| ON DECK FOR WEDNESDAY, FEBRUARY 12 |

KEY POINTS:

- Markets await a US CPI report that frankly doesn’t matter

- Trump’s trade policy is getting more unglued by the minute

- US CPI expectations

- Powell round two

- BoC to deliver the not-minutes Summary of Deliberations

Ready, set, snooze! The only calendar-based risk to consider will be the US CPI number and it matters not one iota to the Fed. Off-calendar risk could easily matter much more these days.

For that matter, Trump’s unglued trade policy that’s threatening 50–100% tariffs on Canadian autos and combining 25% steel and aluminum tariffs with 25% across the board tariffs for a cumulative 50% rate on the metals from Canada and Mexico matters way more. Trump and his combative Commerce Secretary Lutnick (here) should listen to the various industry voices in the US including Ford’s CEO (here). This is policy made up on the fly by a chaotically mismanaged White House more interested in the trade than the impact of its actions upon millions of lives.

I’m also more concerned about where the heck to put well over another 40–50cms of snow on the way through the weekend than I am about CPI. That’s 15–20” for the few in the world still on the Imperial system, an exclusive list including only the US, Liberia and Myanmar! Tariff them for the added compliance costs of having to convert!

Why US CPI Just Doesn’t Matter

Why doesn’t this CPI report matter? One reason is because the FOMC is very clearly on hold for the March 19th FOMC and so nothing immediately hangs on this report.

Another reason is that there will be three CPI and three PCE reports before the next meeting on May 7th. One report will decide absolutely nothing, and if we do get tariffs, then the FOMC won’t be spending a whole lot of time looking back on inflation that was. For one month. Plus, there will be a whack of job market readings and dozens of erratic policy signals from the US administration. Among those signals – other than tariffs – are whether Congress can deliver on Trump’s fiscal wish list in the first 100 days as per his demand, and which lands just before the May FOMC. That’s the bigger picture in my opinion, whereas this CPI report just doesn’t cut it.

And of course, the FOMC focuses upon the PCE inflation reading for which we need CPI and tomorrow’s PPI to firm up expectations for the next update.

CPI Expectations

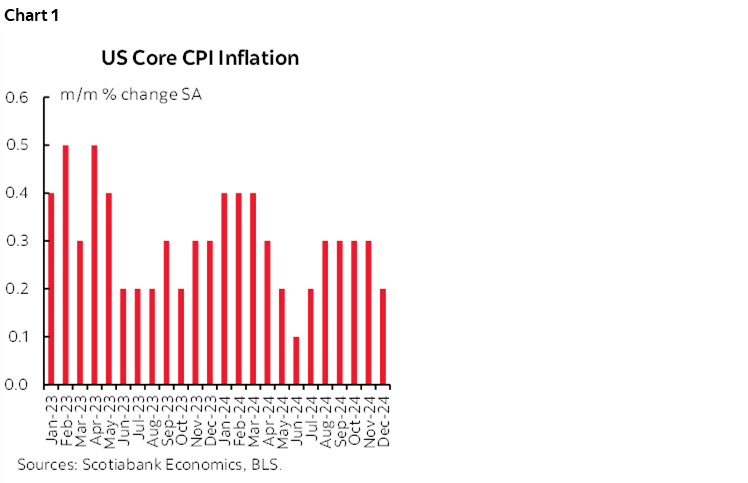

Chart 1 shows the recent pattern for m/m core CPI. The last print for December was 2.7% m/m SAAR and the 3-month moving average for core CPI is running at a hot 3.3% m/m SAAR.

Consensus expects 0.3% m/m SA for both headline and core CPI in January. The Cleveland Fed’s nowcasts are 0.2% for headline and 0.3% for core. I also went with 0.2% m/m SA for headline and 0.3% for core in Scotia’s estimates that were submitted last week.

Gas prices were up a touch but by a little less than is seasonally normal and so there is a small m/m drag from SA gasoline prices on headline CPI.

Vehicle prices were materially lower last month in both seasonally unadjusted and adjusted terms according to industry guidance. How that translates into the CPI methodology is uncertain, but it could hold back core.

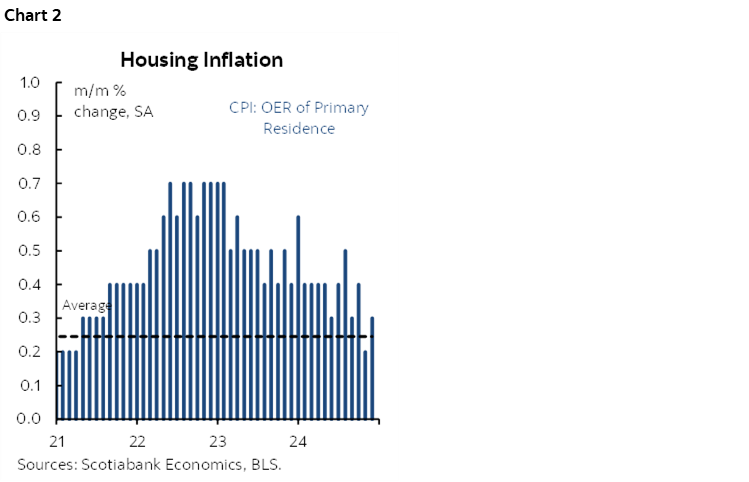

I’ve gone with sticky shelter prices up 0.3% m/m that are off the peak influences but still showing some persistence (chart 2).

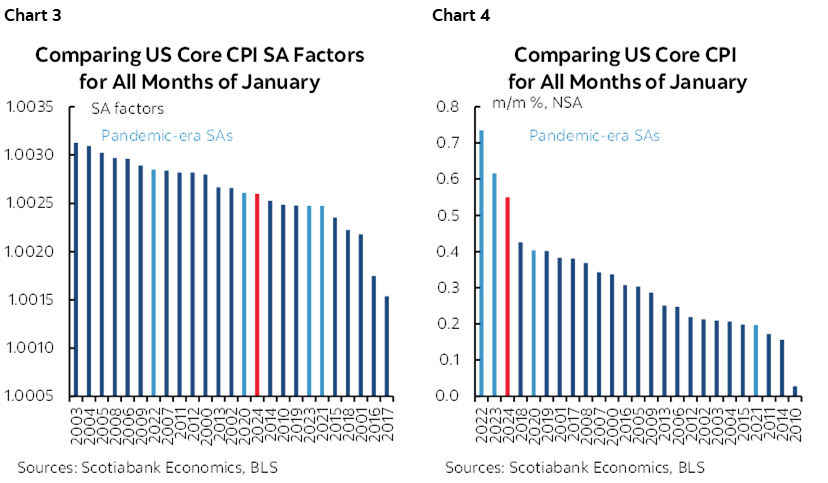

January’s seasonal adjustment factors tend to be on the lighter side in recent years (chart 3) but NSA price gains to start each year tend to be stronger than usual in recent years (chart 4). Starting since before the pandemic back in 2018, company pricing models pivoted toward jumping out of the gates with larger price increases to kick off the new year. The seven biggest January m/m NSA price gains have all been the seven years since 2018.

That said, this is the report that introduces annual revisions to estimated seasonal adjustment factors stretching back over the past five years and so there is lower confidence in the SA factors that will be applied to the NSA changes.

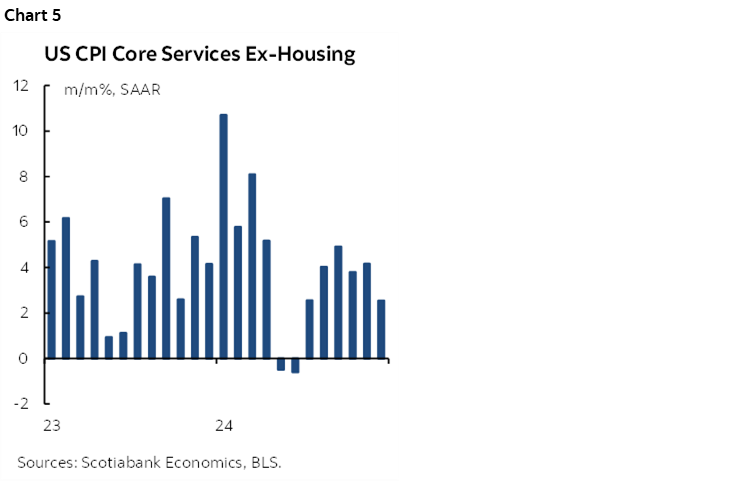

Core service prices (ex-energy and housing) have also become tamer over time, but still exhibiting considerable stickiness (chart 5).

There is more on US CPI etc in my Global Week Ahead here.

Powell Round Two

Federal Reserve Chair Powell delivers round two of his semi-annual testimony this time before the House Financial Services Committee (10amET). He may react to CPI, but flag that a lot more data is needed to inform the length of the pause.

BoC’s Summary of Deliberations

I’m not expecting much out of the BoC’s Summary of Deliberations (1:30pmET) in the wake of various communications from the Bank of Canada.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.