ON DECK FOR WEDNESDAY, JANUARY 29

KEY POINTS:

- Markets await the Fed, BoC, US tech earnings

- Bank of Canada preview

- Uh oh, ‘Team Transitory’ is back in Canadian consensus thinking

- FOMC preview

- The RBA is more likely to cut next month after dovish CPI

- Riksbank cuts, stands by hold forecast

- Brazil’s central bank widely expected to hike 100bps

- Meta Platforms, Microsoft and Tesla to release earnings after the close

Happy Lunar New Year! Welcome to one of five times this year when the BoC and Federal Reserve will deliver decisions on the same date. They’ll each do what they must on the game day decision, and then try to out-dither each other on the noncommittal path forward not least of which given the uncertainty around the US administration’s next steps particularly on tariffs. Whatever impact they may or may not have could be short-lived with three of the ‘Magnificent 7’ US stocks reporting Q4 earnings in the aftermarket (Tesla $0.75, Meta Platforms $6.78, Microsoft $3.12). Overnight markets brought forward more evidence to support an RBA cut next month and the Riksbank’s 25bps cut. Brazil’s central bank is expected to hike 100bps later today.

BANK OF CANADA PREVIEW

The statement, MPR with updated forecasts including tariff scenarios and Governor Macklem’s opening remarks to his press conference all arrive at 9:45amET. The press conference starts 45 minutes later. Here’s what to expect.

Scotiabank Economics Expects a 25bps Cut

They will probably cut 25bps. Consensus is unanimous and markets are priced for it. That makes it the easy thing to do, though they have surprised in the past. Macklem’s December presser guided they would consider further easing, though not at the same back-to-back 50bps pace. That means 25 or zip, and a gradualist approach would prefer a step down rather than going cold turkey. I’ll come back to why I don’t think they should cut.

QT Announcement to be Reaffirmed, Implementation Likely At a Subsequent Meeting

A risk is that they announce the end of QT at this meeting but the bigger likelihood is that Macklem just reinforces what Deputy Governor Gravelle said recently. Why deliver a speech on doing so sometime in the first half of 2025 if you’re not open to discussing it now, versus delivering the speech in March on the usual timeline they’ve used in the past. I think this is low probability versus doing so at a later date, but not zero. Why low? Because they won’t be at their revised settlement balance targets until summer. Personally, I don’t think their QE experiment was worth it independent of the Fed’s and considering the enormous management time that was spent on implementing QE, scaling it back, implementing QT with 100% roll off and now getting out of QT. The rate equivalence was hard to prove and de minimis either way.

Tariff Scenarios and Discussion Will Be Key

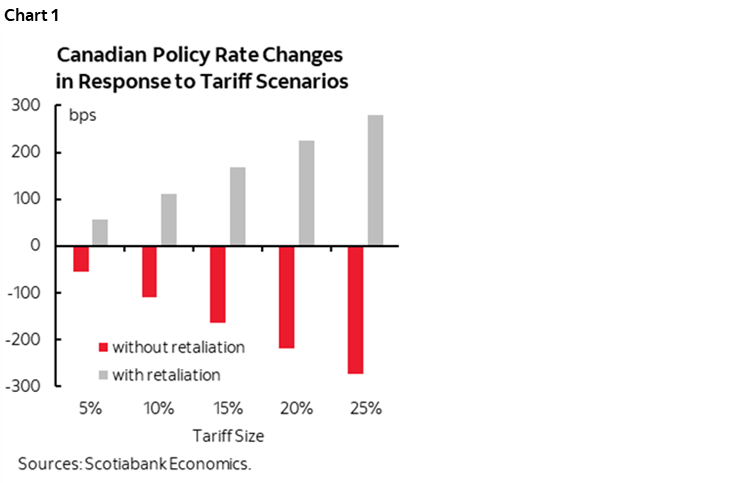

Watch the tariff scenarios. Macklem said they were being updated the last time he spoke at the December presser and they’ll be presented with this MPR. One of the scenarios in July 2019 was a universal 25% tariff which they are likely to include again, along with other more targeted ones. They may break out with- and without-retaliation, unless they’re convinced retaliation is likely. Their 2019 scenario assumed retaliation and the full outcome was a peak impact on inflation after 1 year but persistence up to 2 years depending upon whether expectations are unmoored.

A comment on that last point is worth it. Embedded within the rise of inflation is an unknown reaction function that they do not publish (ie: rate path). Saying they expect to achieve 2% inflation within two years is a) what the BoC always says because otherwise they’d be admitting failure in their mandate to achieve 2% within the medium-term, and b) probably includes a tightening path. That is what our modelling reveals as well (chart 1). At the minimum, you wouldn’t be fanning the flames of inflation even further by cutting, not in any material way at least.

And so the money question in the presser will be to ask Governor Macklem whether there is uncertainty about the direction of the policy rate in tariff wars with and without retaliation. Could it go up or down.

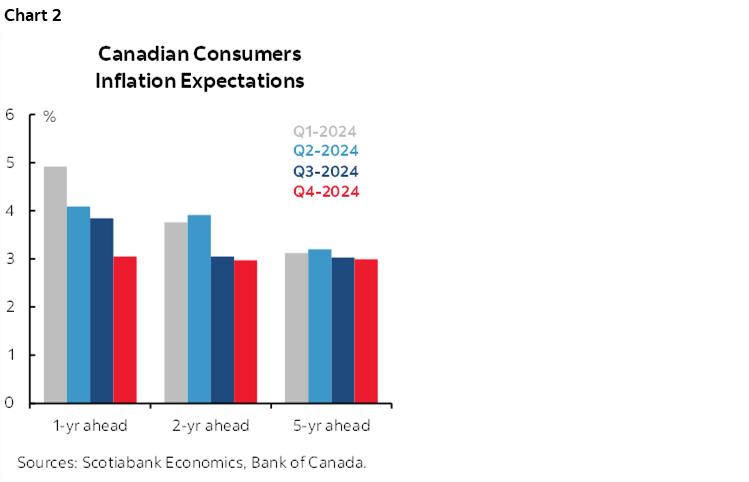

Further, note that the ‘transitory’ camp is back again. Uh oh—that was a disaster for the part of the forecasting community that bought into it during the pandemic whereas Scotiabank Economics did not. There is the direct effect of a tariff hike on prices that is transitory inflation. Then there are all the indirect effects from the damage to supply chains, to a further unmooring of inflation expectations that remain at or above the BoC’s upper limit of the 1–3% inflation target range (chart 2) and a shrinking supply side of the economy which add to inflation risk. This is a reborn version of the effects in the pandemic when ‘team transitory’ didn’t get this point.

Noncommittal Forward Guidance

On forward guidance, I’m not expecting much if anything. He should just shrug his shoulders given the bidirectional risk of the policy rate under tariff scenarios, plus the ex-tariff base case risks to further easing that I’ll return to next. For now, if you don’t know what will happen on tariffs and retaliation and you claim you don’t act until it is fact, then don’t pre-commit to doing anything now. At 3% they would be within the BoC’s 2.25–3.25% neutral rate range and no longer obviously restrictive. They don’t know what neutral is exactly—nobody does—and so as far as they’re concerned they’d likely be at it. Anyway, neutral is a very long-run guidepost for an economy in perfect equilibrium with no further shocks, and so nearer term policy rate decisions wouldn’t be made to hit some falsely precise level. Forecasting some further trivial move to hit an elusive long-run guessed-at target is not something worth sacrificing teamwork for! Canada 5s at 3% +/- are fair value given current information that could change very quickly and soon.

They’re Already in the Neutral Range, and Why They Shouldn’t be Easing

On why they shouldn’t cut there are several reasons. Their preferred core inflation gauges have been running at the 3–4% m/m SAAR range for months, signalling ongoing residual inflationary pressure. This is despite modest slack that may either be too small to matter enough, or dominated by other inflation drivers, or nonexistent if potential GDP is overestimated. Growth is modestly rebounding with Q4 tracking. Cooling labour force growth through immigration changes should tighten labour markets. Job growth is very strong in 1mo, 3mo, 6mo and 12mo horizons and it’s hogwash that it’s just public sector employment even if you accept putting such a filter on (as opposed to doing so just for overshooting civil servants). Consumption is performing reasonably well in three of the past four quarters as the rate sensitivity has lowered due to the rise of services. Growth ex-tariffs should pick-up with lagging effects of past monetary easing, lagging effects of immigration, accelerating real wage growth, exaggerated effects of mortgage resets, pent-up demand and massive pent-up savings.

See my Global Week Ahead from last Friday for more.

FEDERAL RESERVE PREVIEW

This one is just a statement at 2pmET followed by about an hour-long presser 30 minutes later. We’re in between SEPs including dot plots with the next one due in March. Markets are priced for nothing. Consensus unanimously expects a hold. FOMC officials have spoken that way. Make minor tweaks, repeat the December press conference, and move on.

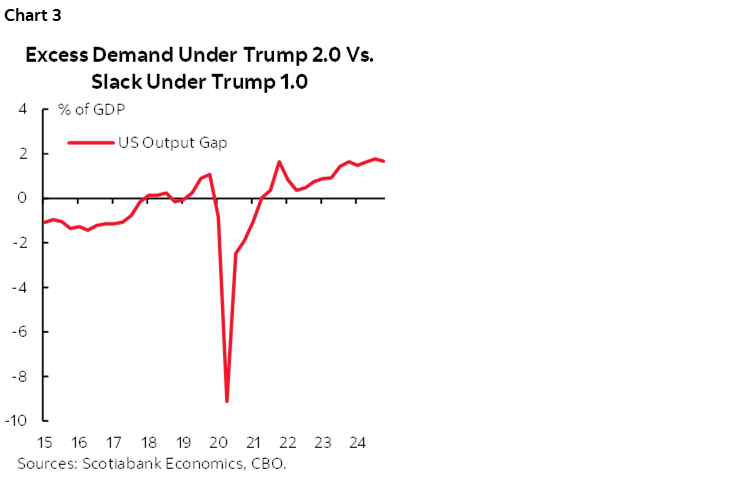

One reason is that the economy continues to perform well and this could carry dual mandate pressures. Q4 GDP the next day is likely to be around 3% q/q SAAR give or take (Scotia 2.8%); either way, it’s likely to be well above the economy’s noninflationary speed limit, or potential growth rate. That means the US economy continues to push further and further into excess aggregate demand (chart 3).

Given correlations with employment growth this suggests that part of the dual mandate may remain strong. Trump’s 8-month severance offer to federal employees who choose to resign instead of returning to the office could be a transitory hit to the 3 million Federal government employees in nonfarm payrolls (1.9% of total nonfarm payrolls) but I suspect it will be a modest hit. The bigger issue is that tighter immigration policy is likely to return population and labour force growth to nothing and perhaps negative, thus retightening the job market and putting renewed downward pressure on the UR.

On core inflation, we’ll get a second consecutive soft core PCE print on Friday probably around 0.2% m/m SA after the 0.1% prior reading. That’s encouraging, but not enough evidence yet and especially given the mess being created by abnormal SA factors post-pandemic. If the economy is in strong excess demand with a significantly positive output gap, then you would be careful toward a couple of months of data of disinflationary data in what could be merely another false soft patch. An economy at a starting point of excess demand that then adds fiscal and regulatory easing including through effects on banks while tightening immigration policy to crush the labour market’s supply side has to be viewed as facing greater upside risk to inflation.

On the rest of the macro assumptions, I would expect Powell to say the same things he said in December. Some FOMC members incorporated some assumptions on the incoming administration’s policies, some didn’t, and some were in between. He’ll say they won’t generally do so until they have more information. They might have it after this meeting and before the March one at least on topics like tariffs, retaliation, the magnitude of the immigration hit, whether the latest funding spat gets by the courts, and with a tax battle looming later.

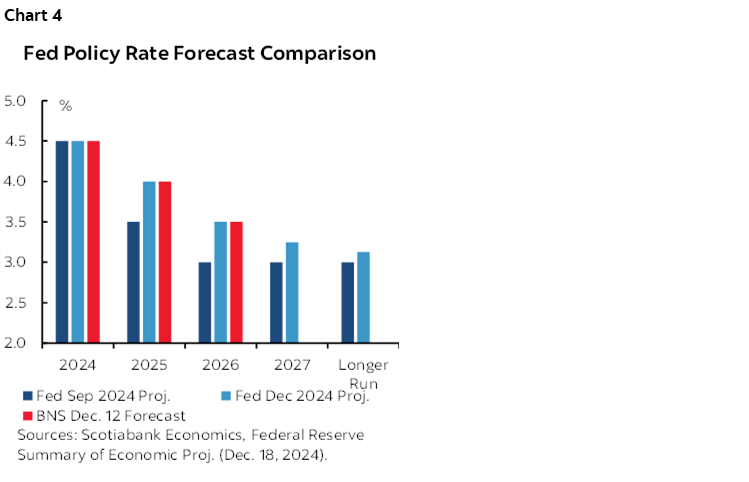

All said and done, say nothing new. Keep options open, but ever so slightly. I don’t think he’ll do anything to pre-commit to March especially since there is already a modest chance at a cut priced and with markets priced for -50bps this year which matches the December median FOMC projection (chart 4). He presumably wouldn’t want markets to make that a base case after today amid all of the uncertainty on the underlying excess demand pressures on the dual mandate combined with policy risk. Why rock the boat.

RBA LIKELIER TO CUT AFTER DOVISH INFLATION REPORT

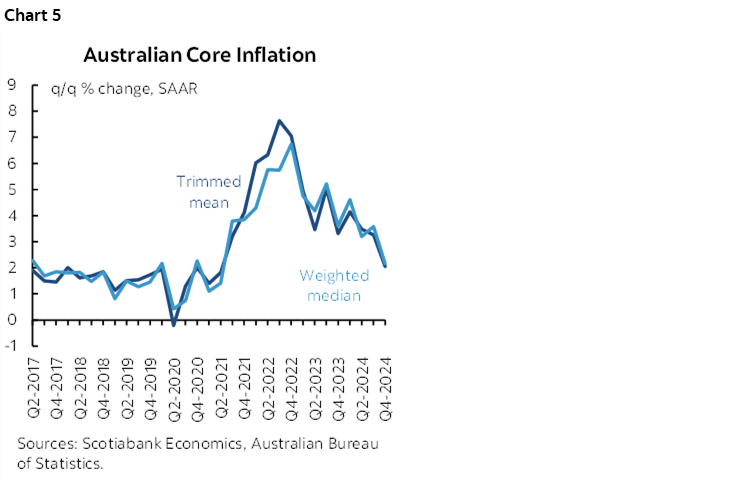

Australia CPI buoyed expectations for the RBA to cut 25bps on February 18th. A few more basis points were added to meeting pricing that is almost at a full quarter point, 2s rallied 7bps and A$ sank. Key is that the trimmed mean and weighted median CPI readings both landed on 0.5% q/q SA which is significant because the annualized rates are now at the bottom of the RBA’s 2–3% headline target range, and because they were the softest readings since 2021—before the great surge (chart 5).

RIKSBANK—CUT, STANDS BY HOLD FORECAST

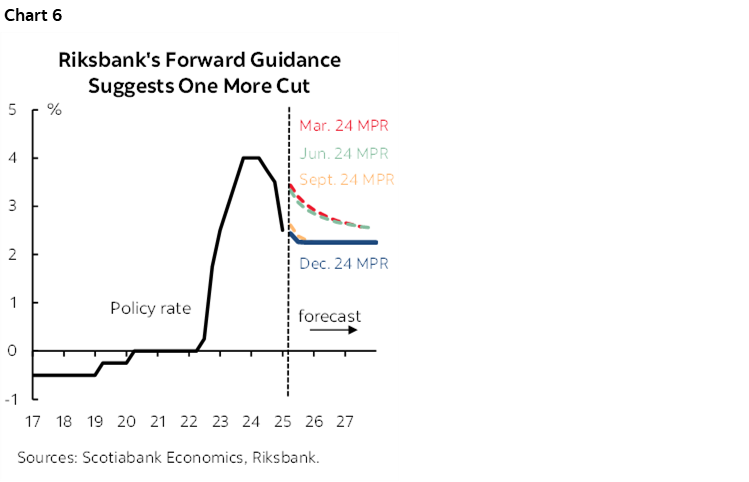

The policy rate cut of 25bps matched most economists’ expectations. The Executive Board said that the rate profile published in December “essentially holds” which means they are leaning toward holding unchanged for a while (chart 6). Their statement then said that “if the outlook remains unchanged, the policy rate may be cut once again during the first half of 2025.” There was little reaction in Swedish rates and the krona as markets continue to lean toward pricing another cut over H1.

BRAZIL’S CENTRAL BANK TO DELIVER ANOTHER MEGA-HIKE

Brazil’s central bank is widely expected to hike its Selic rate by 100bps today (4:30pmET). Recall that at the last meeting in December when they hiked by 100bps they said “the Committee anticipates further adjustments of the same magnitude in the next two meetings, if the scenario evolves as expected.” If BCB delivers three 100bps hikes in a row, then the result by the March meeting will be a Selic rate of 14.25% that would eclipse the peak post-pandemic rate peak and hit the highest since 2016. A chief concern is soaring inflation expectations.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.