ON DECK FOR FRIDAY, DECEMBER 5

KEY POINTS:

- Constructive market tone awaits three main developments to end the week

- Carney, Sheinbaum and Trump to meet today…

- …as trade headline risk could count more than data…

- …with Trump’s threat to pull CUSMA deal lacking much credibility

- Canadian jobs trend will remain strong

- US PCE: too stale to matter for next week’s FOMC

- Ditto for consumption, incomes

- US UofM sentiment: consumers as unemployment forecasters

Markets are in a fairly constructive mood at the end of the week. Hopefully that holds up through Canadian and US data releases that are on tap this morning along with potential NAFTA/CUSMA/USMCA sparks. Overnight developments were very light, such as a strong beat by German factory orders that have jumped higher in the past two months after sliding for four. Stocks are broadly higher across major benchmarks. The dollar is gaining against most crosses except the yen. Sovereign bonds are little changed. Cybercurrencies have a slightly soft tone.

CUSMA/USMCA Sparks?

A good outcome to today’s possible meeting(s) between Canadian PM Carney, Mexican President Sheinbaum and Trump would be to hear that trade talks have restarted.

Any number of bad outcomes could include variations of Trump issuing threats and insults with no such progress.

The developments start at around 12pmET with the World Cup draw and could run until Carney hops back on his plane by about 7pmET. Social media posts could arrive afterward.

Trump and his highly compliant US Trade Representative Greg Greer both mused yesterday that maybe they’ll walk from the CUSMA/USMCA deal next year when the review kicks in more formally. Righto. I guess there are dumber things that a US administration that is diving in the polls could do ahead of midterms next November than to torpedo its own economy with job losses and soaring prices by killing the agreement, but it’s a short list. We’ve heard such threats before, and they lack credibility.

Listen to the tone of hearings this week and it’s clear that US businesses value the deal. Attempting to kill it would open up a whole series of messy and highly uncertain scenarios for Congress and SCOTUS including the risk of embarrassing defeat right before the vote. The series of events wouldn’t help the Trump administration’s image before voters as one that is weakening America’s international relations and putting the economy at risk. Millions of jobs would be at risk across US border states. We’ve heard this negotiating tactic before, there is no ‘art’ of the deal versus mere chaos and theatre, and it’s all a patient waiting game for however long it takes to negotiate a good—or less bad—outcome without being pushed into a bad deal.

And remember Trump’s tweet in 2019 about the deal he signed: “America’s great USMCA Trade Bill is looking good. It will be the best and most important trade deal ever made by the USA. Good for everybody—Farmers, Manufacturers, Energy, Unions—tremendous support.” Also recall that the CUSMA/USMCA deal changed very little about the original NAFTA deal despite all the hype.

The three heads of state may meet together or separately on the sidelines of the World Cup draw to select match-ups in next year’s tournament. Mixing sport with politics is a great example of how there is no sport that is more politicized than soccer/football and no more politicized head of a sports body than Gianni Infantino.

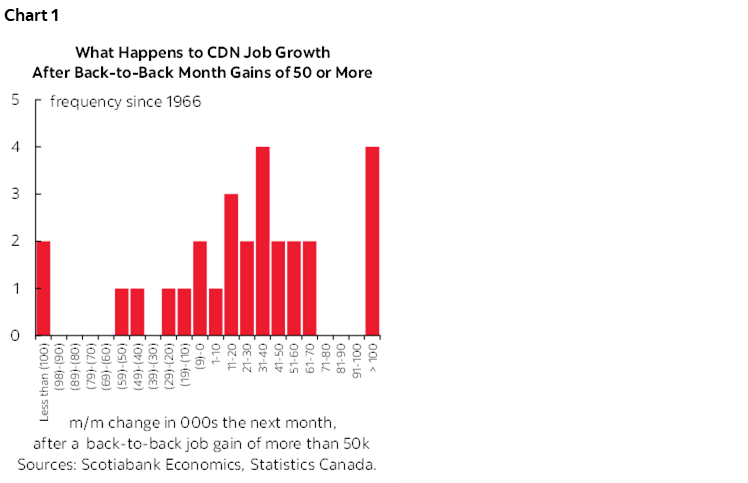

Canadian Jobs—The Trend Will Remain Strong

Canada updates jobs for the month of November along with other metrics like the unemployment rate, the change in the size of the labour pool, wages, hours etc (8:30amET). Consensus is spread out all over the map. Consensus is at -2.5k for jobs, I’m at -15k, estimates range from a low of -25k to a high of +43k. If anyone tells you that only they know the likely divine truth, then run. Fast. I wrote about some possible considerations in my weekly (here). Now let’s do the clean up after seeing the numbers.

And it doesn’t matter. LFS gets revised only once per year unlike rolling monthly revisions in the US. Therefore, it would take a mammoth drop to offset the 127,000 jobs created over the prior two months. In a trade war. The BoC looks at trends, especially for such a noisy report. It has issued clear guidance that it is done cutting and on hold at least for a considerable amount of time barring the emergence of a truly large and sustained shock. For what it’s worth, chart 1 shows what happens the month after two back-to-back strong gains, although none of those prior episodes involved a trade war started by the US.

PCE—Lagging September Data Won’t Change Much for the FOMC

Speaking of data that doesn’t matter, we have the updated PCE inflation, consumer spending and income figures. For September. Yes, September, thanks to Washington’s ineptitude that shut the government for a record period of time. At 10amET instead of the more common 8:30amET. Most estimates are around 0.2% m/m SA for core PCE and a tick higher for headline. Modest growth in incomes and spending are expected. I very much doubt the figures matter to the FOMC on the path to next week’s decision, but may figure into the latest data dependent inputs to their revised projections in the upcoming fresh Summary of Economic Projections and new dot plot.

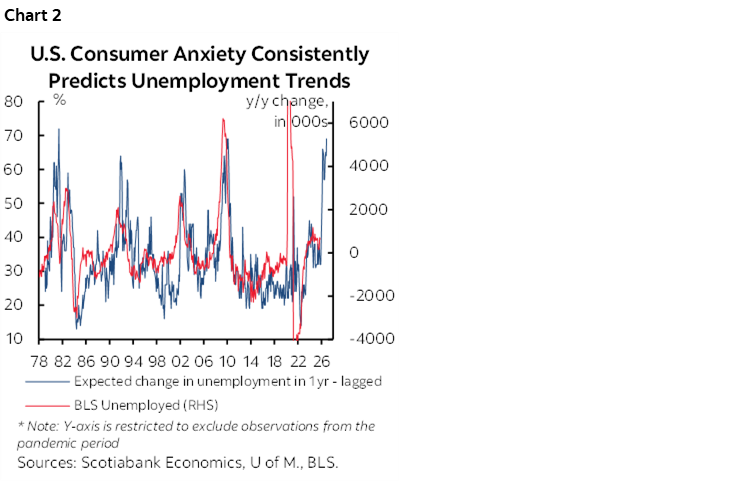

UofM Sentiment—Consumers Accurately Forecast Unemployment

The problem from a markets standpoint is that UofM consumer sentiment for December arrives at the same time as the aforementioned batch of numbers (10amET). It often drives a market reaction and this time that might be tough to disentangle from the PCE reaction.

One measure that cruises beneath the radar that you should watch is expected unemployment over the next year. Chart 2 shows that what consumers expect with a lag aligns very closely with what actually happens. You could argue that’s just spurious and nonsense; that might be a tad arrogant or dismissive. You could instead argue they’re better forecasters than economists and markets. Lots of consumers with their ears to the ground hear the water cooler talk on their employers’ plans and this bubbles up into an aggregated figure that may be insightful. And accurate.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.