ON DECK FOR FRIDAY, DECEMBER 19

KEY POINTS:

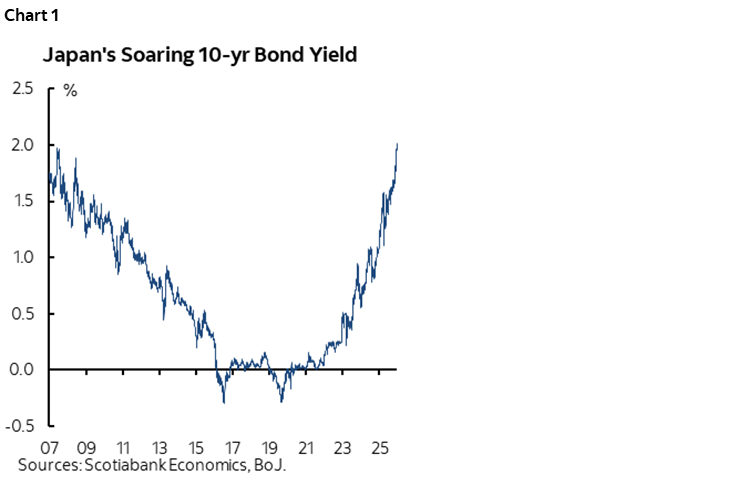

- JGBs, yen part ways post-BoJ hike

- BoJ hikes, Ueda’s customary caginess should not have surprised

- What does Fed’s Williams think of CPI?

- More Fed Chair trial balloons

- US home sales, UMich revisions on tap

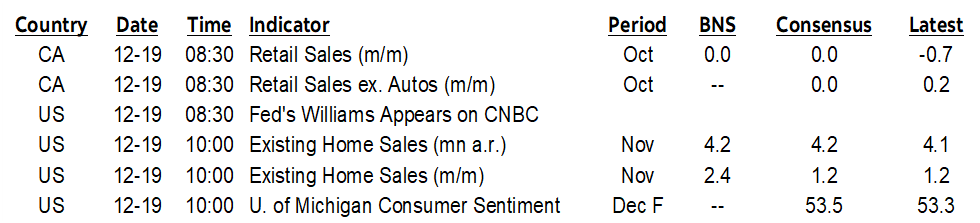

- Two months of Canadian retail sales on tap

- UK consumers say bah humbug

- BanRep likely to hold

- Russian central bank cuts as war’s fiscal toll mounts

This will be the last morning note before the holiday period and I’ll send out two-week Global Week Ahead this afternoon.

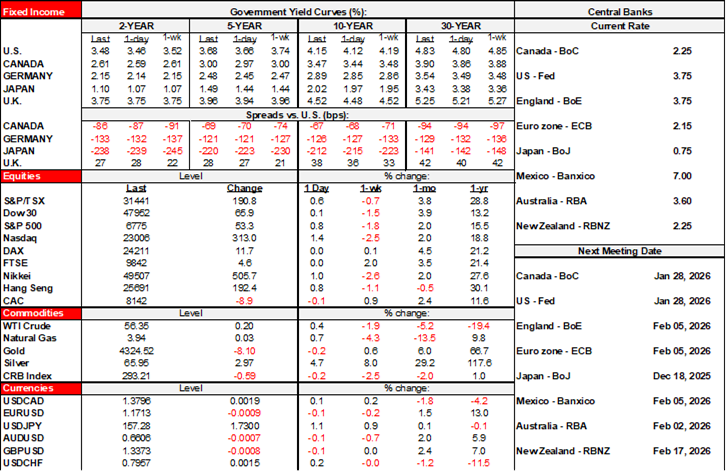

Global markets are ending the last full trading week of 2025 with a touch of apprehension. Bonds are broadly cheaper as sovereign benchmark yields inch higher across markets with spillover from JGBs probably the main culprit. Stocks are mixed, with gains in US futures but mostly flat European exchanges after Japanese equities rallied. The dollar is broadly firmer, but mostly so against the yen.

We’ve heard from the BoJ and Russian central bank with BanRep still on tap as the deluge of pre-holiday central bank decisions last week and this week finally comes to an end. Trial balloons on Fed candidates continue to float with this morning’s headlines touting Governor Waller’s interview performance alongside guidance that BlackRock CIO Rick Rieder will be interviewed soon. Mr. Rieder has had a strong career in fixed income markets but possesses no formal training in economics required for the role in my view.

There is also some modest data to consider including bleak UK consumer spending, uncertain Canadian retail figures, and some US housing data and possible UMich revisions. Key may be how NY Fed President Williams reacts to US CPI this morning.

BOJ — JGBS AND THE YEN WENT THEIR SEPARATE WAYS

The BoJ met expectations for a 25bps hike that raised its target rate to 0.75%. Bonds took the bias somewhat hawkishly as the JGBs curve slightly bear steepened, but not so for the yen that is the weakest major cross to the dollar among the majors. Currency traders either sold the fact and consolidated positions or were disappointed that Governor Ueda did not explicitly spell out the path forward. Of course he wouldn’t do so. Ueda is coy, downright cagey at times, and speaks in code. There were no forecasts offered at this meeting with the last round delivered in October and the next one due with the January 23rd decision which may lean on the numbers a little more heavily to spell out intentions. Markets are pricing one cut by July/September and are leaning toward another in Q4.

WHAT DOES WILLIAMS THINK OF US CPI?

The US focus will include possible reaction to yesterday’s made-up, thoroughly fake CPI data by the NY Fed’s Williams (8:30amET), and light data (new and existing home sales 10amET, UMich revisions 10amET). Fed officials are unlikely to overtly say they don’t trust the data but are likely to offer a nuanced degree of caution. Some are pointing toward the deceleration in y/y rates of inflation as further progress, but that obviously relies on the degree of trust one has October and November data which in my books should be very, very low (recap here).

TWO MONTHS OF CANADIAN RETAIL SALES DUE

Canada releases retail sales for October that may revise preliminary guidance for essentially no growth m/m, plus the first preliminary estimate for November (8:30amET).

UK CONSUMERS MUTTER HUMBUG!

UK consumers were not in a spending mood right up to the cusp of the holiday season. Sales volumes ex-gasoline slipped by 0.2% m/m SA in November after a 0.8% m/m drop in October (revised from -1.0%). They are tracking a decline of under 1% q/q SAAR in Q4 and so it would take a blow out December to rescue the quarter.

COLOMBIA’S CENTRAL BANK LIKELY TO HOLD

BanRep is widely expected to stay on hold at an overnight rate of 9.25% (1pmET). It has been on hold since April. Inflation expectations are back on the rise again. Core inflation has stopped falling and is at 5.2% y/y. COP was appreciating strongly since April but has recently lost some ground partly as US President Trump and Colombian President Petro increasingly lock horns.

RUSSIA CUTS AHEAD OF TAX HIT FROM WAR

The Russian central bank cut by 50bps to 16% as widely expected. Guidance noted that “monetary policy will remain tight for a long period” with inflation running at 6.6% y/y. The government plans a 2% increase in the VAT to 22% because of fiscal pressures emanating from Russia’s war on Ukraine. This is no time to let up on Russia in my opinion.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.