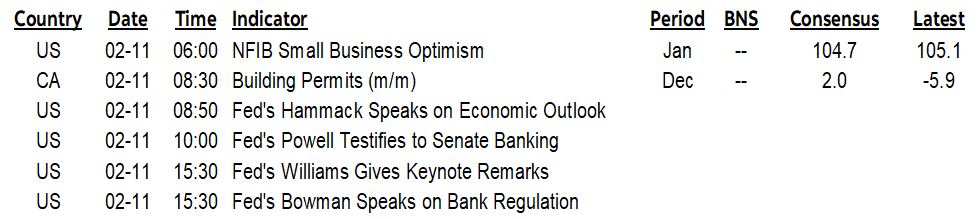

ON DECK FOR TUESDAY, FEBRUARY 11

KEY POINTS:

- Bond yields rise into Powell, post-tariffs

- Trump’s tariffs will spur full pass through into higher inflation…

- ...as even the US aluminum lobby says so...

- …and announcing them into Powell’s appearance wasn’t terribly bright!

- Canada, EU threaten retaliation

- Powell’s testimony will double down on patient messaging

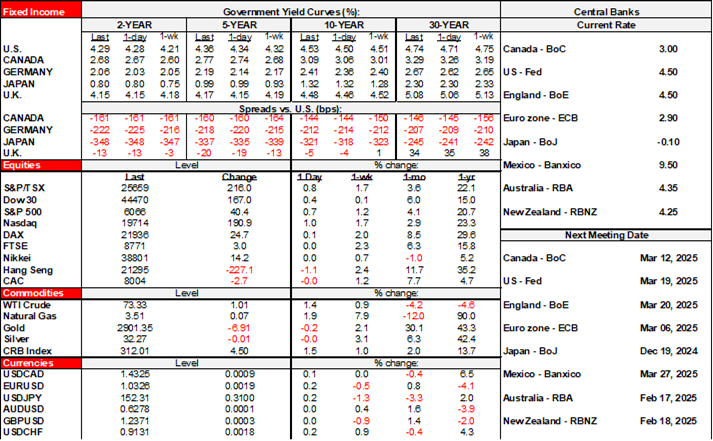

Sovereign bond yields are moderately higher across major markets in the wake of Trump's tariff announcement last night and ahead of today's Powell testimony. Equities are flat to slightly lower across major markets.

Metals Tariffs to Spur US Inflation

Trump did indeed announce a 25% tariff on all imports of steel and aluminum in all forms effective March 4th. The executive order for steel is available now (here) but the one for aluminum is still pending. Trump is again abusing national security provisions claiming that imports are a threat to national security only so that he can bypass Congress. The move tears up past agreements, proving yet again that Uncle Sam’s signature isn’t worth much. Canada and the EU have both said they intend to respond in 'firm' fashion. The Canadian retaliation has already begun through various tactics including my family joining this trend by avoiding personal travel to the US this March break.

But there are significant question marks.

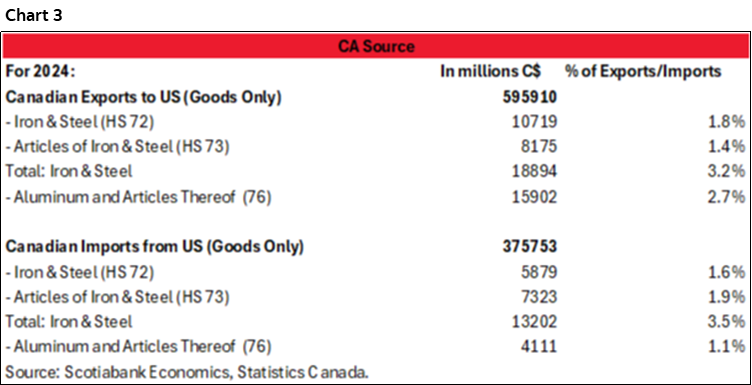

First, note that the March 4th effective date for the steel and aluminum tariffs from all countries—which heavily targets Canada given where the US sources its imports of the metals as illustrated in yesterday’s morning note—roughly coincides with the 30-day delay of the 25% tariff on all Canadian and Mexican exports to the US. When the US imposed steel and aluminum tariffs in 2018 they took effect immediately.

So, a key question is why the matching delay? Is this a hint at an off ramp on the universal tariff? Alternatively, are the steel and aluminum tariffs cumulative to the 25% on all Canadian exports or just cumulative to pre-existing levies on other countries? Trump had alluded to this issue in vague language last week.

Second, does the US have the ability to replace foreign imports? Trump made this factually false claim: “We don’t need it from another country. As an example, Canada. If we make it in the United States, we don’t need it to be made in Canada. We’ll have the jobs. That’s why Canada should be our 51st state.”

Dream on. But key here is that his own country’s industry is calling his bluff and backed by chart 1 that shows capacity use in the US mining sector is sky high.

Once one gets past the first two paragraphs in this release from the Aluminum Association in the US that basically suck up to Trump, the last paragraph is the key. They point directly to how much comes from Canada and how US-based aluminum smelters have no spare capacity and it would take "billions of investment over decades to make the US fully self-sufficient for its metal needs."

That means prices will go up on full pass-through effects. That benefits Trump's buddies in the sectors whose shareholders get a pay raise but at everyone else's expense.

And so I'll say it again, there is nothing more patriotic for American c-suites to do than to jack up prices on their fellow Americans. American businesses and consumers that use steel and aluminum should be taking out their anger on the domestic steel and aluminum producers who benefit from Trump’s tariffs at least in the short-term. It’s a lousy national industrial policy to stiff your own consumers that harkens back to the dark days of mercantilism.

Federal Reserve Chair Powell's Testimony to Double Down on Patience

The other main development will be round 1 of Federal Reserve Chair Powell’s semi-annual Congressional testimony (10amET). The first round is before the Senate Banking Committee and he’ll read a statement at the start and then go to tedious political rants by Senators and Q&A.

How misguided to announce inflationary tariffs on the eve of Powell's testimony but the US administration's communications are in disarray.

Expect Powell to double down on his guidance that ‘we don’t need to be in a hurry to adjust our policy stance.’ The new information for Powell since the last time he spoke will include the metals tariffs, probable retaliation, and a solid nonfarm payrolls report that beat expectations on net after including upward revisions. The 3-month moving average for payrolls is holding very firm at 237k and I think he’ll say the January gain of 143k was stronger than it appeared. Q4 GDP was also released after his last press conference and while headline was weaker than expected, details like consumption and final domestic demand were robust. Expect lots of questions on tariffs and probably the same answers.

More Fed-speak arrives with NY’s Williams (3:30pmET) and Governor Bowman (3:30pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.