ON DECK FOR THURSDAY, DECEMBER 11

KEY POINTS:

- Mixed markets post-FOMC as tech earnings disappoint alongside local market drivers

- China loosely pledges stimulus, faces inelastic demand for money

- Aussie jobs disappoint, drive A$ weaker, bonds richer

- Mexico sets a high price for Trump’s affections

- CHF rallies as SNB indicates a high bar for negative rates

- BSP signals end of easing campaign, peso rallies

- Brazil’s central bank held

- US, Canadian trade figures could inform Canadian GDP revisions

- Lira barely flinched after Turkey’s mega cut

- US jobless claims on tap

- SCOTUS IEEPA decision could come at any moment

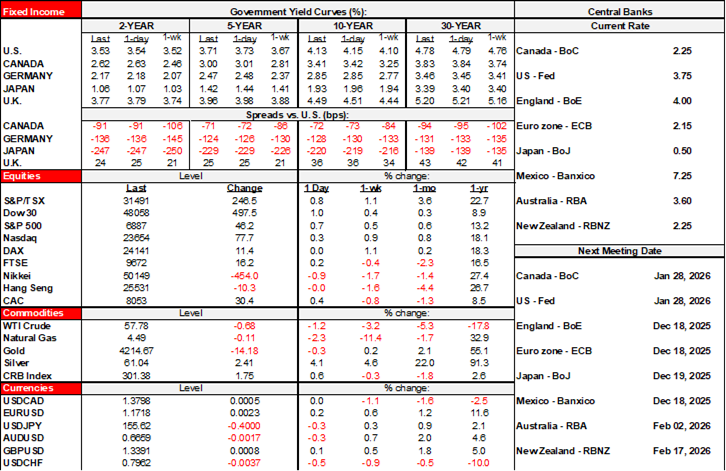

Overnight markets were mixed post-FOMC that drove rallies in Treasuries and equities yesterday afternoon (recap here). Canadian markets are still pricing a hike by late next summer with September’s meeting fully priced after yesterday’s BoC decision (recap here).

Asian equities generally pushed lower in Japan, China and South Korea, while European equities got a bit of a lift. Sovereign bonds are slightly dearer across Europe and with a similar bias in US Ts this morning. US equity futures are being dragged somewhat lower this morning on tech earnings as Oracle’s results spill over. Currency markets are divided with outlier moves explained by localized developments like central bank decisions and Aussie jobs (see below). On tap is light data out of Canada and the US with most of the emphasis upon implications for Canadian GDP revisions.

CHINA SIGNALS EASING AHEAD

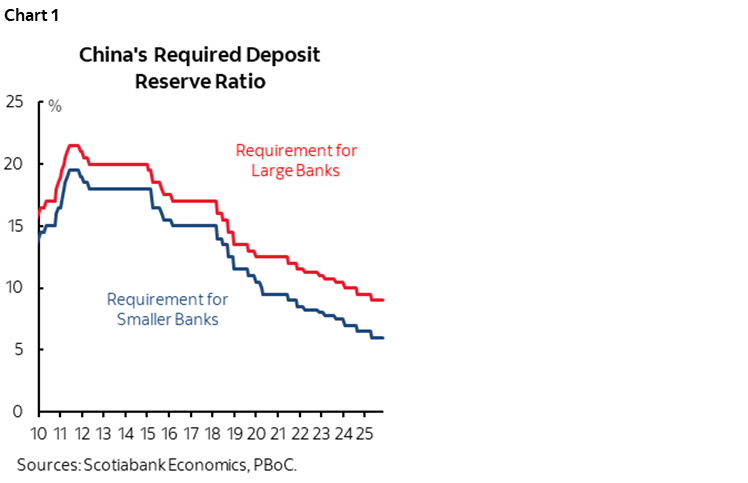

China’s Central Economic Work Conference wrapped up with guidance that “moderately loose” monetary policy to counter very weak inflation will be accompanied by “more proactive” fiscal policy next year. That sounds like rate cuts and required reserve ratio cuts alongside unclear fiscal targets. Chinese equities were left unimpressed. China, however, faces relatively inelastic demand for money that may not respond to easier monetary policy. Constantly falling house prices create reticence to take on big liabilities. Years of cuts to required reserve ratios won’t necessarily spawn increased borrowing on either the supply or demand sides (chart 1).

WHAT PRICE IS TOO HIGH FOR MEXICO?

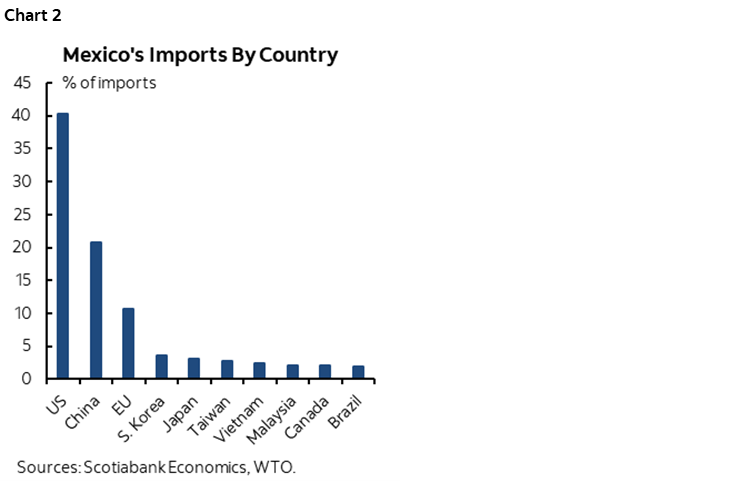

What price is too high to avoid the wrath of Trump? Mexico may be on the verge of finding out. The country approved tariffs of up to 50% on Chinese and other Asian imports but with most of the focus on China. Chart 2 shows the large share of imports coming from China. Trade diversion is possible, but still, the outcome is likely to drive Mexican prices higher as the effects rattle through the economy. Bear in mind, however, Trump’s threats to impose tariffs while demanding concessions including access to water. That should concern Canadians; the US has been trying to get Canadian water since the 1980s trade negotiations but it has been a consistently firm red line for many reasons not least of which because of poor water conservation practices stateside.

AUSTRALIAN MARKETS RATTLED BY JOBS

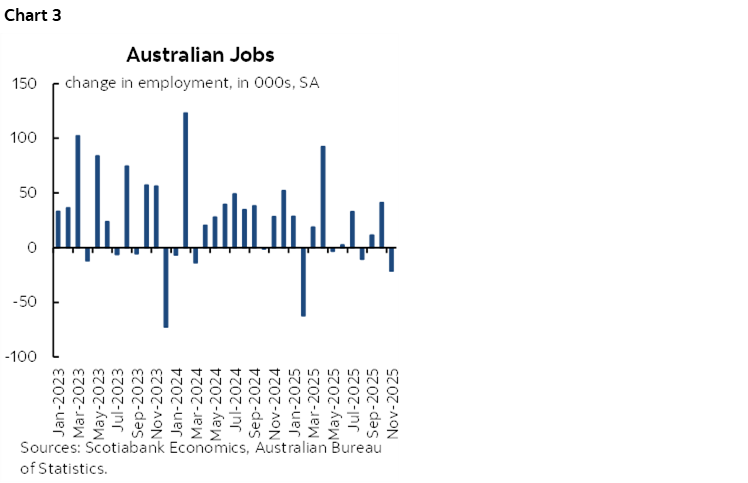

Australian markets were rocked by a weak jobs report for November. The A$ is the weakest major cross to the dollar this morning and Australia’s rates curve rallied by about 9bps across most maturities except slightly less at the long end. Employment fell by 21k as full-time jobs fell by 57k and part-time fell 35k. Chart 3. The unemployment rate nevertheless stayed unchanged at 4.3% because folks exited the workforce. The labour force participation rate slipped by two-tenths to 66.7%. The RBA would look at trends whereas markets don’t. The country gained 52k jobs over the prior two months and is up by 130k ytd with one month left.

SNB SETS HIGH BAR FOR NEGATIVE RATES

The Swiss franc heaved a sigh of relief post-SNB to become the strongest of the major performers this morning. The Swiss National Bank held its policy rate unchanged at 0% that was universally expected. Key was the bias. While President Schlegel said they are open to returning to negative rates if needed, the broad tone dampened speculation the SNB may be moving there anytime soon. The SNB lowered its inflation forecast a touch to just 0.2% y/y in 2025, 0.3% next year, and 0.6% the year after. Schlegel downplayed the forecast revisions, deflected any sense that the inflation outlook makes negative interest rate policy more likely, and indicated a willingness to intervene if CHF strengthens. Clearly they view a return to negative rates through a different light this time around, or they’re wrong and we’ll see in 2026.

BSP SIGNALS END OF RATE CUTS, PESO RALLIES

Bangko Sentral ng Pilipinas cut its policy rate by 25bps to 4.5% as widely expected. No surprises this time. Governor Remolona indicated that rate cuts “may have ended already. This may be the last cut.” That bias drove the peso higher. Take it with a grain of salt given BSP’s proclivity toward surprises.

BRAZIL’S CENTRAL BANK STRUCK A SLIGHTLY MORE NEUTRAL TONE

Brazil’s central bank held its Selic rate unchanged at 15% last evening as widely expected. The tone of the statement and forecasts was a touch more neutral but indicated no rush to ease.

LIRA SHAKES OFF MEGA CUT BY TURKEY’S CENTRAL BANK

Turkey’s central bank cut by 150bps to 38% on the one-week repo rate. A little less than half of consensus expected -150bps with a slightly larger contingent at -100bps. The lira barely budged.

TRADE FIGURES COULD DRIVE CANADIAN GDP REVISIONS

On tap into the N.A. session will be a batch of Canadian and US trade figures for September (8:30amET). Normally we get the US advance merchandise figures before the full set of accounts that are due today, but that advance report was a casualty of the shutdown. Ergo, today’s figures will be the first look at US trade in September. By corollary, we’ll get the first glimpse at Canadian trade that month now that the US side is back to collaborating on data.

The figures matter more to Canada than the US. That’s because of the role that imports played in propelling Q3 Canadian GDP to 2.6% q/q SAAR. That was based on made-up trade figures in the absence of anything more concrete. There could be implications for GDP revisions, but we can’t tell the direction and magnitude until seeing the numbers.

The US also updates weekly claims data (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.