ON DECK FOR MONDAY, FEBRUARY 3

KEY POINTS:

- Equities, CAD, MXN, CNH plunge as US starts a trade war

- What happened over the weekend and next steps

- Trump just doesn’t get the trade and dollar connections

- Fentanyl? Oh please. Tariffs have nothing to do with that

- Canadian tariffs were not ‘dollar for dollar’…

- ...likely giving the BoC room to ease near-term…

- ...amid a highly uncertain inflation outlook that risks whipsawing them again

- US ISM-mfrg to be stale on arrival

- Fed-speak, ECB-speak on tap

- See the Global Week Ahead — Tithes to the King, here

Trump—allegedly elected as a better steward of the economy—thought his first major act should be to pick a trade war with allies. Duh-duyyyy! Putin’s loving the fact that all of his western foes are now fighting each other. Markets aren’t so impressed. Stocks are broadly lower by either side of -1½% declines in NA futures and European cash markets. Asian equities have more catching up to do after the Lunar New Year holiday and so they fell by more; Tokyo and Seoul dropped 2½%, Taipei was down 3½%, mainland China is still off. Markets are functioning through price discovery.

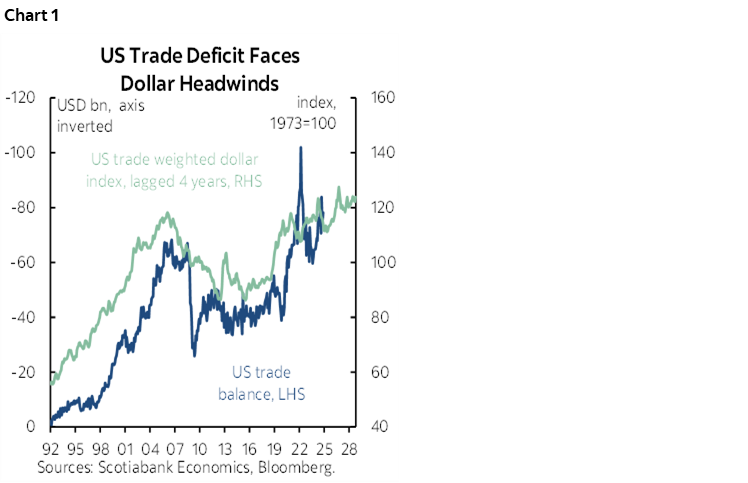

The dollar is stronger across the board. Trump just doesn’t get it. US tariffs on net reduce demand for foreign currencies through the harm to imports and raise safe haven appeal for the dollar which is benefitting the yen as well. What happens when you raise appetite on net for dollars? The lagging effects drive a bigger trade deficit which worsens Trump’s concerns, so he’ll do more to strengthen the dollar, and on we keep going with the usual lagging effects (chart 1). Duh-duyyy! All major crosses are weaker to the dollar with MXN’s 2% drop leading the way.

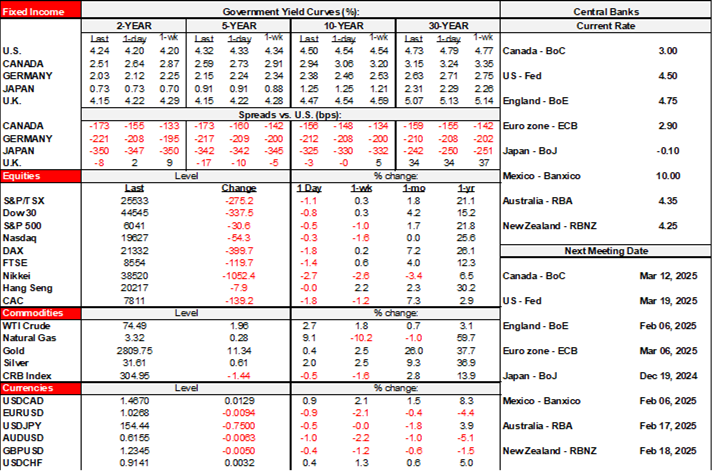

US Treasuries are underperforming everywhere else with 2s mildly cheaper in a bear flattener move. Canadian government bonds are outperforming all comers with the whole curve down by double digits in yield terms. EGBs and gilts are also rallying as were Antipodean rates overnight.

As a reminder, I put out this piece titled The Saturday Night Tariff Thrashing yesterday morning after providing coverage to clients and staff via chat rooms etc throughout Saturday evening. It summarizes what the US did, how Canada, Mexico, China and Canadian provinces are responding, and next steps.

There isn’t much to update since I put that out. Since the note was put out we got the list of what Canada is targeting with 25% tariffs on $30B of imports from the US this Tuesday and guidance that the target list for the other $125B of targeted imports would be provided “in the coming days” with a 21-day public comment period. The first tranche of retaliatory tariffs is similar in nature to the goals of the 2018–19 tariffs that aim for red states (Harleys, OJ, booze et). The guidance for the second list is that “It will include products such as passenger vehicles, trucks and buses, steel and aluminum products, certain fruits and vegetables, aerospace products, beef, pork, dairy products, and more.” That’s the list that possibly includes Teslas.

This may be relevant to your clients in terms of seeking relief from Canada’s tariffs or refunds. Share and advise as suitable across clients and Scotiabankers especially their commercial and investment banking and equity clients.

Trump is to hold calls with PM Trudeau (it isn’t known who asked for the call) and President Sheinbaum this morning. Monitor remarks afterward including ones that inform potential appetite for further retaliatory measures. Plus watch for company remarks especially in autos that are on the front line of all of this.

There have been some additional provincial developments since the summary note was released that are relatively minor, like more provinces pulling US alcohol from stores. You’re also hearing more warnings from some of the most heavily affected industries, like autos and steel, so watch the developments closely amid dire warnings of near-term plant shutdowns and cancelled contracts.

And as a reminder, it’s a full-on lie that Trump’s tariffs against Canada have anything whatsoever to do with fentanyl despite the way the executive order was crafted. The only reason for that reference in defiance of the facts is so that Trump can fabricate a national security crisis so that he can bypass Congress and exploit the past pieces of legislation that were not intended to be used for such purposes. Full stop, don’t buy into the misleading US propaganda that I see some gullible media personalities falling for.

My Global Week Ahead article went over the real underlying reasons for Trump’s tariffs.

Light Data Shouldn’t Matter

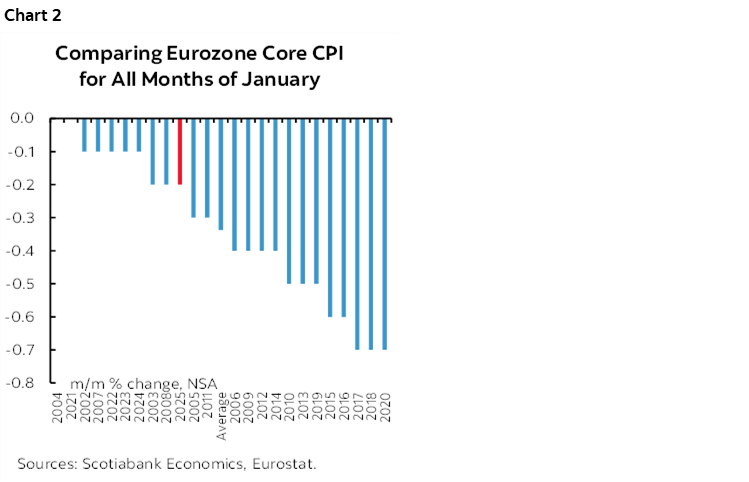

Data doesn’t matter except for the diehards. The main release was that Eurozone CPI was a touch firmer than consensus expected (-0.3% m/m NSA, -0.4% consensus) and in y/y terms as well (2.5%, 2.4% prior and consensus). Chart 2. Part of the reason is that Italy’s CPI fell -0.7% m/m NSA (-1.1% consensus). Markets didn’t care because trade wars reset the risks as Trump escalated his tariff threats to Europe.

We’ll get some US data this morning at 10amET. It won’t matter either. ISM-manufacturing for January might inform supply chain preparedness effects for the lunacy, but it’s a lagging reading in the face of Trump’s weekend sucker punch.

Limited Fed-speak is on tap (Bostic 12:30pmET, Musalem 6:30pmET) and we may hear initial takes on the effects of trade wars now that the Fed can no longer say they won’t incorporate anything until its fact. Well, it’s fact now.

BoC Implications

As previously noted, not matching with dollar-for-dollar tariffs lessens inflation risk of Canadian tariffs and CAD depreciation and makes a cut—perhaps an upsized one—more likely. They said dollar for dollar but that's not what they've done. Not even close.

But as long as markets are functioning, which they likely will, then wait. I don’t see emergency pressure at this point to contemplate an intermeeting move. CAD and market rates can do their work at first. It's a risk but I think there is a very high bar for going inter-meeting.

One reason is that the BoC will want to see next steps and evaluate the longevity of the shock. Who knows exactly where this is going. The players are far too erratic.

Another reason is that tariffs will have slower lagging effects than at other times when the crisis was instant in financial markets or with complete shutdowns. Monitor this in terms of industry guidance on specific sectors.

Another reason is to evaluate early evidence on the supply shock.

What also matters is the fiscal response that is pending. I can see coordinated announcements by the Feds and provinces and BoC again, like early in the pandemic. That’s possible soon, but it can't pass it until >March 24th unless prorogation is temporarily suspended. So wait to coordinate.

The key question is how the rest of the curve responds. Yields move lower in the short term, but if we're heaping on fiscal stimulus amid supply chain shocks that may include plant closures and CAD is unmoored then inflation risk further out repeats the pandemic and then the BoC is whipsawed again.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.