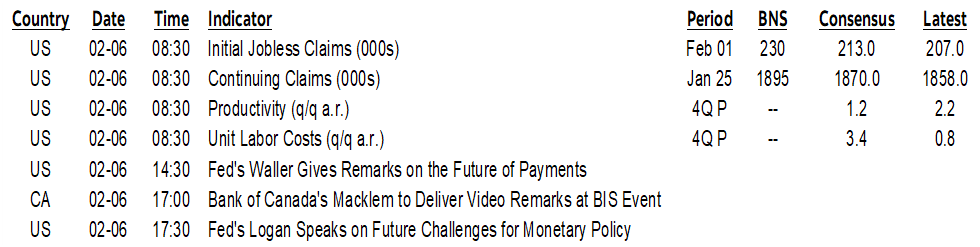

ON DECK FOR THURSDAY, FEBRUARY 6

KEY POINTS:

- Yen-sterling divergence driven by hawkish BoJ, dovish BoE

- US mass layoffs plunged compared to recent patterns to start the year

- BoC’s Macklem to weigh in on monetary policy…

- …and may provide freshened guidance with the uncertainty damage done

- Did markets take the Bank of England too dovishly?

- Banxico expected to cut

- Hawkish BoJ talk

- US productivity-adjusted wages likely accelerated

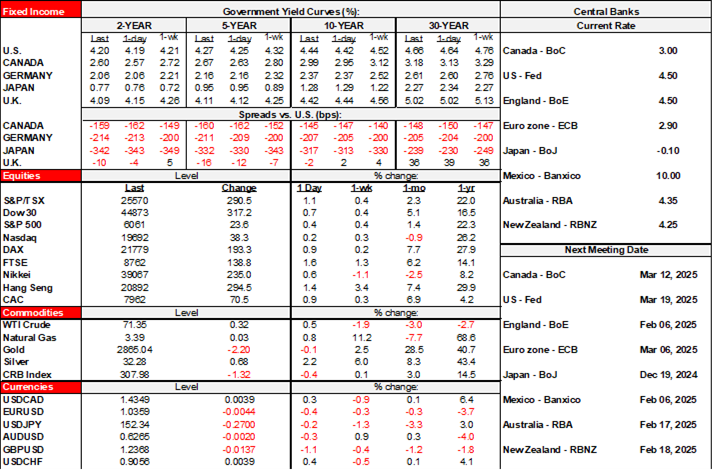

Four central banks are weighing in alongside limited data. The list includes a BoE cut and guidance that may have been taken a little too dovishly by markets, a pending Banxico cut, BoJ comments overnight, and pending BoC remarks that may be informative. So far, the market tone is constructive with equities up across most exchanges, sovereign yields a touch higher, and the dollar broadly stronger except against the yen after BoJ-speak.

US Layoffs Were Seasonally Low Ahead of Expected Gain in Labour Costs

More US labour market data is on tap before the only data that truly matters tomorrow.

Mass layoffs in January were much lower than is seasonally normal for recent like months of January which is the approach to take since the data is not seasonally adjusted. There were 49,795 layoffs in January versus 82k last January and 103k the January before that. The past couple of years have seen a surge in layoffs to start the year in a definite departure from prior years and this likely reflects distorted seasonal hiring and firings at the start of each new corporate fiscal year. That didn’t happen this year. And it wasn’t due to California fires or anything like that, since the biggest decline in layoffs last month compared to the prior two months of January was in the East.

Chart 1 shows layoffs, and chart 2 makes the seasonal point by illustrating how low this year is starting off compared to the prior two.

Q4 productivity and unit labour costs will be released at 8:30amET and they are expected to signal an acceleration of productivity-adjusted labour costs. Initial claims (8:30amET) are also due after the prior week fell largely due to California’s fires that temporarily interrupted filings.

Hawk Talk from the BoJ

Hawkish talk from the BoJ lit up the yen again at least on a relative basis to other crosses while it holds it own against the dollar. BoJ Board member Tamura said overnight that he thinks the policy rate of 0.5% now should rise to 1% over the second half of fiscal 2025 ending March 31st next year. That added a little to BoJ pricing that was leaning in that direction with a next hike fully priced by September. Tamura is viewed as among the most hawkish Board members, if not the most hawkish.

Former BoJ Governor Kuroda also sounds enthused. He said “Japan’s economy is completely back. It’s perfectly natural for the BoJ to conduct policy normalization. There is no mistake that a virtuous cycle between wages and inflation has been recovered. The BoJ will proceed with normalization by carefully watching those trends.”

There is still a need for caution in my view as the BoJ marches through elevated global trade and investment uncertainty.

Bank of England Cuts, Dovish Stance Drives Weaker Sterling, Lower Yields

The Bank of England wasn’t as dovish sounding as markets seemed to think in my opinion. They cut Bank Rate by 25bps as widely expected, but the rest of the statement and forecasts amplified market pricing for further easing.

For one thing, the vote was 7 in favour of a 25bps cut and two (Dhingra, Mann) who preferred 50 and so yes, the fact that a minority were driving a debate for a bigger cut is somewhat dovish at the margin. The statement (here) continued to signal serial downside surprises to GDP growth in the near-term. Yet forecasts for inflation were revised up across 2025, 2026, and 2027 and CPI inflation remains above 2% for longer than expected in the last round of forecasts in November. Forecasts for growth were revised a little lower in 2025 but higher in 2026 and 2027. The supply side is expected to grow more slowly than previously expected and guidance indicates that while tariffs are not incorporated into the forecasts, the uncertainty is expected to hamper investment.

Guidance noted that “Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restrain is appropriate.” They also indicated ‘a gradual approach’ in the prior statement.

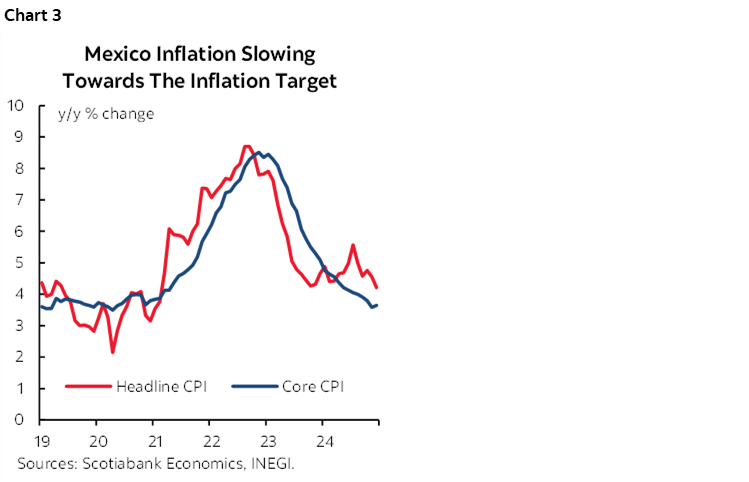

Banxico Expected to Cut Again

Banxico is (almost) unanimously expected to cut its overnight rate by 50bps on Thursday, taking it down to 9.5%. Inflation continues to make progress (chart 3). There is obviously significant ongoing risk surrounding tariff developments. MXN has depreciated from about 16.7 to the dollar last Spring to about 20.6 now.

BoC Governor May Give Freshened Guidance

A BoC speech drop occurs after the market close today. BoC Governor Macklem will issue a speech titled “Future Challenges for Monetary Policy in the Americas” at 5pmET. He was to have attended the BIS conference in Mexico in person but cancelled that earlier this week and will now just issue his prepared speech on the BoC’s website. There will be no media lock up or Q&A. Watch closely what he says about the heightened trade uncertainty. My hunch is that he may lean toward saying the damage has been done regardless of whether tariffs actually do arrive or not, but with mixed effects on the supply side (via reduced investment) and demand (exports).

Light Overnight Data

As for data, the only notable release overnight was strong German factory orders. December was up 6.9% m/m which more than tripled consensus expectations, though recall that orders fell by over 5% the prior month. Maybe it’s tariff front-running, or just the latest extension of see-sawing German data.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.