ON DECK FOR TUESDAY, DECEMBER 30

KEY POINTS:

- Global markets mixed on the last full trading day of 2025

- Firm Spanish core inflation reinforces prolonged ECB rate hold

- US ADP tracking close to 50k pending today’s weekly refresh

- FOMC minutes will be as stale as three-day old turkey stuffing

- US repeat-sale house prices are falling in real terms…

- …which means a negative wealth effect on consumption for most Americans

- Won tumbles as factory production retreats

Global markets are mixed on the last full trading day of 2025 before tomorrow’s half day for bonds and, let’s face it, everything else. US equity futures are flat, TSX futures are up a smidge along with European cash markets after Asian equities fell in Japan and Seoul but held relatively firmer in China. Sovereign bonds have a tiny cheapening bias. Currencies are mostly little changed except for a drop by the won after a small monthly gain in industrial output disappointed expectations for December after a large plunge in November.

I’ll put out a short Global Week Ahead later today and then regular publishing will resume on Monday.

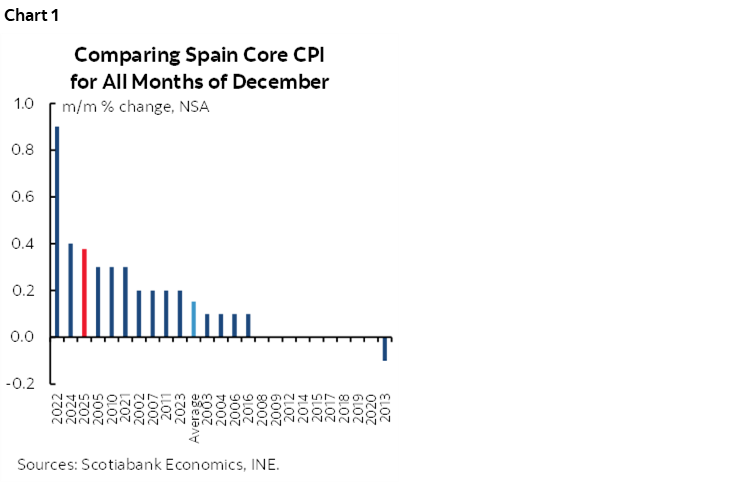

FIRM SPANISH CORE CPI REINFORCES LONG ECB HOLD

Spain’s core CPI inflation held firmer than expected at 2.6% y/y (2.5% consensus, 2.6% prior). On a month-over-month basis it was up by about 0.4% in seasonally unadjusted terms. Since it’s seasonally unadjusted data, we need to compare December to all prior Decembers as done in chart 1 which shows this one was among the warmest on record. Readings for other major Eurozone economies and the Eurozone tally will be available next week.

Markets barely reacted with only a mild cheapening bias across EGBs, probably because markets already expect no policy rate changes by the ECB through the coming year with rate cuts done for the cycle.

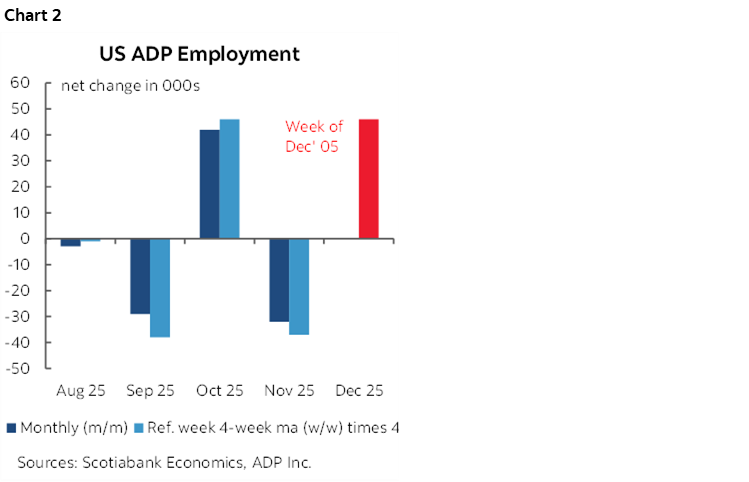

US ADP PAYROLL ARE TRACKING A MODEST GAIN

The US weekly 4-week MA ADP private payrolls gauge (8:15amET) will inform expectations for next week’s monthly ADP reading. Up to the week of December 5th this measure was running at about 46k converted to a monthly equivalent from the 11.5k/week average. Depending upon what we see into this morning’s reference week measure, that could reinforce the recent oscillating pattern of changes (chart 2).

STALE FOMC MINUTES ON TAP

FOMC minutes will arrive as stale as three-day old turkey stuffing (2pmET). Watch discussions around the forward rate path and the rationale for US$40B/mth of liquidity injections and the discussions around the path forward for the balance sheet including after April tax filings. Remember that the minutes are not vote weighted and so they reflect opinions that will overweight some of the dissenting regional Presidents. Also recall that we’ve gotten a lot of data on jobs and inflation since then, much of which has been fabricated. Next week’s nonfarm payrolls matter more than today’s minutes.

US HOUSE PRICES ARE DRIVING A NEGATIVE WEALTH EFFECT FOR MOST

The US also refreshes repeat-sale measures of house prices in October (9amET). What’s important here is that they are falling in real terms (ie: adjusted for inflation). This implies a negative wealth effect for the majority of US consumers who own little by way of equities.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.