ON DECK FOR THURSDAY, FEBRUARY 13

KEY POINTS:

- Global bonds consolidate yesterday’s post-CPI sell off

- Tariff man is putting on his suit again…

- …saying ‘this is the big one’ on reciprocal tariffs

- Canada may be facing an April election instead of May

- US PPI to be a slight downward emphasis upon the Fed’s preferred core PCE gauge...

- …but the Fed has an eye on the bigger picture on a long hold

- BoC’s Summary of Deliberations reemphasize policy ambiguity in trade wars

- OSFI basically abandoned higher capital requirements because the US did

- Trump’s perilous call with Putin

- Gilts slightly underperform on UK data beats

- Philippines central bank surprises, pointing to global uncertainty

There is a lot on the go this morning, from an expected tariff announcement to firmer talk of an early election call in Canada, plus a central bank surprise and data. Data is focused on US PPI that adds slight downside to next week’s PCE report that will likely land at 0.2% m/m SA, but who cares with the Fed’s focus upon greater uncertainties. UK macro beats are weighing on gilts. Europe is seriously ticked about the Trump-Putin call that in my view faces a very long and uncertain road toward some form of peace regardless of Trump’s hubris.

The market tone is consolidating yesterday's post-CPI sell off in sovereign bonds and putting up modest rallies across most major markets. The dollar is also broadly softer. NA equity futures are very slightly higher with most of Europe outperforming except for London.

AN EARLIER ELECTION IN CANADA?

Canada’s NDP is reportedly warning its candidates and campaign staff about a snap election call as early as March 10th, the day after the Liberals choose a new leader. They are of the belief that Mark Carney—the leading candidate—would call an election immediately and hence not wait for parliament to return from being prorogued on March 24th. That initial time line had set up a confidence vote by no later than March 31st and then hold an election sometime in May after the required campaign period. If this is true, then Canada may face an election in April.

US PRODUCER PRICES OFFSET SOME OF CPI’S IMPLICATIONS FOR PCE INFLATION

US producer prices were up by 0.4% m/m in January (0.3% consensus) and core prices excluding food and energy were up 0.3%, matching consensus. There were strong upward revisions that lifted PPI by 0.5% m/m instead of 0.2% in December, and core PPI by 0.4% m/m in December instead of 0.

Key is how PPI translates into the Fed’s preferred PCE inflation readings given that some components of PPI are used in PCE. Chart 1 shows how PPI components translate into about a –0.06% weighted drag on headline PCE and slightly more for core PCE, which generously rounds up to a –0.1% weighted drag.

Take that along with CPI implications for PCE that were explained in yesterday’s CPI note (here). The core CPI reading of 0.4% m/m SA would be knocked down by –0.18ppts due to the different weights issue and by another –0.07 or so by the PPI implications for a net expectation that core PCE will land on about 0.2% m/m SA.

And because of the upward revisions to PPI, core PCE may be very slightly revised higher but that effect largely gets lost in the rounding.

And who cares. The Fed is obviously on a lengthy pause and so it will need multiple rounds of data while it evaluates policy and other developments before having confidence in making future moves.

MILD UK DATA BEATS

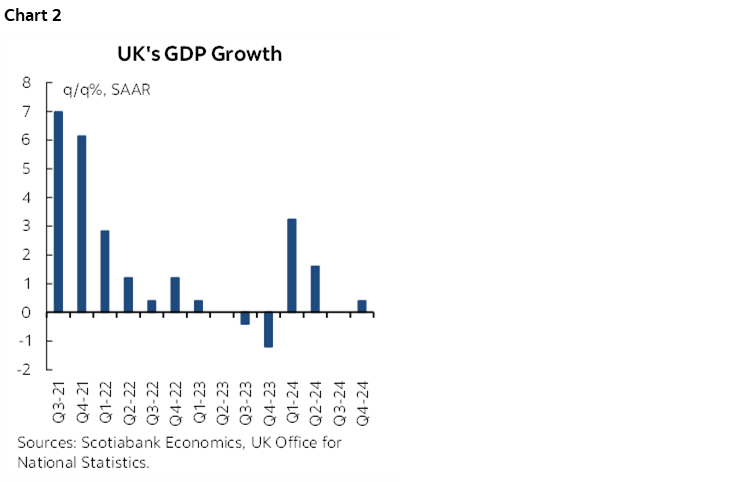

UK macro data posted a set of mild beats that partially explains mild underperformance by gilts. Q4 GDP was weak, but at 0.1% q/q SA nonannualized was slightly better than consensus (-0.1%) and the absence of revisions to the prior quarter’s 0% reading allowed the UK to ever so slightly escape a technical recession call (chart 2). GDP for December was up 0.4% m/m, four times consensus. Industrial output climbed 0.5% m/m (0.2% consensus) which basically cancels the prior decline of the same magnitude. Services also grew 0.4% m/m in December (0.1% consensus). The trade balance also turned out better than expected with positive revisions as exports grew 0.7% m/m, but the 1.5% m/m drop in imports after being flat in December signals soft domestic demand.

PHILIPPINES’ CENTRAL BANK SURPRISES, BASICALLY POINTS FINGER AT TRUMP

Bangko Sentral ng Pilipinas surprised by holding its policy rate unchanged at 5.75%. Only one out of 29 within consensus got the call right as everyone else expected a 25bps cut. Uncertainty toward global policies and their effects—looking at you, Trump—was flagged as the reason for the hold, but forward guidance continues to lean toward future easing and a planned 200bps cut to the required reserve ratio over 2025H1. That would take the ratio down to 5% in a continued progression lower from 12% in 2023 and the 20% level a decade ago.

TARIFF MAN TO ANNOUNCE RECIPROCAL TARIFFS TODAY

Ever the showman, Trump posted this on his social media account this morning:

“Three great weeks, perhaps the best ever, but today is the big one: reciprocal tariffs!!! Make America great again!”

In all caps no less. The announcement is expected at 1pmET. We need to see details on rates, which countries and sectors, and timing. We may or may not get all of that today. Trump’s pattern is to make a splash, and then hold off. The more he does that, the more nobody should listen to him.

The issue is imposing tariffs on countries that have tariffs on the US. Perhaps other countries will do the same to the US in sensitive areas like how the US 25% “chicken tax” on imported trucks benefits domestic US producers. If so, then there goes US truck demand abroad.

I for one would seriously dispute ‘three great weeks’ because in my opinion they’ve been a chaotic, rolling train wreck starring Trump with dampening effects on confidence to invest. Nevertheless, watch for a more formal announcement on the tariffs today that likely uses Section 232 again.

What should Canada do in response to Trump’s tariffs? Increasingly it’s looking like US industry is speaking up against them. See recent comments by the CEOs of companies like Ford and Generac about how tariffs would heavily disrupt their supply chains and cause higher prices. So Retaliate. Then Just. Sit. Back. Retaliate, while making it clear that Canada is in it for the long haul if necessary and so as to avoid being bullied into a bad agreement that it could be stuck with for years, and then let US industry talk some sense into this chaotic US administration. I don’t accept any arguments in favour of Trump’s tariffs other than that they are entirely about him.

BOC’S SUMMARY OF DELIBERATIONS REEMPHASIZED POLICY RATE UNCERTAINTY

The Bank of Canada’s Summary of Deliberations in the lead up to the decision on January 29th was released yesterday (here) and reemphasized the ambiguity around how the policy rate would be managed in tariff scenarios.

There were two key passages in that regard. Here’s one:

"Members discussed whether to provide any guidance on the future path for the policy interest rate in its communications. They agreed that given the high level of uncertainty surrounding the outlook, and the wide range and complexity of potential trade conflict scenarios, that it would not be appropriate to do so at this decision. Members agreed that it would be important to provide Canadians with their updated analysis and assessments of the impact of a trade conflict on the economy and inflation as it unfolds."

And here’s another:

"Members were concerned that US tariffs on Canadian exports would add significant pressures on Canadian exporters. Over time, this could lead to business closures and companies exiting the export sector. In the long run, tariffs introduce inefficiencies that weigh on the productive capacity of an economy—meaning lower productivity and lower potential output than in the absence of the tariffs. Members recognized that monetary policy is not able to offset these longer-term implications of a trade conflict. It would only be able to smooth the path in the short-term as the economy transitions to a lower productivity and lower output trajectory."

The takeaway? I continue to think that consensus is ignoring the supply side arguments all over again and choosing to look past lessons it should have learned in the pandemic. You need to watch supply side implications stemming from trade wars as closely as the demand side implications.

OSFI ABANDONS BASEL III PLANS

This announcement by OSFI—Canada’s bank regulator—deferred plans to increase to the Basel III standardized capital floor level ‘until further notice.’ Ergo, indefinitely. They had previously delayed plans by a year last summer, but have now largely shelved them. This follows the global pattern of delayed or cancelled plans including in the US. OSFI did say there would be ‘at least two years’ notice before revisiting. What this means is that Canadian banks won’t be at a relative disadvantage to banks elsewhere—notably the US—in having to set aside more capital. The competitive equity angle clearly dominated their decision since the release notes that “At present, however, there remains uncertainty about when other jurisdictions will fully implement Basel III.” Under Trump? Likely never.

TRUMP IS OVERPROMISING A RUSSIA-UKRAINE PEACE DEAL

I wholeheartedly agree with John Bolton’s take on Trump’s phone call with Putin yesterday when he said:

“President Trump has effectively surrendered to Putin before the negotiations have even begun.” He went on to flag the “terms of a settlement that could have been written in the Kremlin.”

So Trump wants to cozy up with Putin, throw Ukraine under the bus, embolden Russia's future aggression while picking fights with his allies. All very much as expected and hardly cause for fist pumping despite some of the naïve views I’ve seen and heard. Markets are taking is as an off-ramp from geopolitical risk with WTI oil prices down almost US$/barrel since headlines began hitting yesterday.

Ukrainians will hate Russians for decades for what they've done and the territory that has been lost to date. There will remain a Ukrainian resistance no matter what agreement is struck. There will remain Russian agitation on the ground in one form or another regardless of any deal that may eventually be struck. Peace with Russia is never to be trusted; Russia-backed separatists continued their attacks after the 2014 war and the West’s indifference allowed Russia to come back again about a decade later. Just when Putin’s war was straining Russia to the max, Trump throws a lifeline that raises future risks around Russian aggression applied against other states. Ukrainians will never trust the West that threw them under the bus in 1994 by promising security in exchange for giving up nuclear weapons. It has no reason to trust the West now.

Now Trump promises to end the war. By leaving the Europeans and Ukraine out of talks and yet curiously assuming European forces—not American troops—will commit to the enormous long-term cost of a peacekeeping force while their forces are not backed by NATO Article 5 guarantees.

The US always thinks it can end wars with military might and the flick of a switch but leaves intractable messes behind in its wake (Afghanistan, Iraq, Vietnam etc). And then what, Russia comes back again in future years? Relieve Russia of sanctions while imposing tariffs on allies?

That’s always been my fear about this US administration in that it would cozy up to brutal regimes and distance itself from allies. That is a far cry from the America that I grew up watching but it is becoming reality in today’s Trumperica.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.