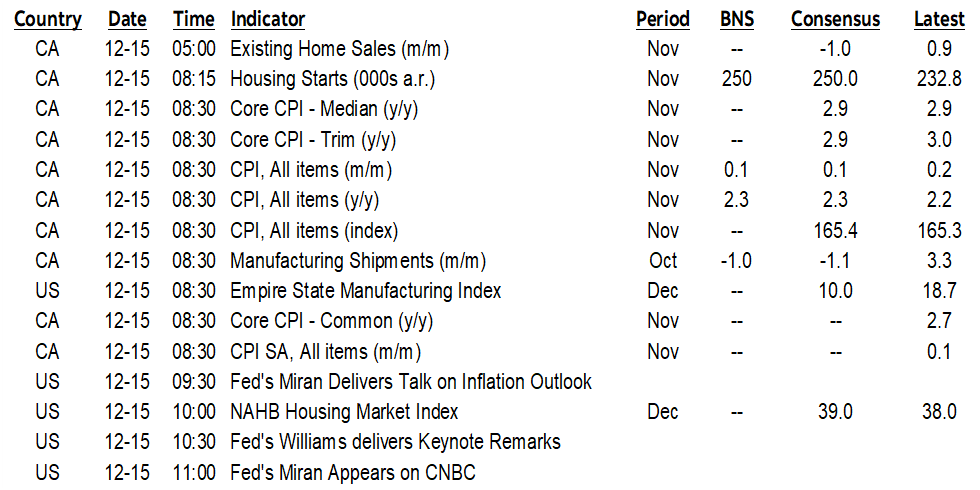

ON DECK FOR MONDAY, DECEMBER 15

KEY POINTS:

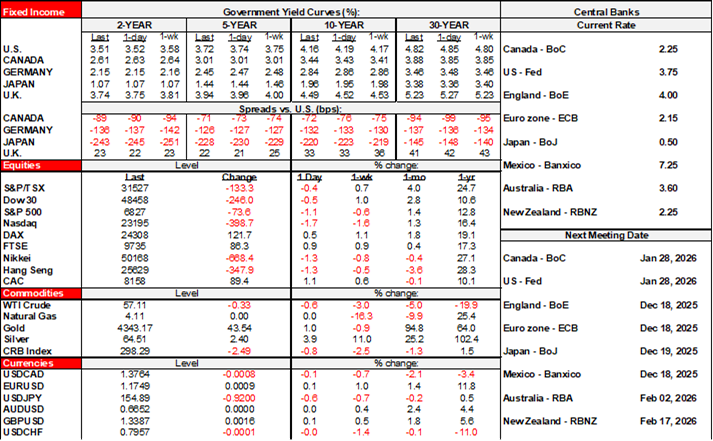

- Markets are in a positive mood outside of Asia

- Canadian CPI—No reason to be blue, it’s only one of two

- Chilean markets likely to respond favourably to election outcome

- China’s economy disappointed in November…

- ...as consumer spending struggles, house prices remain in freefall

- Japan’s Q4 Tankan survey reinforces BoJ Governor Ueda’s resilience

- Canadian home sales slip, housing starts & manufacturing due out

- Global Week Ahead—Too Soon? (reminder here)

The market mood is generally constructive to start a jam-packed week with a dozen central banks on tap, plus two US nonfarm payroll readings, one US CPI reading for November, Canadian CPI (today), and key UK data pre-BoE among others.

Stocks outside of Asia are rallying a touch including mild gains in NA futures and European cash. Asian equities started the week on the back foot with declines across China and Japan. Sovereign bonds are slightly richer outside of Japan.

There are few new catalysts aside from weak China macro data. Most of today's improved risk appetite across western markets could just be a bounce back from Friday's sell off when US tech led the decline.

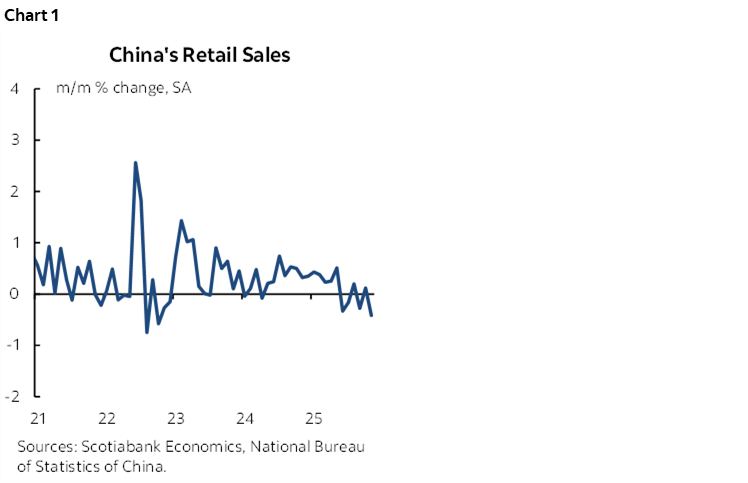

CHINA'S ECONOMY DISAPPOINTS

China registered softer readings for the month of November that indicate growing downside risk for consumers.

Retail sales only grew by 1.3% y/y (2.9% prior and consensus). They have fallen in four out of the past six months in m/m seasonally adjusted terms and posted very mild gains in the other two (chart 1).

What is not helping is that house prices continue to fall with new home prices down -0.4% m/m for the thirtieth straight decline and for a y/y decline of just under 3% (chart 2). Resale home prices were down 0.7% for the 31st straight drop. Falling house prices mean relatively inelastic demand for money as we see in the previously covered figures for financing activity at the end of last week. Folks who aren’t buying homes are less likely to buy the junk we put in them.

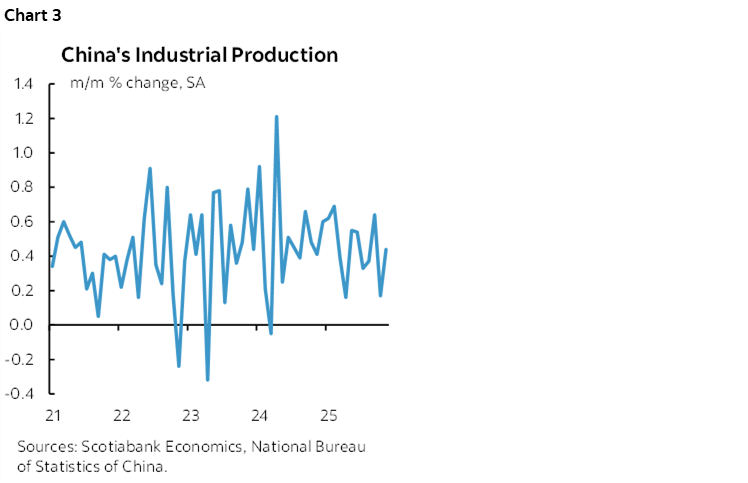

Industrial production slightly missed expectations at 4.8% y/y (5% consensus). That has been holding up a bit better (chart 3).

CHILE'S ELECTION LIKELY TO SUPPORT RISK APPETITE

A classic right versus left final round led to victory for the right wing candidate in yesterday's Chilean election. It wasn't even close. José Antonio Kast won an estimated 58% of the popular vote and handily defeated the communist candidate, Jeannette Jara. The outcome was generally expected after the first round election revealed strong support for right-of-centre candidates that coalesced around Kast. American writers interpret this as a hemispheric turn toward more conservative leaders because of Trump, assuming Trump is conservative, which I doubt, while also ignoring Canada’s election outcome earlier this year. Maybe, just maybe not everything revolves around the US versus local drivers. Did I mention the other candidate was a communist??!

The COP is appreciating slightly early in the Monday session which extends the currency’s terrific run since early April during which it has appreciated by about 10% to the dollar.

JAPAN'S TANKAN POINTS TO RESILIENCE

Japan’s Q4 Tankan survey registered small improvements at large and small manufacturers as well as smaller non-manufacturing businesses but unchanged readings at larger non-manufacturing businesses.

CANADIAN CPI HEADLINES CANADA FOCUS

Canada updates one of two CPI readings before the next Bank of Canada meeting on January 28th. They may impact markets but I wouldn't look for any serious policy implications with the BoC signalling a prolonged pause and in more of a forward-looking mindset.

The November reading (8:30amET) is expected to post a soft headline gain of 0.1–0.2% m/m seasonally unadjusted that would leave the year-over-year rate around 2 1/4%.

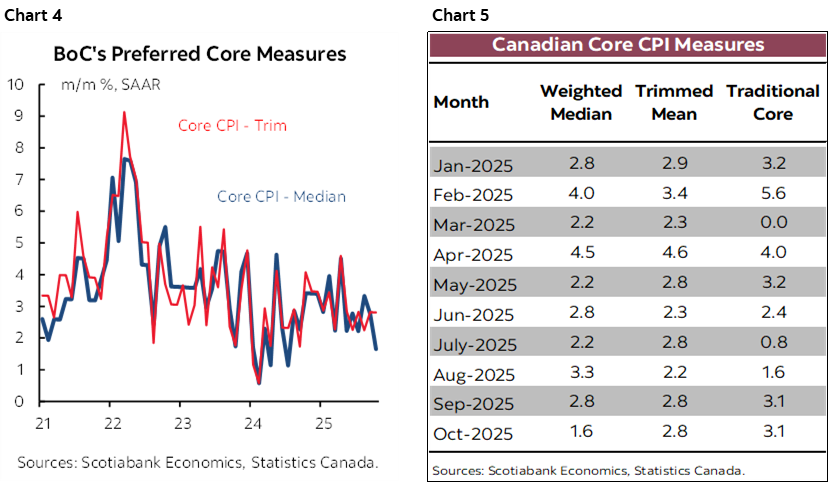

Key will be core measures. They're not exactly cool as charts 4 and 5 demonstrate in m/m terms and seasonally adjusted at annual rates.

Canada also offers housing updates today. Existing home sales slipped by -0.6% m/m SA and were down by just over 10% y/y. Sales have fallen in two of the past three months. New listings were down 1.6% m/m, signalling a lack of new supply held back sales. The sales to listings ratio moved up half a point to 52.7%. Months of inventory stood at 4.4 and has been floating around that level for five months.

Housing starts are up next (8:15amET).

Finally, manufacturing conditions in October (8:30amET) are expected to retreat somewhat from September's huge 3.3% m/m SA gain in shipments.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.