ON DECK FOR MONDAY, DECEMBER 29

KEY POINTS:

- Global markets are a touch nervous to start a light week

- A global round up of what you may have missed last week

- BoJ reinforces further hike risk

- Light US data on tap

- What’s in store for this week

- Global Week Ahead — Two-Week Holiday Edition (reminder here)

- Canadian Rates Outlook 2026 (reminder here)

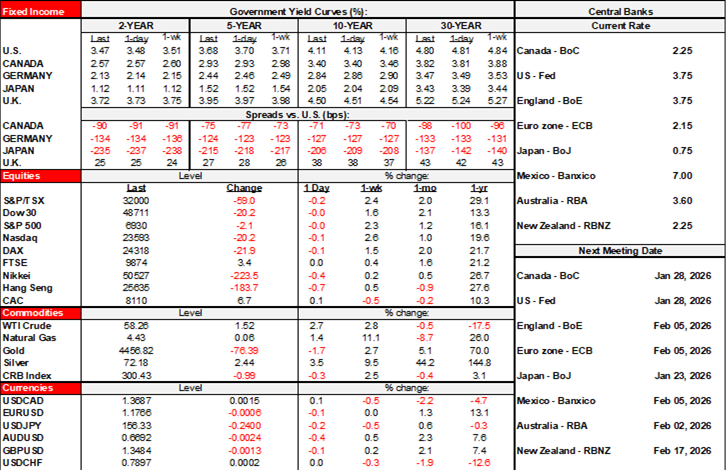

Markets are kicking off the last few trading sessions of 2025 in cautious fashion. US and Canadian equity futures are a touch lower after a weak Asian trading session and with European exchanges slightly in the black so far. Sovereign bond yields are flat to slightly lower across major benchmarks. The dollar is a touch firmer against most major crosses except the yen.

Developments are very light. The Bank of Japan’s summary of discussions in the lead up to the December 19th hike emphasized that some board members view the real policy rate as low and that further rate increases may be appropriate. The 10-year JGB yield edged up a basis point and the yen is slightly outperforming.

There is no breakthrough in Ukraine peace talks which should probably surprise no one; all I can say is Ukraine should have no trust whatsoever for any security guarantees that are worthless. China is doing some saber rattling around Taiwan in retaliation against the US sales of arms. The US will refresh minor readings today including pending home sales during November (10amET) and the Dallas Fed’s manufacturing index for December (10:30amET).

WHAT YOU MAY HAVE MISSED LAST WEEK

What follows is a review of what you may have missed last week when many folks were on holiday. It starts with markets and then global indicators. There was nothing material in terms of policy developments.

Markets—Hello, Santa

Markets were constructive as the Santa Rally held true to form. There was broad dollar weakness as all majors and semis gained. The S&P 500 gained 1.4% but futures are moving a touch lower this morning and with the TSX up +0.8%. The US 10s yield moved slightly lower by 2–3bps with the 2s yield unchanged. The Canada 10-year yield moved down about 7bps with 2s down 5bps. Gold gained US$175/oz last week to temporarily move back above US$4500 before slipping below it this morning. Bitcoin is down by just over US$100.

BoC pricing for nearer term meetings was unchanged but moved about 3bps lower for next October’s meeting to put pricing on the fence between a hold and a hike. Our view is unchanged in that nearer term meetings are unlikely to bring change with the next move likely up but not for quite a while. In the meantime, bidirectional noise will likely govern trading.

Fed pricing remains close to nothing for a change at the January 28th meeting followed by little change for about -15bps at the March meeting and a full cut not priced until June. I wouldn’t pay much attention to market pricing given the market’s poor track record.

Global Indicators—GDP Tracking in Canada, the US and Mexico

Several global indicators were refreshed as follows.

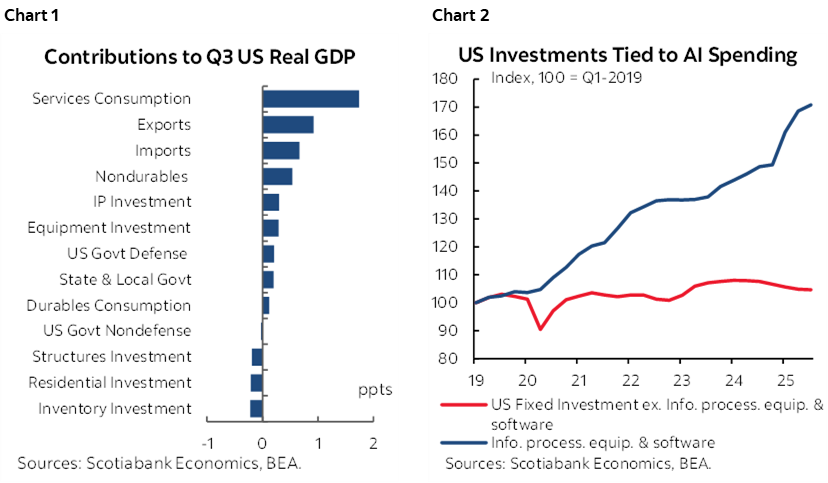

US—US GDP solidly beat expectations, but its relevance is scant to none as a lagging reading that’s too soon to reflect a multitude of policy developments in 2025 and amid forward-looking uncertainties not least of which a weakening job market, tariffs, tight immigration etc. Chart 1 shows that most of the growth came from services consumption and trade. Investment ex-AI related activity was weak (chart 2).

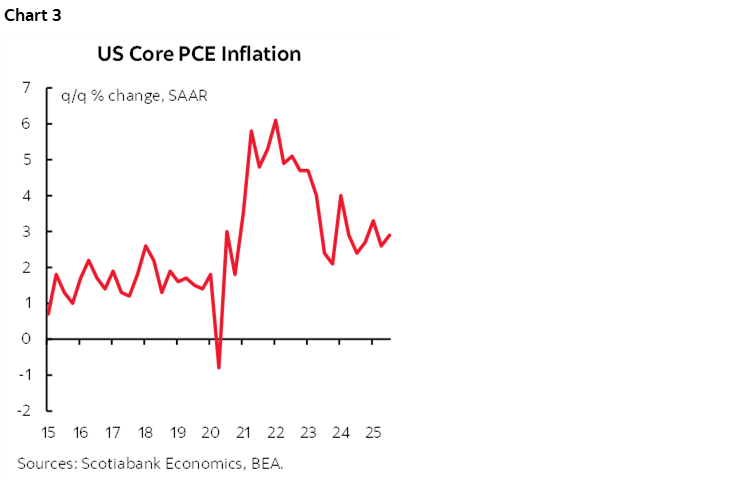

US core PCE inflation pick up to 2.9% q/q SAAR in Q3 from 2.6% the prior quarter but was on the screws. Chart 3 shows the persistent trend of elevated inflation readings.

US core durable goods orders continue to grow with another 0.5% m/m SA gain in December and upward revisions to the prior month for the fourth consecutive gain.

US factory output was flat in November after shrinking by –0.4% m/m in November and has been flat to lower in each of the past four months. No homecoming here.

US consumer confidence slipped entirely due to present situation, as expectations moved up. The ‘jobs plentiful’ reading edged lower.

Canada—GDP on the Screws, Inflation Warning, BoC Cautious

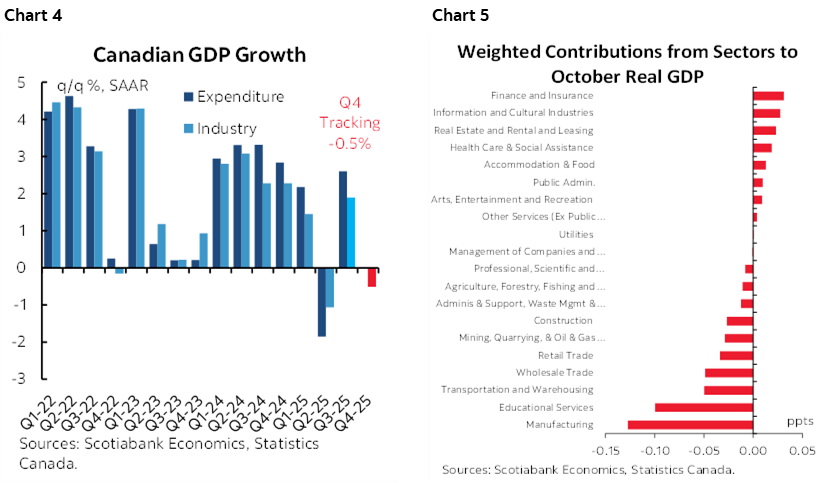

Canadian GDP was in line with expectations. The economy shrank by -0.3% m/m SA in October (consensus -0.3%, Scotia -0.2%) and was guided to have grown by a paltry 0.1% in November on a tentative basis without details. That leaves tracking tentatively at about -0.5% q/q SAAR using monthly, production-side GDP accounts after expenditure-based GDP grew by 2.6% in Q3 and production-based GDP grew 2.1% which was revised up from +1.9% previously (chart 4). What was more important to Canada in my opinion was strong US GDP during Q3, albeit how that holds up going forward will be the key. Chart 5 shows what drove October GDP.

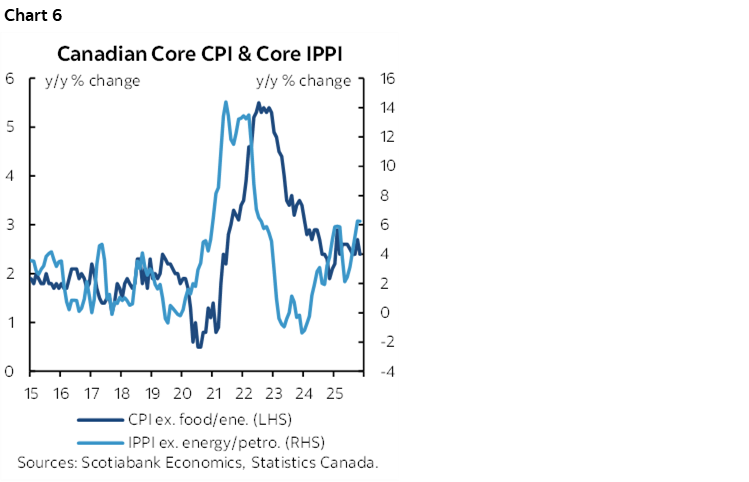

Canadian industrial prices point to a coming inflation surge (chart 6). Industrial prices were up 0.9% m/m in November after jumping by an upwardly revised 1.7% in October. Industrial prices have been up sharply ever since June. How much gets passed through to end consumers is uncertain, but the chart shows the evidence on how industrial price changes lead consumer price changes.

Statcan issued preliminary flash readings for manufacturing and wholesale sales during November that don’t materially impact Statcan’s preliminary estimate of +0.1% m/m GDP growth that month. Manufacturing was guided to have fallen by -1.1% m/m in November which follows a -1.0% m/m drop in October after a large 3.6% gain in September. Wholesale sales were guided to have been flat in November (+0.1% m/m) after a similarly flat reading the prior month.

The BoC’s Summary of Deliberations leading up to the policy decision on December 10th (here) contained little by way of added consequence. They did acknowledge more clearly than they did on statement day that GDP figures including revisions mean “there is likely somewhat less economic slack than previously assessed.” They said CUSMA/USMCA negotiations were a bidirectional risk going forward which wouldn’t shock anyone other than folks tempted to go to only one side of the potential outcomes. In reference to the impact of structural changes affecting global trade, they emphasized that “fiscal and industrial policy measures were the appropriate tools to address this structural transition given that monetary policy cannot restore lost supply.” On the policy rate, the BoC reiterated that it was “at about the right level” to keep inflation close to 2% going forward and that “it was difficult to predict when and in which direction the next change in the policy rate would be.” That reinforces expectations for a waiting period during which no change is expected before the BoC then reassesses developments.

Mexico’s Economy Doubled Consensus

Mexico’s economy surged in October. The monthly economic activity index serves as a GDP proxy and was up by 1.0% m/m SA which doubled consensus, while the prior month’s contraction was revised to be smaller (-0.4% instead of the original -0.6%).

Japan—Bah Humbug

Japan dumped a series of readings on Christmas Day when global markets were shut. Apart from the fact Christians are a tiny single digit share of Japan’s population, it may have been just as well to release that day when no one elsewhere was watching. Industrial output cratered (-2.1% m/m SA, consensus –2%) but retail sales slightly beat (0.6% m/m, 0.4% consensus). Housing starts fell more than expected. Tokyo core CPI edged lower to 2.6% y/y from 2.8% on an ex-food and energy basis.

This Week—China PMIs Shine on an Otherwise Light Calendar

The rest of this week will be very light in terms of calendar-based developments.

Asia-Pacific—China PMIs On Tap

China will refresh the state’s purchasing managers indices with December readings tomorrow night. South Korea refreshes industrial output for November tomorrow and CPI for December the next day.

LatAm—Peru’s CPI the Main Highlight

Several releases are due out across Latin American markets. The main one will be Peru’s CPI for December on New Year’s Day to which I can only say ‘wth??!’. Chile updates several November readings including the unemployment rate (tomorrow), retail sales (Wednesday), industrial production (Wednesday) and the monthly economic activity index (Friday). Colombia updates the unemployment rate (Wednesday). Mexico will update S&P’s manufacturing PMI (Friday).

Europe—Spain Kicks Off Eurozone CPI Tracking

The only thing to watch will be Spain’s CPI for December (Tuesday) that will kick off the march to the rest of the major countries and the Eurozone tally next week.

Canada—Quiet

Enjoy your week. Canada only has S&P’s manufacturing PMI for December (Friday) to consider. Bonds will shut early at 1:30pmET on Wednesday and will be closed for New Year’s Day before business as usual on Friday for anyone who is around.

US—Stale Fed Minutes

We’ll get ADP’s weekly private payrolls measure on Tuesday along with house prices during October. FOMC minutes are due tomorrow but are likely to be stale on arrival in light of two rounds of nonfarm payrolls and inflation readings. The January 28th policy decision continues to rest on key data and developments between now and then. Weekly jobless claims land on Wednesday. Bonds will shut early at 2pmET on Wednesday and will be shut for New Year’s but will be fully open on Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.