ON DECK FOR WEDNESDAY, DECEMBER 3

KEY POINTS:

- Mild risk-on sentiment ahead of US data

- US ADP, ISM-services and IP on tap

- Canadian bank earnings continue to beat the analysts

- Canadian productivity — watch revisions

- America’s disappearing wealth effect

- US auto sales rise, Canadian sales fall

- More evidence China's economy is softening

- European PMI revisions signal more resilience

- Aussie GDP misses, SK GDP beats

- SNB faces renewed negative rate prospects

Markets are in a generally positive frame of mind toward risk assets ahead of US data. Equities are mildly higher and cybercurrencies continue to recover from Monday's sell off—except for the ones affiliated with the Trump family. Sovereign bond yields are generally little changed with slight outperformance in the US. There were a few nuggets on the overnight calendars, but nothing earth shattering from a markets standpoint. The main events on the docket for today are US data including ADP private payrolls and ISM-services, and more Canadian bank earnings after Scotia’s beat yesterday. Other overnight releases are covered below.

Since they started to roll in early October, cybercurrencies have lost US$1.16 trillion in market capitalization versus all US equities that have gained only US$0.4 trillion since then. At US$71.2 trillion, US equity market capitalization still swamps cybercurrencies at US$3.2T, but the changes at the margin are what count. Also note, however, that the too-long-of-a-name-to-mention measure of repeat sale home prices has gone from peak gains of over 20% y/y in 2022 to just 1.3% y/y now; real house prices are falling in the US. The housing wealth effect on consumption matters far more than the equity effect in aggregate and to mainstreet given massive income and wealth disparities in the US system. The effects are probably contributing to some of the softening in confidence measures.

But it could be worse. In the Trump cyber world, American Bitcoin Corp peaked at almost US$100k very temporarily in 2019 and is now worth—wait for it—$2.19. That won’t even buy you a decent cup of coffee.

N.A. DATA UPDATES

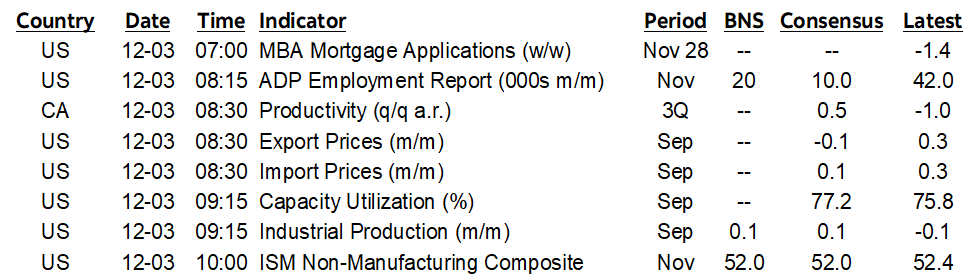

US vehicle sales climbed a touch to 15.6 million SAAR in November after October's drop down to 15.3 that came after the expiration of EV credits. These are still decent levels (chart 1).

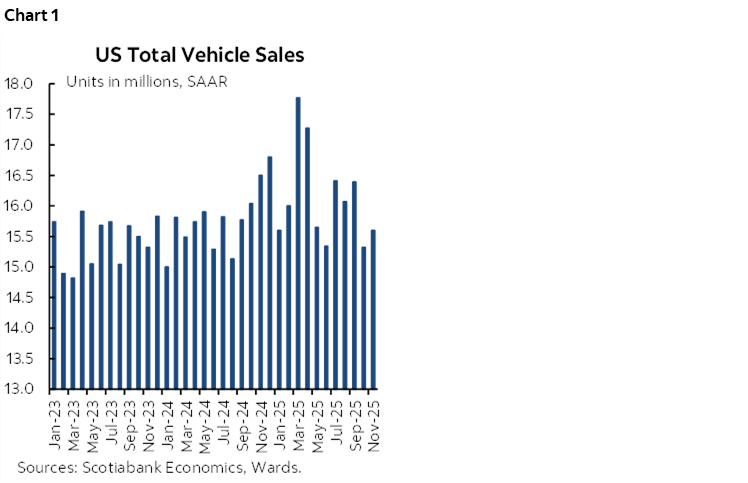

Canadian vehicle sales slipped by about 2½% m/m SA in November after the hottest month for sales since March (chart 2).

A trio of US readings could be impactful to markets this morning.

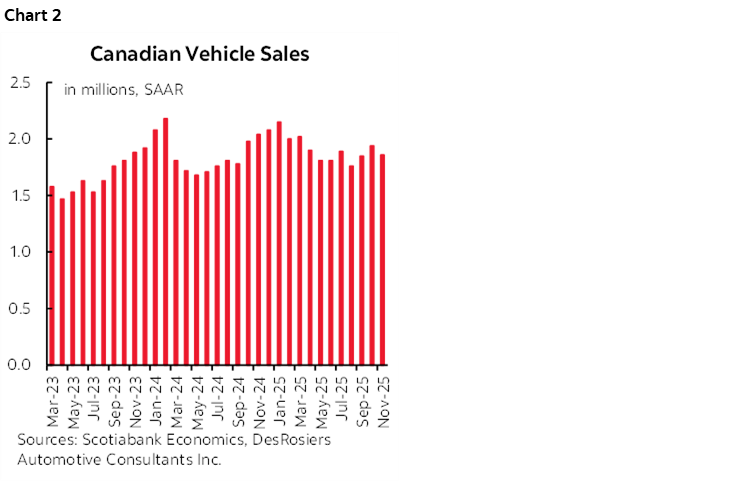

- ADP private payrolls for November (8:15amET): Consensus expects 5k with Scotia at 20k alongside potential negative revisions. Weekly estimates have been deteriorating including after the reference week for October's reading that may suggest a downward revision to that month. That said, the weekly measure doesn't line up very well with the monthly gauge and ADP itself is a poor guide to nonfarm private payrolls (chart 3).

- Industrial output for September (8:15amET): A weak reading with little change is so lagging because of the government shutdown that it may not garner much attention.

- ISM-services for November (10amET): This may show continued moderate growth with solid growth in new orders and sharply rising prices.

Canadian Q3 productivity figures (8:30amET) could post a gain for a change. The main reason is that hours worked were up only modestly (0.4% q/q SAAR). The Q3 GDP beat won't translate through very well to productivity given the import distortions. Also watch revisions to the 2022–24 period after GDP was revised substantially higher last Friday.

OVERNIGHT RELEASES

Swiss inflation was a touch weaker than expected and mildly reinforced markets pricing for a modest chance at returning to negative rates. CPI slipped -0.2% m/m and to 0% y/y. Core CPI is running at just 0.4% y/y. OIS pricing points to only about a one-in-five chance at negative rates on December 11th but half a chance later in 2026. Persistent Swiss franc strength since the start of the year adds to SNB's challenges.

China’s private composite PMI fell six-tenths of a point in November to 51.2 as services softened half a point to 52.1. We already knew that the private manufacturing PMI slipped a touch beneath 50 in November.

There were mild upward revisions to the November purchasing manager indices for the Eurozone (52.8 instead of 52.4) and UK (51.2 instead of 50.5). Germany and France were revised up while first readings showed a higher Italian composite and a lower Spanish reading.

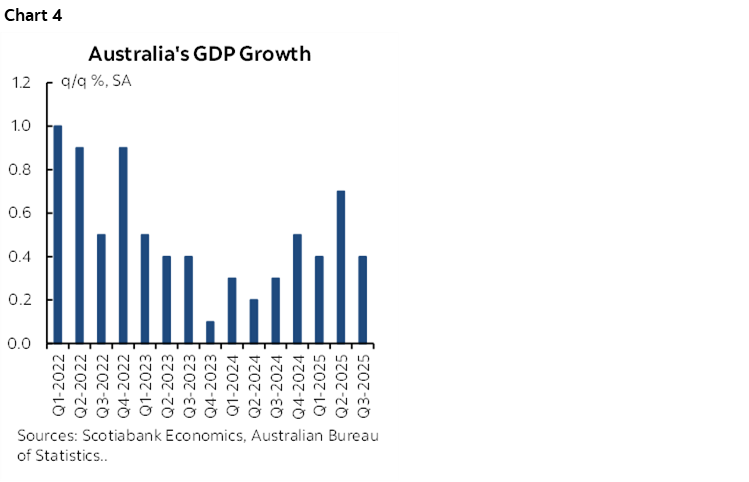

Australian GDP disappointed. Q3 growth of 0.4% q/q SA fell shy of consensus at 0.7% and the miss was only partially offset by a slight upward revision to Q2 (0.7% from 0.6%). Chart 4.

South Korean Q3 GDP slightly beat (1.3% q/q SA, 1.2% consensus).

CANADIAN BANK EARNINGS

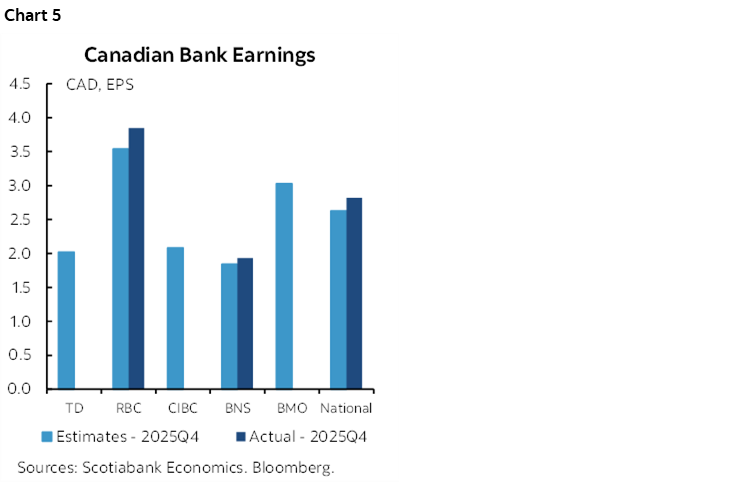

Canadian bank earnings continue to beat after BNS led the way yesterday (chart 5). The analyst community was too negative for three banks and counting so far. A blue and gold bank is the latest (Q4 EPS C$3.85, consensus $3.54 with slightly higher than expected provisions and higher than expected revenues). Quebec’s National Bank also beat (Q4 EPS C$2.82, consensus $2.63 with higher than expected revenues).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.