 shows the first zippo reading in a year. France (-0.1%, 0% consensus), Germany (-0.2%, -0.1% consensus) and Italy (0%, 0.1% consensus) were all weaker than expected (chart 2).

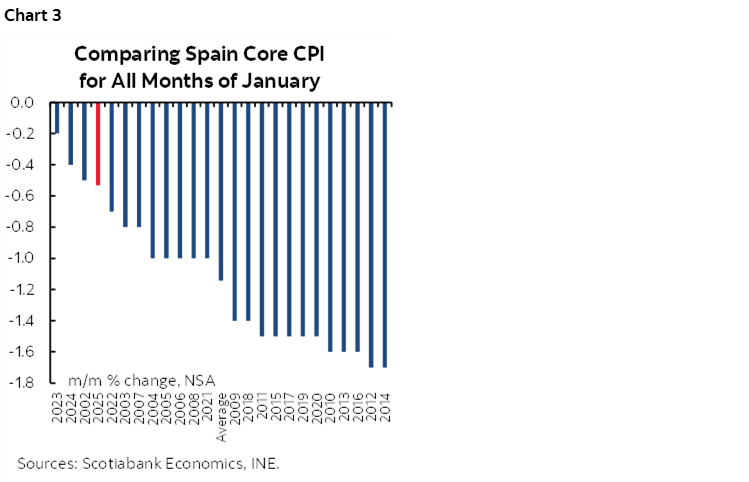

Spain Kicked Off Eurozone CPI Tracking in Mixed Fashion

Spanish CPI kicked off Eurozone tracking ahead of France and Germany tomorrow and then the Eurozone tally on Monday. Spanish core inflation was a touch lower than expected (2.4% y/y, 2.5% consensus) but in m/m terms the -0.4% NSA drop was warmer than for a usual month of January which suggests firmer pressures at the margin (chart 3).

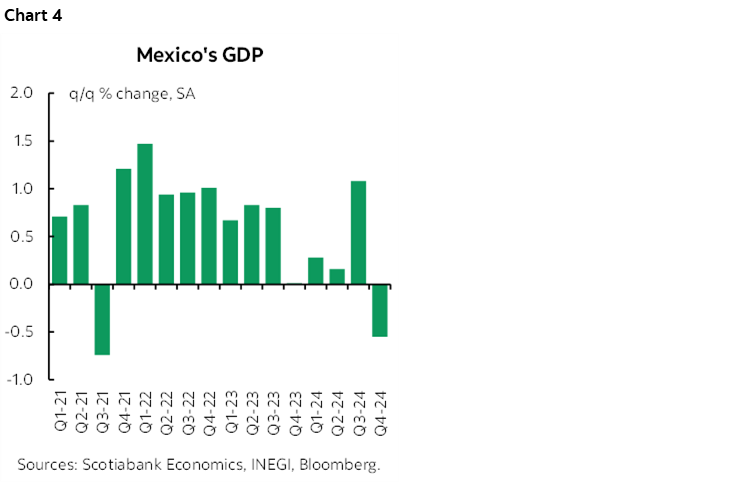

Mexico’s Economy Contracted More than Expected

Mexico’s economy contracted by triple the expected pace in Q4. GDP was down -0.6% q/q SA nonannualized (consensus -0.2%). That’s the first contraction since 2021Q3 but it follows the 1.1% q/q SA nonannualized surge in Q3 and so some give back was expected (chart 4).

ECB to Cut, Probably Signal Further Easing

The ECB is universally expected to cut this morning (8:15amET). It’s the guidance and forecasts that will matter particularly including what comes out of Lagarde’s press conference (8:45amET). There is room to ease given Governing Council’s confidence it is on track toward achieving 2% inflation in the near term and with the 3% deposit rate about 100bps above a neutral rate estimate. With growth stumbling, an easing bias is likely to persist today. Trump’s threat that “they’re going to be in for tariffs” hangs over confidence in their inflation forecasts and will be reassessed at the March 6th meeting. So may next week’s wage figures to be published on Wednesday.

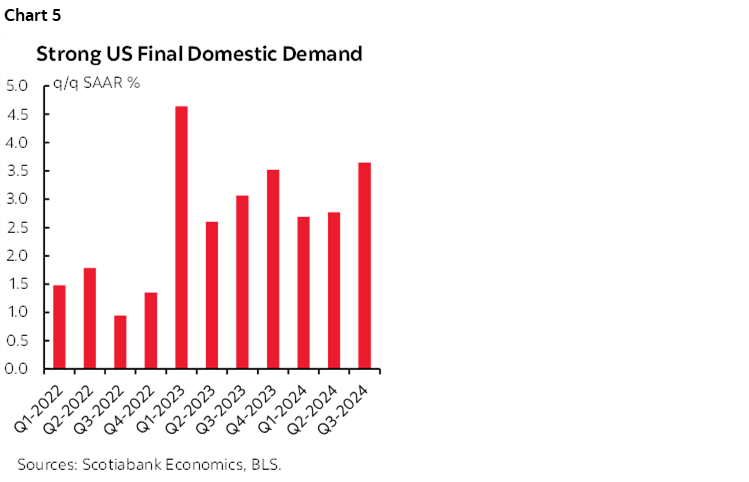

US Q4 GDP May Disappoint on Inventories, Imports—Watch FDD

Yesterday’s inventory and trade figures threw a bit of a spanner into the works insofar as estimates for today’s Q4 US GDP are concerned (8:30amET). Consensus sits at 2.6% q/q SAAR and Scotia’s estimate is 2.8%. The range runs from 0.9% to 3.2% with most clustered in the 2–3% zone. The Atlanta Fed’s ‘nowcast’ was updated yesterday to reflect the inventory and trade figures and was revised sharply lower to 2.3% from 3.2% as inventories fell and the US trade deficit ballooned. The nowcast doesn’t always get it right. Key may be to cut to the Final Domestic Demand figure that focuses upon the health of the domestic economy excluding inventory and net trade figures and that is expected to reveal solid growth in consumption which may matter the most. FDD has been very strong for the past seven and possibly eight quarters (chart 5).

US Core PCE Inflation Expected to Pick Up

Also keep an eye on US Q4 core PCE for Q4 (8:30amET). I’m at 2.4% with consensus at 2.5%. That’s using my 0.2% m/m core PCE estimate we’ll get tomorrow and assuming no revisions which there may well be. Because of possible embedded monthly revisions, you can never really tell if a surprise in core PCE on a quarterly basis tells you anything about December’s estimate that arrives tomorrow.

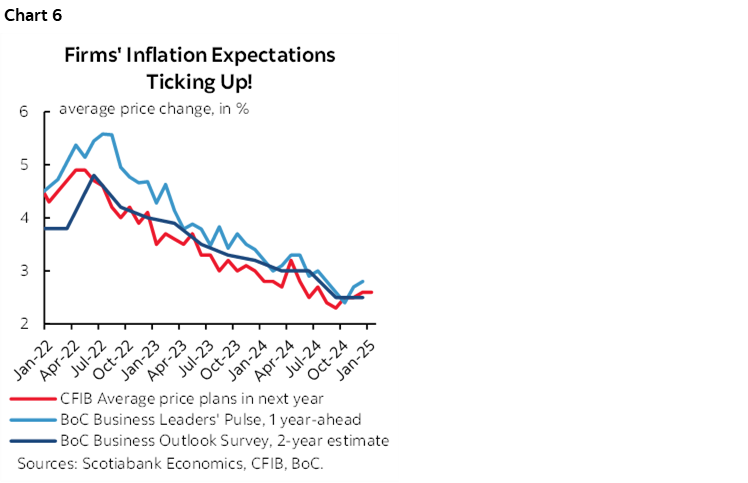

Canadian Small Businesses Signal Resilient Hiring and Inflation Expectations

Canadian CFIB small business confidence slipped a bit (54.6, 56.5 prior) but hiring and price plans were steady. Businesses expect to hike prices by 2.6% over the coming year which is unchanged, and the net hiring intentions measure improved with 14.3% saying they intend to hire more (14.7 prior) while 12.7% say they intend to decrease staffing (down from 16.8%). The inflation reading is fresher than the BoC’s gauges and signals persistent pressures (chart 6).

Canada also updates the SEPH payrolls measure for November (8:30amET). It’s a lagging indicator and only reflects payrolls which in Canada means it misses many small businesses. The wage figure will be the one to watch.

Why Macklem Held his Punches

With the benefit of some distance now I’m of the view that despite doing a good job in describing the ambiguities around how tariffs will impact the BoC, Governor Macklem held his punches. He was not as direct on the direction of rate risk in a tariff scenario as he could or arguably should have been because he didn’t want to disrupt Canada’s strategy in response to potential US tariffs. The headline he likely sought to avoid was about not cutting as much, if at all, and possibly hiking everyone’s borrowing costs if Canada retaliates in a big way and drives a surge of inflationary pressures. That might have undermined Canadian unity into the tariff threat.

At the end of the day, from one Governor to another, the BoC will always err on the side of partnering with the Canadian government based on years of monitoring their actions.

Lutnick Attempted to Provide a Face-Saving Tariff Offramp for Trump

Well, that was rich. US Commerce Secretary Lutnick has the nerve to tell Canada “Show us the respect, shut your border." Respect hasn’t exactly been a word that I would use to describe anything his boss has shown my country, though we have a lot of company in that regard. Further, the US can and should address its own northern border issues, like tightening inspections to stop the flood of illegal guns coming into Canada, and spending money on its own surveillance and enforcement. The US does a poor job of managing its own side of the border and is merely trying to offload costs onto Canada.

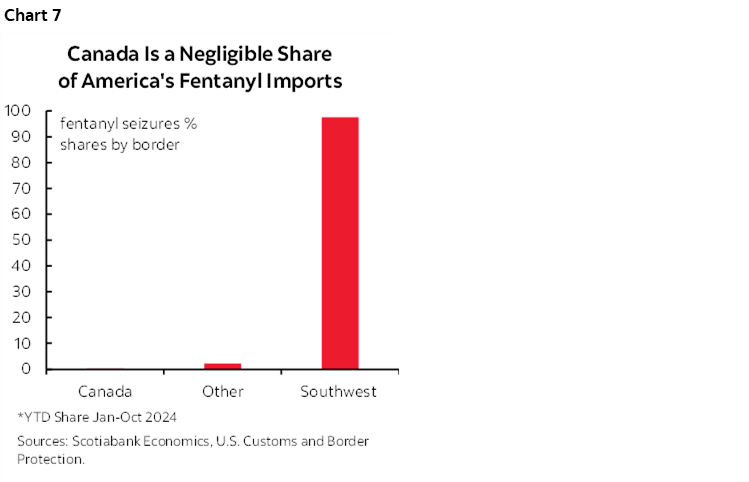

And yet I think the main takeaway from Lutnick’s remarks yesterday was that he may have been trying to set up a face saving offramp for Trump to back off his ruinous tariff plans. He claimed that the 25% tariff threat this weekend is oriented toward getting Canada to stop the flow of fentanyl into the US. Regular readers know that’s absolute rubbish as Canada is a trivial source of this problem for the US using US data (chart 7)! Regardless, Lutnick said “And as far as I know, they are acting swiftly, and if they execute it, there will be no tariff.” Fine, we’ll spend more on border toys so you don’t have to in addressing a largely made-up concern. The rest of what he had to say sounded like his best impression of Trump’s trade victim hogwash and warned tariffs could still be imposed later into Spring.

Lutnick and Bessent don’t call the shots, but it’s clear they are trying to delay and defer most of the tariff threat in a way that doesn’t totally embarrass their boss’s rhetoric. We’ll see if Trump does his usual thing by undermining and rejecting their efforts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.