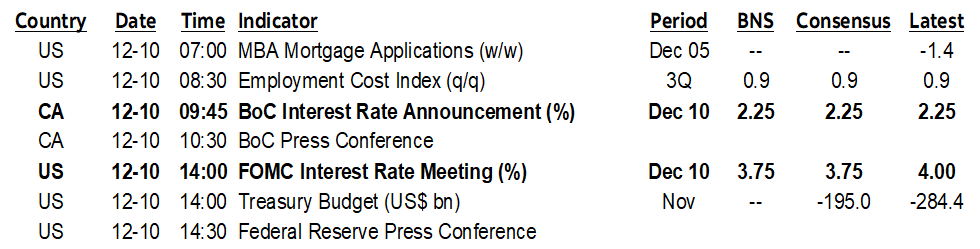

ON DECK FOR WEDNESDAY, DECEMBER 10

KEY POINTS:

- Bonds and equities cheapen ahead of the Fed…

- ...partly driven by BoJ, ECB comments

- Expectations for several global central banks are pivoting to neutral-hawkish stances…

- ...that could bring dollar weakening to do some of the Fed’s work

- Why the Fed has no choice but to cut today…

- …why the dot plot could closely resemble September’s…

- …and why whatever they say will be quickly faded

- BoC to hold today…

- …and possibly increase upside risk to inflation outlook

- SCOTUS might deliver IEEPA decision as soon as today

So long, 2025! That sentiment has to be front and centre in the minds at the Federal Reserve and Bank of Canada. Today brings the final policy decisions of a very long year and with the added risk that we could hear from SCOTUS on the IEEPA tariffs at any moment. Last minute reading is available here including BoC and Fed previews, and here for a Canadian rates outlook.

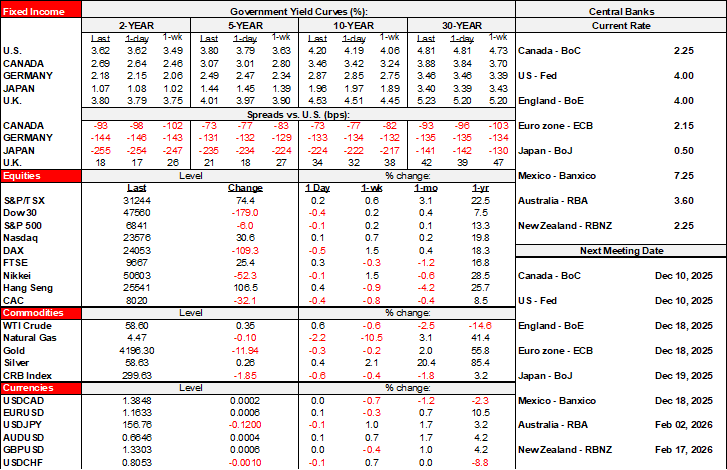

Sovereign bond yields are pushing gently higher into the decision. Equities are pushing gently lower. Cheaper bond and equity prices are signalling unease toward the Fed’s stance. The dollar is little changed against most major currencies.

Added developments may also be contributing to higher yields. BoJ Governor Ueda flagged resilience of the Japanese economy in the face of US tariffs ahead of next week’s policy decision that is mostly priced for a 25bps hike. ECB President Lagarde indicated that growth forecasts for the Eurozone economy are likely to be raised again in next week’s communications while Governing Council member Simkus weighed in against any further rate cuts.

Note the broadening tone across central bank expectations. Markets are leaning toward hiking in 2026 by the Antipodeans (RBA, RBNZ), the Bank of Canada, and the BoJ while the ECB’s bias is increasingly shifting toward a neutral-hawkish stance. If that happens, the dollar weakening that could ensue could do some of the Fed’s job.

FOMC—CUT, THEN SHRUG UNTIL MASSIVE DATA DUMP

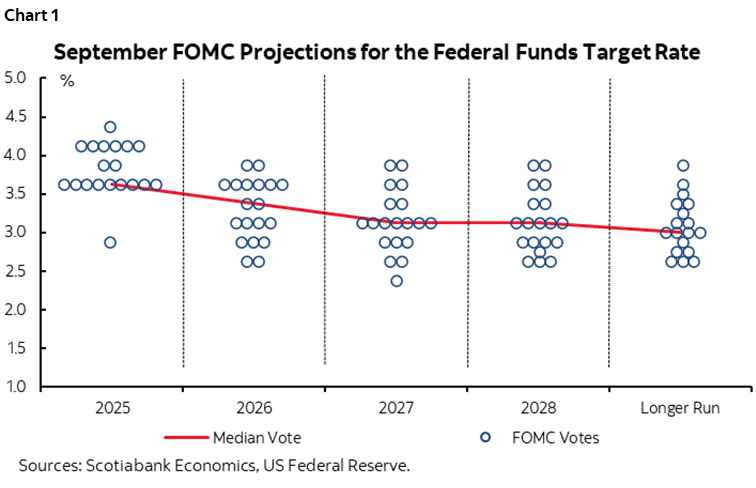

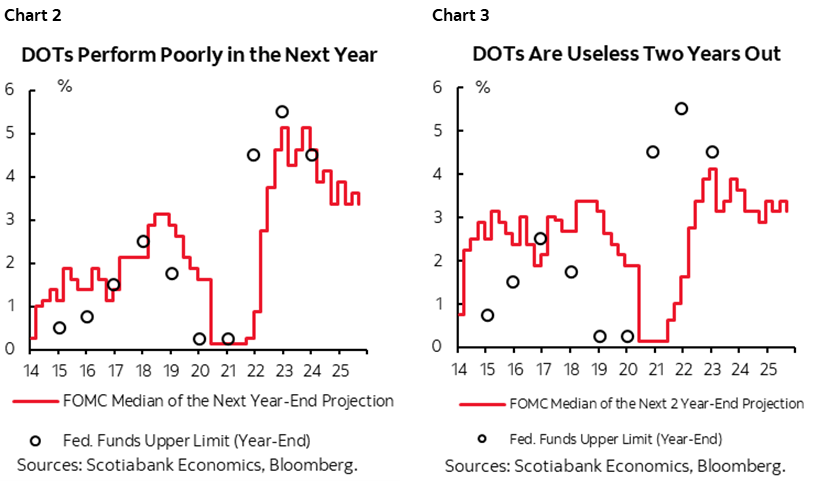

It’s finally here. The last FOMC decision of a very long year. A cut is widely expected a priced. The bias may not be any different than the one that was embedded way back in the September dot plot. That dot plot conveyed a view that only one more cut would be delivered in 2026 and then one more in 2027. The views were scattered then as they are now (chart 1). Whatever they show in the dots recall a) they do nothing to inform meeting timing versus year-end points, and b) they tend to perform poorly (charts 2, 3).

The statement will appear here at 2pmET. The fresh Summary of Economic Projections including an updated ‘dot plot’ will be here, also at 2pmET. Both links will only work at 2pmET.

Chair Powell’s press conference will be held at 2:30pmET for around 45 minutes or so. It can be watched here or at newswire services like Bloomberg (live <go>). Always have a back up feed given common tech problems.

I’m treating this meeting as a mere placeholder before we get a tonne of information that will do much more to inform the bias than anything they say and do today. Views on where rates are heading into 2026—especially the early part of the year—are total guesswork at this point. By early January we’ll get three rounds of nonfarm payrolls and a tonne of inflation data. Until then, the Fed, markets and economists are forecasting in the dark.

So let’s deal more with the immediate decision at hand. Why cut?

- insurance. There is a seven-week gap between now and the next decision on January 28th. There is a lot of information between now and then including catch-up to three rounds of nonfarm payroll reports, multiple inflation reports, year-end potential funding pressures and so on. The insurance cost to cutting now is low but the cost to not cutting into potentially bad developments that could rock markets could be quite high.

- it’s priced, so not cutting would spark potentially severe market turmoil.

- the vote-weighted Committee has done nothing to clearly lean against market pricing. The quorum of power hitters has either been silent since the October decision (Chair Powell), or signalled support for a cut including NY Fed’s Williams and several Governors. Dissents are assured, but they won’t carry the day.

- Powell tends to avoid game day policy surprises on the actual decision. His communications would be fully derailed in the final four meetings of his leadership if he started to do otherwise.

As for the statement, I expect little by way of changes. The opening paragraph is likely to repeat emphasis upon “available indicators”—since so many are not available—that point to moderate growth, slower job gains, a higher unemployment rate and higher inflation over the course of the year that remains “somewhat elevated.” Expectations and other policy goals will lie intact.

The bulk of the emphasis will be upon the SEP but perhaps most importantly Chair Powell’s press conference. Powell is likely to sound noncommittal toward the next meeting. It would be foolish to do otherwise given the massive amount of data, time and developments that lie between now and then.

BANK OF CANADA—GUARDED OPTIMISM

The statement will appear at 9:45amET here. Governor Macklem’s opening remarks will also appear at 9:45amET here.

The press conference will be held at 10:30amET. You can watch it at CPAC.ca with translations in English and French, at the BoC’s website here, at media services like Bloomberg (live <go>) and at select local tv channels

Nobody expects the policy rate to change today. No change is priced until markets begin to seriously toy with a hike by summer into Fall. Bets pick up around June through October and pricing is veering toward almost 50bps of hikes by October.

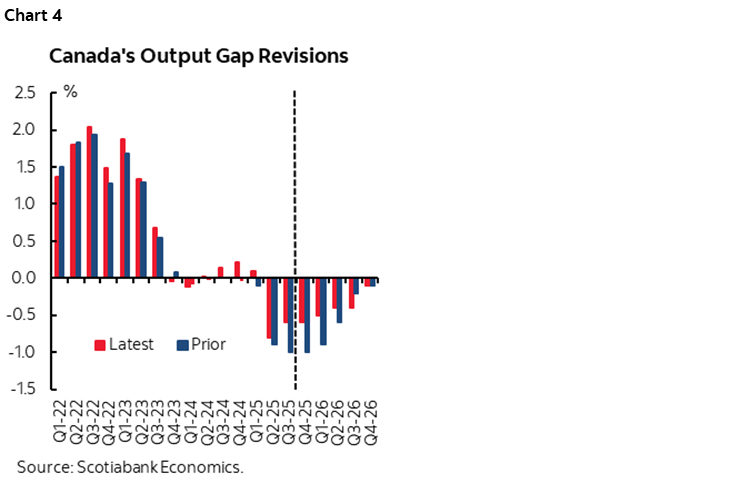

We’ve been calling 2026H2 hikes since September. In fairness, however, much of the move has been in a very short period of time concentrated around the jobs report last Friday. Large GDP revisions since 2022 that slashed estimates of slack could have motivated the market to have this view, but it took the third strong employment gain in a row to spark the move. A great deal of uncertainty lies ahead into 2026 which cuts in both directions to our expectations.

Expect a shorter statement than the last one which was accompanied by an MPR. Expect the second last paragraph to repeat reference to how they view “the current policy rate at about the right level to keep inflation close to 2%.” Expect references to a surprisingly strong trend for job gains and possibly to reduced economic slack (chart 4).

The latter may be statement-codified or referenced in the press conference. A hawkish signal would be a sign the BoC views upside risk to its prior inflation projection in the October MPR. They may choose to hold off on any such perspective until the next chance to launch a wholesale review of data, developments and fresh forecasts at the end of January.

A POSSIBLE SCOTUS DECISION?

Also, some believe that the SCOTUS IEEPA tariff ruling could come as early as today which is the last argument day of the session. If so, then Trump is sure to react and possibly fire off a bunch of social media posts about plan 'B'. That could make this an extra lively market session but it's highly uncertain when SCOTUS will rule.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.