ON DECK FOR THURSDAY, DECEMBER 18

KEY POINTS:

- Markets are constructive ahead of US CPI, ECB

- US CPI: watch the implied two-month average change…

- …in what is otherwise garbage data

- Trump’s address — I want my 20 minutes back

- US tone on USMCA demands is broadly constructive….

- …but only a one-sided opening bid as to be expected

- BoE cut, vote was 5–4 as dissenters favoured a hold, weaker forward guidance

- ECB to stand pat, upgrade forecasts, set low expectations for policy moves

- Banxico expected to cut this afternoon

- Norges, Riksbank both held, both delivered unchanged guidance

- CBCT let its forecasts do the talking

- Shrill cries about Canada’s population dip are unfounded

US CPI and central banks will dominate calendar-based macro risk. Global markets are generally constructive so far, with bonds dearer outside of the UK, and stocks pushing higher. Oil is little changed today after previously rallying.

US CPI—LIMITED INFORMATION FROM GARBAGE DATA

Garbage US inflation data from the BLS will cover the month of November. We’ll only get the y/y rates, no m/m measures, because there is going to be incomplete data for the month of October and hence no real ability to calculated m/m changes. I’m at 3.1% y/y as Scotia’s pick for headline and 3.0% for core, both of which are in line with consensus. They missed the opportunity to collect the October data due to the government shutdown.

At best what you will be able to do is to take November’s core CPI level and figure the percentage adjustment from September’s core CPI level net of any revisions there may be and impute an average m/m SA adjustment to core prices over the two months. If that’s 0.1 or 0.2 or thereabouts, then the market sees the Fed emphasizing the weak payroll figures and cutting at least until we get new information before the Jan 28th decision. If it’s higher, it’s dicier. There will be limited information in this reading in my opinion.

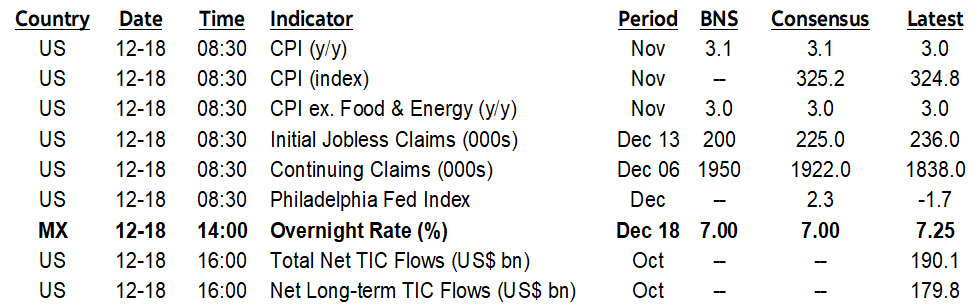

Further, recall all the dents against US inflation data. One example is the record high roughly 40% of the basket that is now being estimated through alternative methods given data sampling and collection issues that pre-date Trump but that his DOGE cuts severely amplified (chart 1). Another example is the made-up seasonal adjustments. Also look at breadth by component in terms of factors like core goods for potential tariff effects, shelter versus ex-shelter, core services etc for underlying drivers. And for this report, the BLS will only collect limited price data for October with most of that opportunity lost to the shutdown.

As for tariff effects, my views haven’t changed. First, tariff pass through is only one subset of supply chain shocks. Second, forget about clear answers with short-term data. The cumulative supply chain shocks from Brexit and Trump 1.0 to the pandemic and geopolitical developments and then Trump 2.0 are rewriting the rule book on supply chains. That will take YEARS to evaluate even though markets may be inclined to think they’ll get all the answers in a handful of readings. That’s just not the way it works. The reverse analog was the multi-decade disinflationary impact of China’s rise along with neighbouring countries.

BoE CUT, DISSENTERS APLENTY, LESS CONFIDENCE IN EASING FURTHER

The Bank of England cut Bank Rate by 25bps to 3.75% as widely expected. The vote was a tight 5–4 as Pill, Greene, Lombardelli and Mann dissented in favour of a hold. Guidance points to further cuts being uncertain. The 2-year UK yield moved marginally higher and sterling appreciated a touch in the immediate aftermath.

RIKSBANK STAYS ON SCRIPT

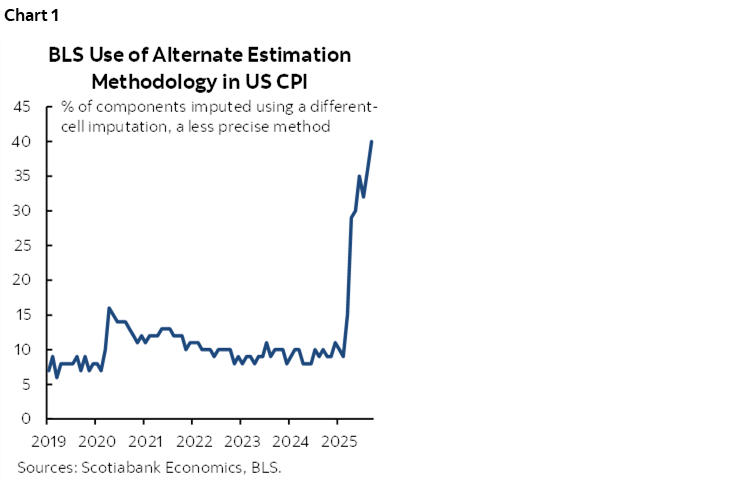

Sweden’s Riksbank left its policy rate unchanged at 1.75% as universally expected. It also left forward guidance unchanged toward a prolonged hold with the next policy rate move likely to be up but not until 2027 (chart 2).

NORGES BANK DELIVERS UNCHANGED STANCE

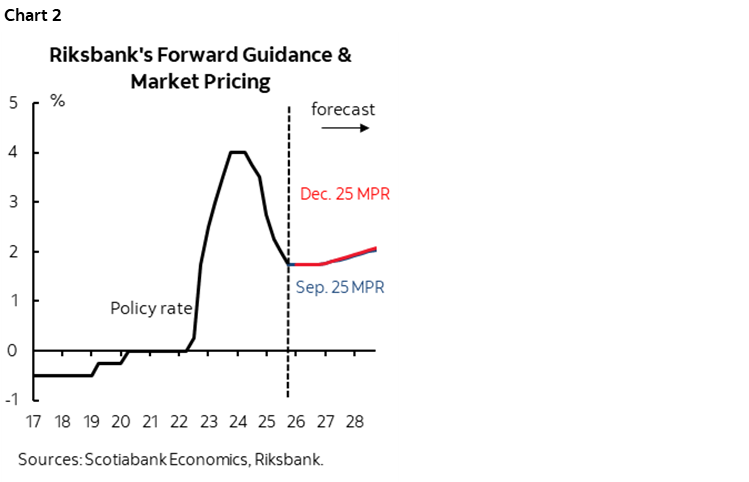

Norway’s central bank also stayed on hold at a deposit rate of 4% as broadly expected. It repeated explicit forward guidance that it still sees room for easing at a one-cut-per-year pace (chart 3). Governor Ida Wolden Bache emphasized “We are not in a hurry to reduce the policy rate.” Norway’s rates curve bear flattened with the 2-year yield up 5bps this morning.

CBCT LETS THE NUMBERS DO THE TALKING

Taiwan’s central bank held at 2% as expected. There is no explicit forward rate guidance, but the numbers did the talking. GDP growth projections were revised sharply higher in 2025 and 2026 while CPI is still expected to be similar in 2026 at 1.6% y/y to the performance this year.

ECB EXPECTED TO HOLD

The ECB is universally expected to stay on hold shortly (8:15amET) with President Lagarde’s press conference to follow 30 minutes later. The tone is likely to be all about the reasons not to expect much from them for a while. Little to no change is expected to the statement. Fresh forwards will be offered and are expected to raise the GDP outlook but they’ve likely been overhyped in relation to small expected changes relative to the private consensus. See my week ahead for more.

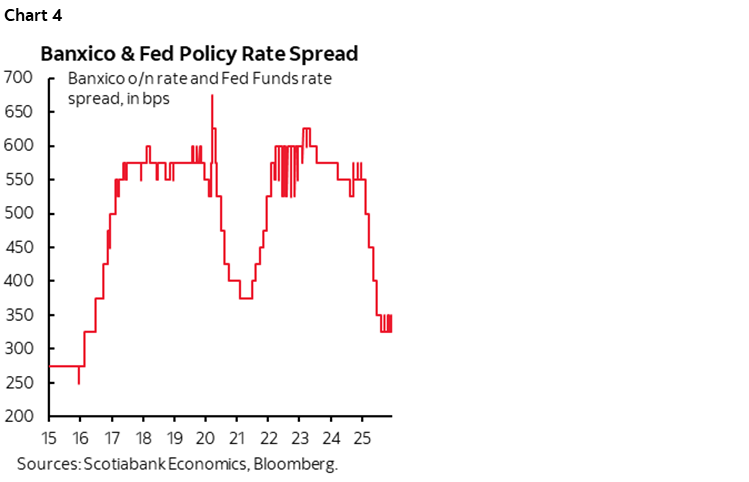

BANXICO TO CUT AS THE HAWKS’ CASE GROWS

Mexico’s central bank is widely expected to cut by another 25bps this afternoon (2pmET). Watch for indications on the bias as the hawks have a growing case in their favour and with the policy rate spread to the Fed at tight levels (chart 4). See my week ahead for more.

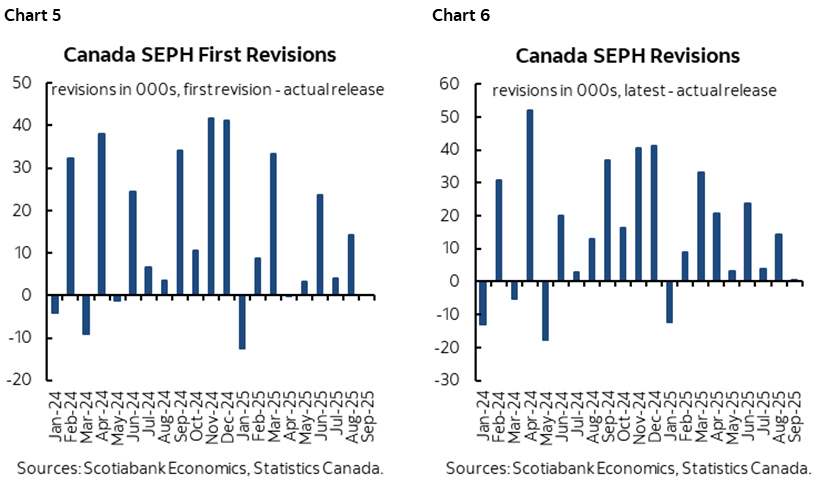

CANADA RELEASES LAGGING PAYROLLS

Canada only releases lagging SEPH payrolls for October. They never matter. They are too lagging, they exclude off-payroll small business jobs by definition, and they are subject to utterly massive monthly revisions to reported employment changes that are commonly in the tens of thousands each month Charts 5–6 show first and cumulative revisions.

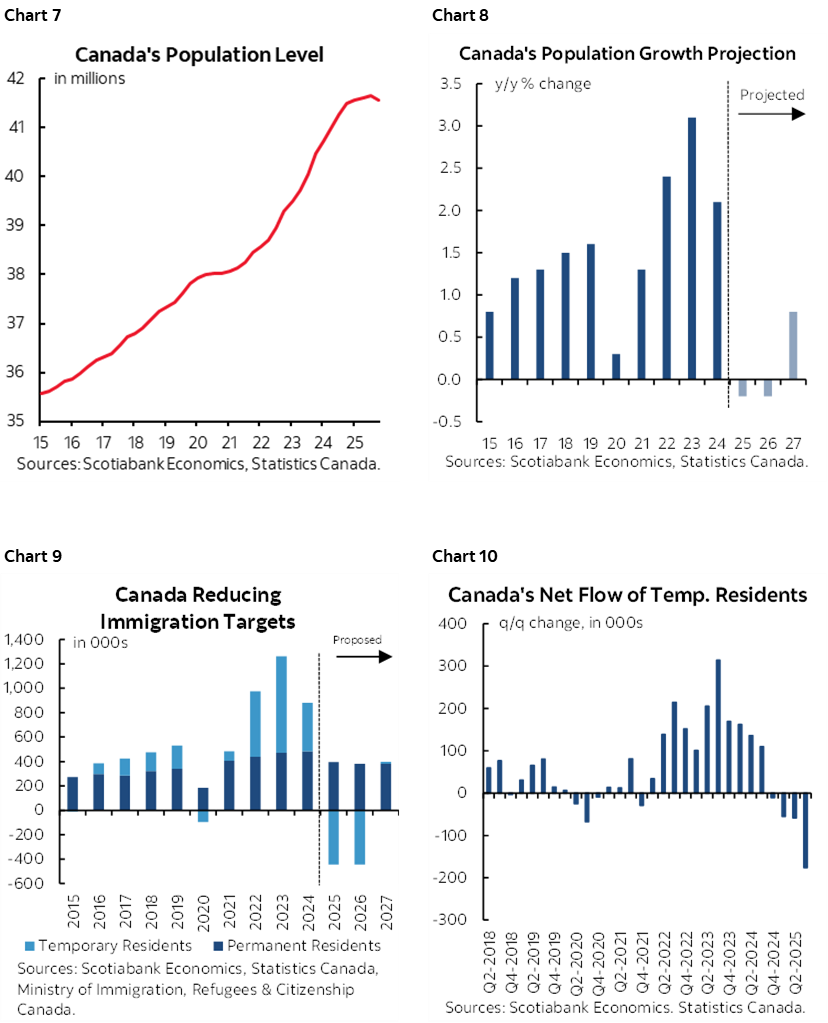

CANADA’S SENSATIONALIST POPULATION HEADLINES

Headlines screamed that Canada’s population decline was the “biggest on record” in Q3. These shrill cries lack balance and miss important points about the reasons and the impact. Charts 7–11 provide context along with the following points.

- One point is to resist viewing it as only a demand side factor as there are offsetting supply side changes in the labour market and broader economy through potential GDP. That’s important to BoC watchers.

- A second issue is that few should be surprised since the pivot on immigration policy changes has been telegraphed for a long while now; the aim is to correct an out-of-control overshoot.

- Third is that population is still up ginormously from 2021 levels (+3.3 million) as the 76k decline in Q3 over Q2 is basically the equivalent to some piddly little hick town in the middle of nowhere.

- Fourth, not all of the folks who arrived in the great surge have pushed through housing and consumer markets; we’re flattering ourselves if we think arrivals from 1, 2 and 3 years ago have been fully assimilated into Canadian society, the job market, the rental and owner-occupied housing markets, business start ups, credit markets, consumer markets etc. That’s just not the way it works so sorry if that rubs the myths about how idyllic Canadian society is that some may subscribe to.

- Fifth, the plan is to scale back on population growth for two years as temps get converted to perms or removed, leaving population little changed whether flat or slightly lower over this period. Then the temps reductions end and population growth resumes.

- And lastly, control for the compositional shift in immigration; the decline is through temps (int’l students, temp foreign workers, asylum seekers) where things really over-shot. Temps fell by 176k in Q3/Q2 while permanent residents increased by 102k. Some temps were likely moved to the perms category. Temps carry a much lower impact upon the economy than immigration through permanent residents. Temps on the international student side were often an abused path to Canada facilitated by fake educational institutions and weak controls.

US LAYS OUT CUSMA/USMCA WISH LIST

US Trade Representative Greer is widely reported to have laid out US demands before both chambers of Congress ahead of negotiations to renew the trade pact. Here are my impressions.

- the broad takeaway is that the USTR emphasized that the majority of feedback garnered from public hearings is supportive of the agreement and wishes it to stay in place. The USTR’s approach is to negotiate while broadly remaining committed to the deal.

- as to be expected, the USTR laid out demands while offering nothing from the US side. Canada and Mexico will likely do the same. It’s to be expected in negotiations.

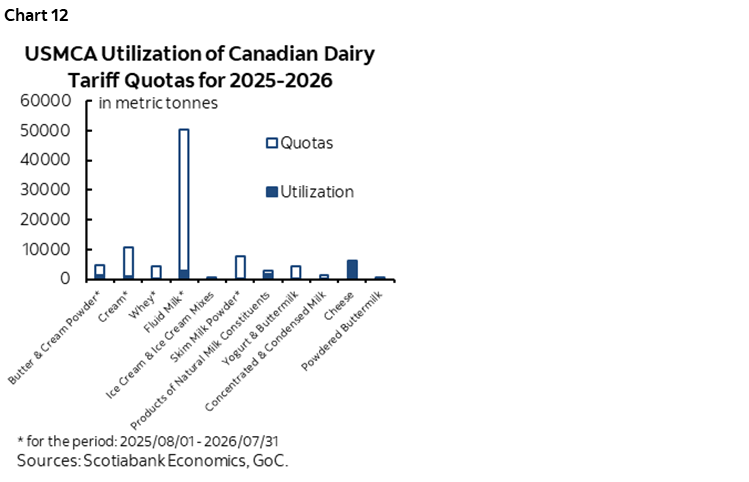

- one of the US demands is to address Canada’s supply management policies surrounding dairy. Don’t hold your breath, Mr. Greer. PM Carney likely puts more important on avoiding a potential constitutional crisis by feeding the PQ’s polling in Quebec into next October’s election than addressing the price of a bag of milk. Further, the US has the exact same quota and tariff system as Canada because Trump agreed to it in the last round, and US producers don’t even use their quotas for export into Canada above which the tariffs would kick in (chart 12).

- the US demands Canada address its Online Streaming Act and the Online News Act as they are perceived to discriminate against US big tech. This is nonsense in my view; how arrogant to demand Canada acquiesce to the demands of the US tech bros who have little to no regard for Canadian culture and policy preferences surrounding it. The Online Streaming Act merely brings US streaming companies under the CRTC’s regulation like others in a level playing field sense; the tech bros just don’t want to have to answer to anybody anywhere. The Online News Act merely requires internet platforms to compensate for using content produced by others rather than ripping them off. More fundamentally, the issue is Canadian fear that an absence of such controls would make for a wild west and greater cultural dominance of US big tech over Canada. It’s the same fear that neighbouring Asian countries have toward China. Large, dominant systems shouldn’t necessarily expect to have their way in exporting their cultures without respect for local preferences.

- the US demands that Canada liberalize procurement programs particularly in the larger provinces. Canada wishes the US would do the same, naturally, with defence procurement at the top of the list.

- the US demands Canada end its provincial bans on imported US alcohol. Recall that the reason for this is in retaliation against US tariffs.

- The US wants Alberta to be nicer to Montana on electricity imports. All I can say on this small issue is, well, whatever.

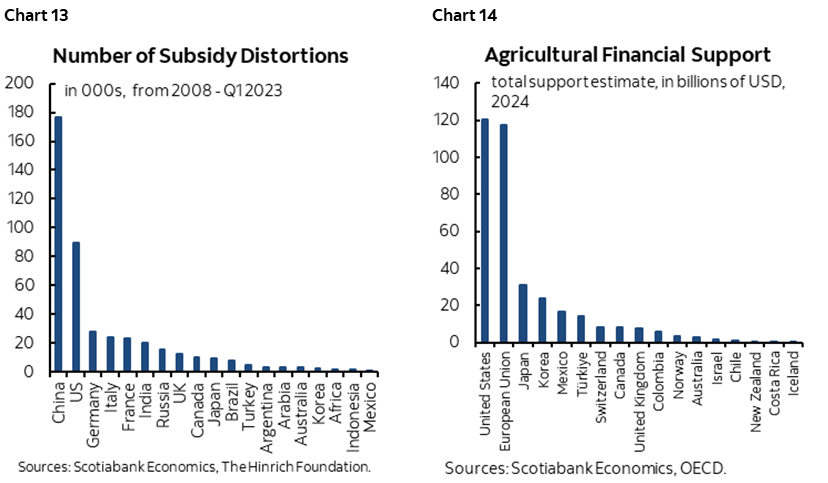

Of course, the US is an angel and offered nothing about its own trade practices. Like hundreds of billions spent annually on subsidies in the US Farm Bill as the US subsidizes agriculture—mainly large corporate farms—more than the Europeans. Like how its southern and Midwest states subsidize global auto companies to locate there, siphoning off investment from northern states and Canada. Like tens of billions in data centre subsidies offered by states as previously cited. Like the so–called ‘chicken tax’ on imported trucks. Like chips and inflation–reduction act subsidies galore. The US ranks highly on its use of subsidies more than others (charts 13–14) and this puts it at an unfair advantage to its trading partners.

TRUMP’S MONOLOGUE—I WANT MY 20 MINUTES BACK

Trump’s roughly 20–minute speech last night was devoid of anything substantively new. He promised US$2.5B to be handed out to soldiers in the form of $1,7776 to 1.45 million military members which is small change in a bigger picture sense.

The rest of the speech was full of mistruths. On example was the claim that prices are falling, when inflation is still about 3% y/y. Another is the claim that the economy and job market are better than ever when in fact Trump inherited nonfarm payrolls on an upward trend that has since gone flat since ‘Liberation Day’ and down after several adjustments described in my nonfarm flash. Further, take AI out, and US investment is falling. A further example is the claim that real wages (ie: inflation adjusted) are performing very well, when they are only up by 0.7% y/y on average and with many Americans below that and with falling real wages.

The speech had the feeling of an angry, denial tone that cited perceived accomplishments while not acknowledging associated turmoil and without paying heed to legitimate concerns of Americans, rather than acknowledgement of the pressures facing many Americans in the job market and in terms of affordability issues.

So why did he deliver it? Maybe it was a sign that the pressure of tumbling approval ratings, a stalled job market and persistent inflation and affordability issues are getting to him on the path to the midterms next November.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.