ON DECK FOR TUESDAY, DECEMBER 16

KEY POINTS:

- Tentative risk off market tone awaits massive US data dump

- US: two nonfarm payroll reports, one household survey, retail sales on tap

- US October payrolls may dip, November may rise—very low conviction on both

- PMIs signal cooler global growth except in the UK

- UK jobs and wages were mixed

- BoC’s Macklem to deliver traditional holiday speech

- BCCh expected to cut

- Eurozone exports plunge

- Is 5% of GDP on defence a total waste of taxpayer money?

What markets are doing now and what markets may be doing shortly once US payrolls roll into town could turn out to be totally different. The coming holiday season is a motivator to data agencies to clear the backlog of US data on top of a deluge of overnight readings.

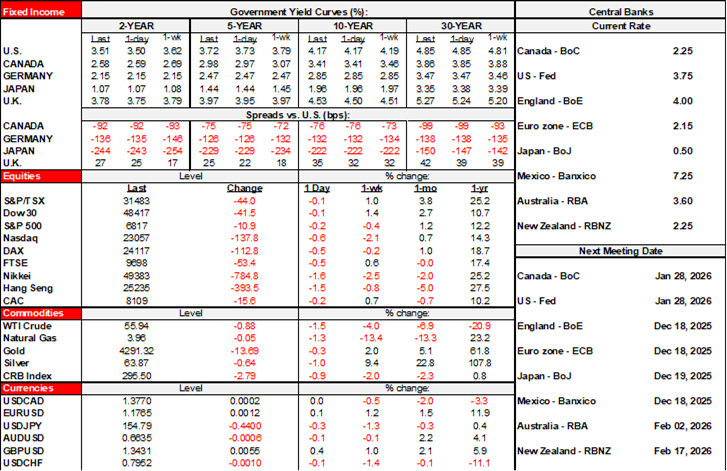

Just for kicks, markets are presently in risk-off mode with US and Canadian equity futures gently lower along with European cash markets and after a weak Asian session that saw bigger declines. Sovereign bond yields are slightly lower across EGBs, slightly higher in the UK and little changed in the US. The dollar is mixed with sterling outperforming.

Weak PMIs everywhere except for the UK were among the overnight catalysts in addition to apprehension ahead of US payrolls.

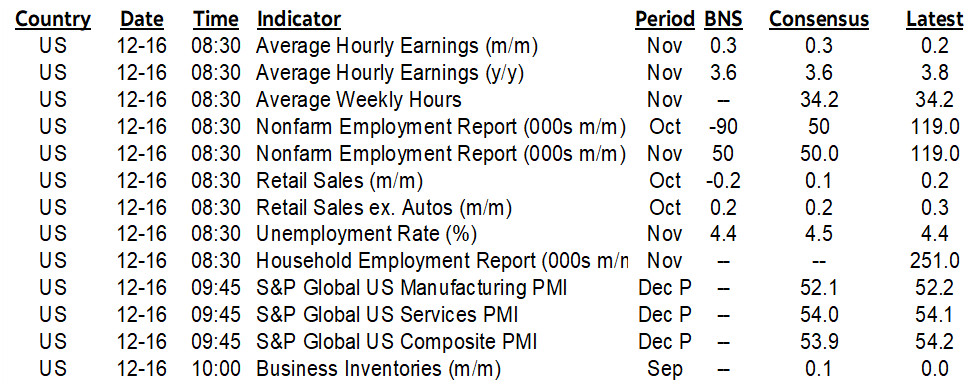

US PAYROLLS, RETAIL SALES ON TAP

High data risk driven by low conviction over the estimates will hit markets. Nonfarm payrolls for October and November will arrive at 8:30amET alongside the household survey for November (October’s was cancelled).

I have the least conviction toward this pair of payroll readings of any readings all year. Estimating November is function of getting November right and getting the jumping off point for October correct which is compounded error risk. That’s on top of falling response rates, wonky SA factors, revision risks etc etc.

Estimating October payrolls involves incorporating a jump in private layoffs, the expiration of DOGE packages in September, and the government shutdown through the payroll reference period that may impact related activities on top of all of the other tracking risk.

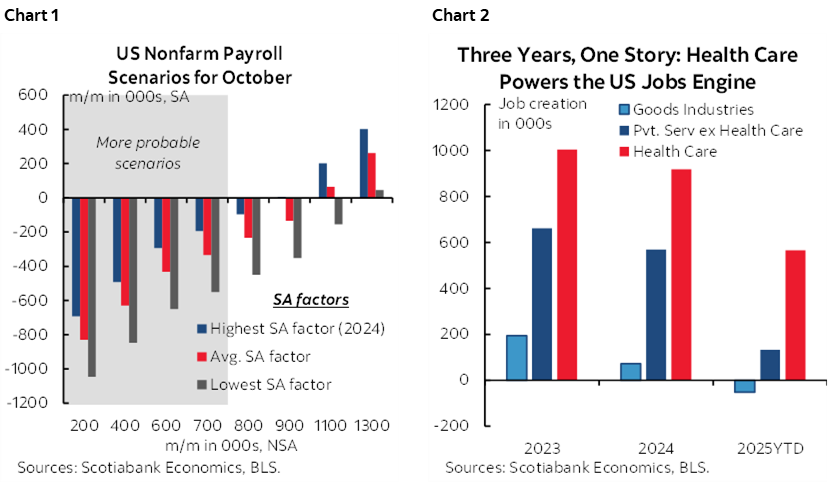

Amnesia hit newswires that forgot to poll for October payrolls that I think could dip. I figure October payrolls could be down (-90k estimate) and November could rebound a touch (+50k) but wouldn’t advise betting the Toronto Blue Jays payroll on it. Scenarios for seasonal adjustments and seasonally unadjusted payrolls slant toward a drop in October (chart 1) and a small gain in November. Also strip out healthcare to get at breadth of hiring or firing (chart 2). See my Global Week Ahead section on payrolls for more (here).

US retail sales are also due out at the same time as payrolls which means they’ll probably be lost in the shuffle. A small gain is expected in nominal terms which would imply that inflation-adjusted sales fell in October. We know auto sales slipped and the gas component and estimate a modest rise in sales ex-autos and gas. The next two reports will be more insightful as they cover the bulk of the holiday spending period.

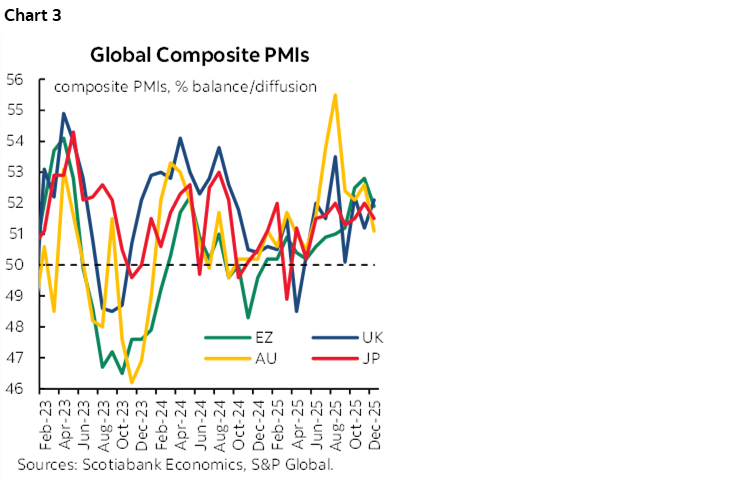

GLOBAL PMIs SIGNAL COOLER GROWTH EXCEPT IN THE UK

With the exception of the UK, purchasing managers indices signalled cooling global growth (chart 3). Here’s the rundown:

- Australia’s composite PMI fell by 1.5 points to 51.1. The decline was driven by weaker services (51.0, 52.8 prior) as manufacturing picked up by six-tenths to 52.2.

- Japan’s composite PMI fell half a point to 51.5 entirely due to weaker services (52.5, 53.2 prior) as manufacturing’s contraction ebbed (49.7, 48.7 prior).

- The UK’s composite climbed almost one point to 52.1 and was driven by higher readings for both services (52.1, 51.3 prior) and manufacturing (51.2, 50.2 prior).

- The Eurozone composite fell by almost a point to 51.9 (52.8 prior) with services mainly responsible for the drop (52.6, 53.6 prior) as manufacturing slightly decelerated (49.2, 49.6 prior).

- India’s composite PMI fell 0.8 points to 58.9 which continues to signal rapid growth. Both services (59.1, 59.8 prior) and manufacturing (55.7, 56.6 prior) cooled.

- US S&P PMIs will be refreshed with December readings at 9:45amET.

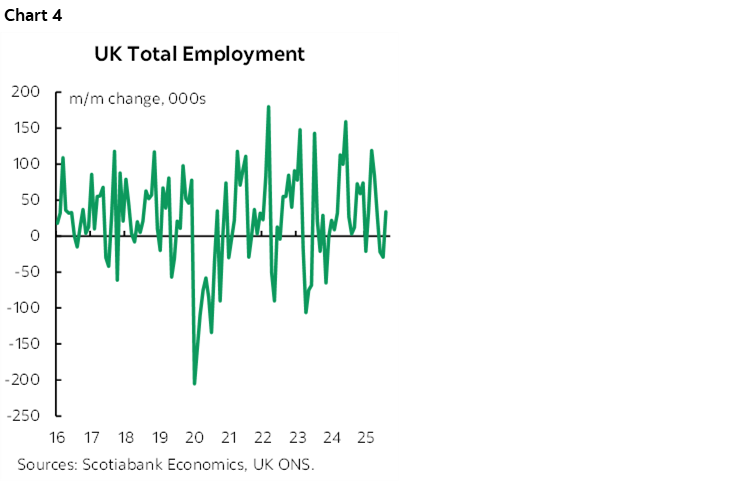

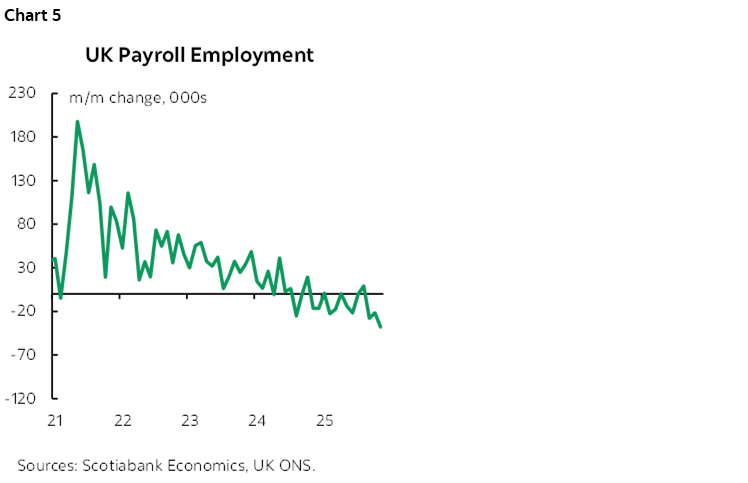

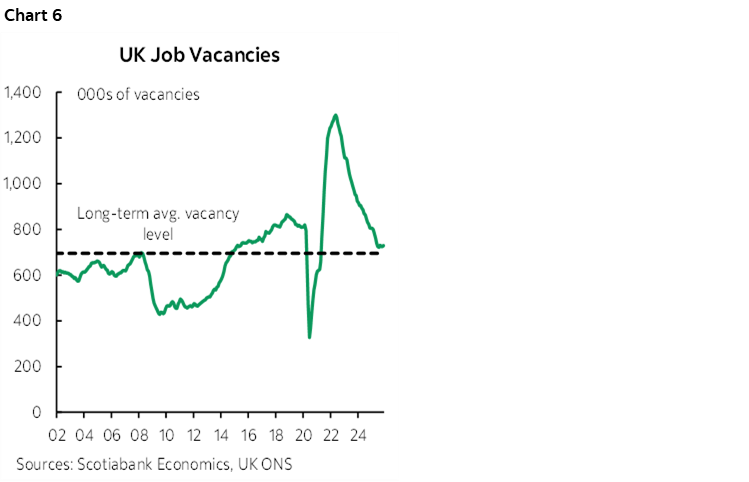

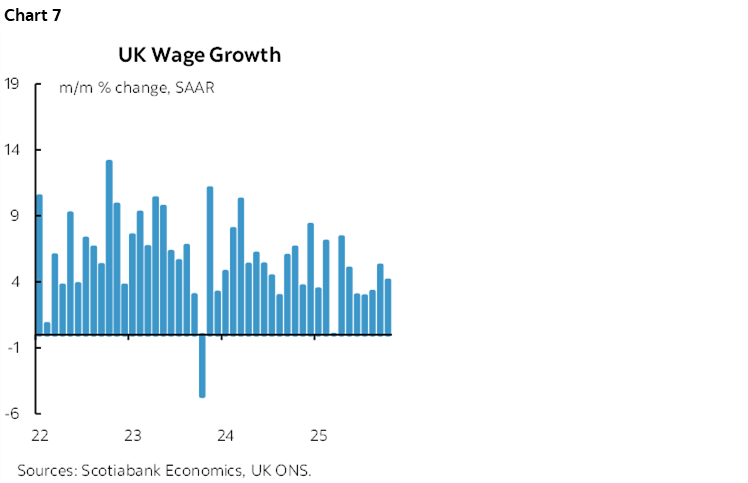

UK JOB MARKET READINGS WERE MIXED

UK job market readings were mixed but generally indicate an underperforming job market. The 2-year gilt cheapened a touch after the 2amET release.

- Total UK employment in October was up by 34k as it rebounded from two monthly declines (chart 4).

- UK payrolls fell by 38k in November which was about twice consensus and the biggest drop since November 2020 (chart 5).

- The UK unemployment rate edged up a tick to 5.1% in October.

- Total UK job vacancies were little changed (+4k) at 729k which remains slightly above the long run average (chart 6).

- UK wage growth landed at 4.1% m/m SAAR in October which remains well above the 2% inflation target (chart 7).

EUROZONE EXPORTS PLUNGED

Separately, the Eurozone’s total exports fell 4.6% m/m SA in October with imports down 3.3% such that the trade surplus narrowed.

SPEECH BY BANK OF CANADA’S MACKLEM COULD GET BURIED

BoC Governor Macklem delivers the Governor’s customary holiday speech this afternoon (12:45pmET). There will be a press conference at 2:15pmET.

Who chose today? In fairness, the BoC has to secure a venue well in advance and may not have anticipated all of the other more important matters to consider.

The topic is anything but clear. The speech title is "Good money and your central bank." Whatever that means.

It's unlikely that we'll hear anything new after last week's decision and communications but the Governor’s holiday speech usually sets the table for the coming year.

Beyond that, maybe the speech title indicates that the topic will be about how 2% inflation control is good for your purchasing power. Maybe it's about Canadian stablecoin and making it sounder than the US legislation. Maybe it's about broad payments reform. Or maybe this one might broach next year's 5-year review. Or maybe all of the above!

BCCH EXPECTED TO CUT

The day ends with a likely cut by Chile’s central bank following Sunday’s election (4pmET).

THE UKRAINE WAR MAY NEVER END

Sorry, but how extraordinarily naïve to claim that peace is near in Ukraine as the US administration continues to side with Putin. The war will never end.

There will always be Ukrainian rebels unwilling to strike peace, infiltrating Russia and contesting territory that Russia steals. Generations to come will hate the Russians for what they've done. Hate the west too for 1994 Budapest and for then caving to Putin and then probably pillaging its resources. Don’t trust the US with its pledge that it will provide security guarantees as you’d be taken as a fool yet again; the US pledge is worthless. Until Putin decides to invade again after retooling once more, whether to claim the rest of Ukraine, or something else. Dysfunction across the West has utterly failed to counter a brutal despot for decades.

Which may make spending 5% of GDP on defence utterly futile. If you’re going to be dysfunctional, lack resolve, lack a spine, and lack coordination, then it won't matter. It won’t make you more secure one bit. It will be like having an enormous sports team payroll but losing every year because you lack character.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.