ON DECK FOR TUESDAY, DECEMBER 2

KEY POINTS:

- Markets stabilize

- Rate cuts, easier capital rules, fiscal stimulus are normally bullish for markets…

- …with the BoE the latest to ease capital rules

- Eurozone core CPI stabilizes

- BNS posts a strong earnings beat

- US vehicle sales expected to be flat

- Canada may update vehicle sales as soon as today

- Fed’s Bowman to testify on stablecoin rules

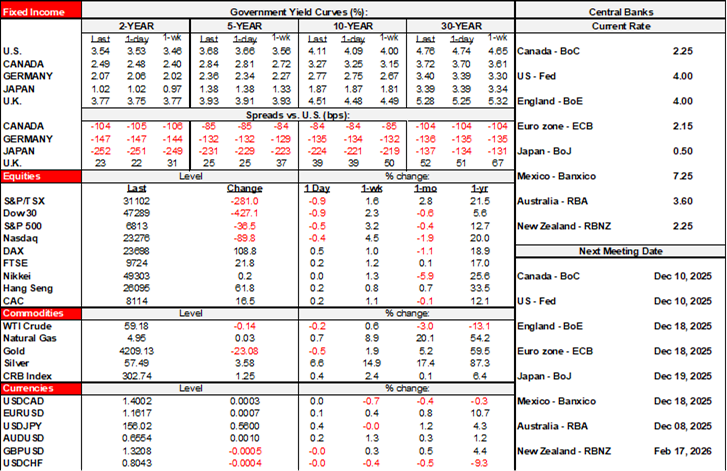

Markets are a touch calmer this morning. Equities are mostly higher across global exchanges, but not by much. Sovereign bond yields continue to rise with minor increases across major benchmarks. Cryptocurrencies are slightly higher after yesterday’s selloff. There are very few fresh developments. Monitor potential US action on Venezuela and pick your motive: fighting drug wars, countering Maduro’s aggression toward Guyana and its rich resources, a virtuous move against a dictator, a quest for a peace prize, or merely a diversionary tactic as polling sinks or maybe a bit of all of the above.

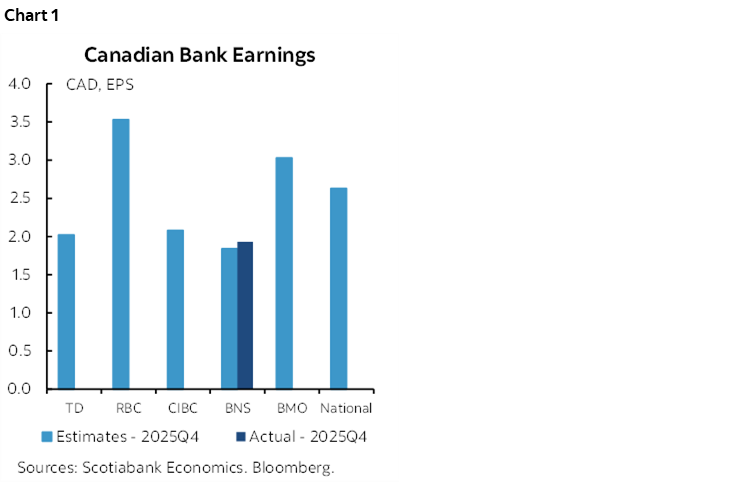

Canadian Bank Earnings Season Off to a Strong Start

BNS (my employer) posted a strong earnings report across the board (here). Adjusted EPS of C$1.93 was well above consensus expectations ($1.84). So were revenues ($9.8B, consensus $9.43). Provisions for loan losses were a little higher than expected ($1.11B, $1.08B consensus). Restructuring charges reflected prior moves. Chart 1 shows expectations for the rest of the banks that release starting tomorrow.

Buried behind the BNS headlines was that long challenged Laurentian Bank was acquired by Fairstone Bank with National Bank acquiring its retail operations.

BoE Eases Capital Rules

Rate cuts, easier capital rules, fiscal stimulus. What’s not to like about the market outlook? In normal circumstances—absent lofty AI valuations—these would be the ingredients to a bullish outlook. The Bank of England is the latest to throw its hat in the ring by easing capital rules applied to banks. The BoE cut Tier 1 capital to around 13% of risk-weighted assets from 14%. Governor Bailey dismissed concerns, saying “It’s a sensible thing to do.” The aim is the foster greater lending activity. The gilts curve is slightly cheaper this morning but not in any different fashion to elsewhere. The moves are parallel to US moves to ease the regulatory framework applied to banks.

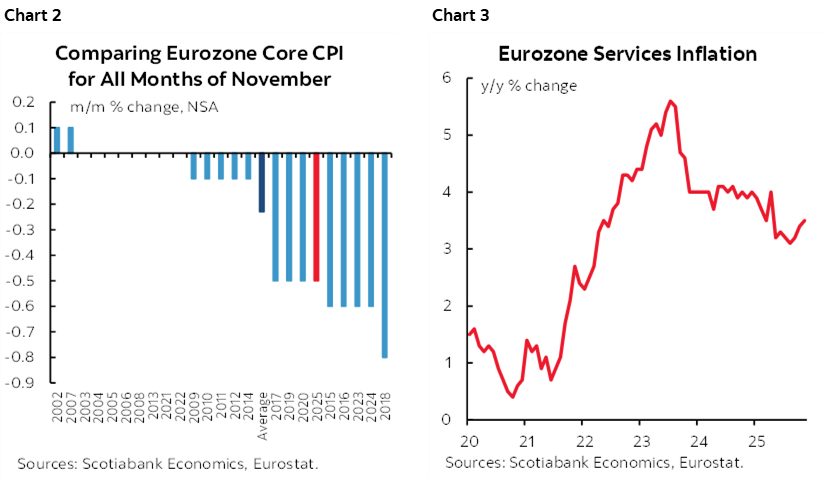

No Surprises in Eurozone CPI

Eurozone core CPI landed on the screws at 2.4% y/y and -0.5% m/m NSA. In month-over-month terms the change was in line with the recent historical average for like months of November that are the comparator since the figures are not seasonally adjusted, but weaker than the full history (chart 2). Total CPI was up 2.2% y/y (2.1% consensus) but slipped -0.3% m/m NSA. Services CPI picked up a bit (chart 3) which will catch the eye of ECB hawks. Consensus was not fully updated after the major economies released CPI figures toward the end of last week. Because markets already had that information there was no real reaction to the data.

Light N.A. Line-Up

An otherwise light line-up lies in store for today. The US only releases vehicle sales for November toward the end of the day with industry guidance pointing toward a flat reading of about 15.3 million units sold at a seasonally adjusted and annualized rate.

Canadian vehicle sales for November may be reported today or soon by Desrosiers but there is no formal release schedule.

Fed Governor Bowman delivers House testimony today (10amET) that will include emphasis upon stablecoin rules.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.