ON DECK FOR MONDAY, DECEMBER 1

KEY POINTS:

- Five catalysts are behind a risk-off start to December

- BoJ’s Ueda may have teed up a December hike

- Black Friday sales volumes appeared to be soft

- Cybercurrencies are getting rocked again

- China’s composite PMI signals first contraction since late 2022

- US, Canada to refresh manufacturing PMIs likely to stay in contraction

- Chile’s economy surged

- Global Week Ahead—Newly Invigorated (reminder here)

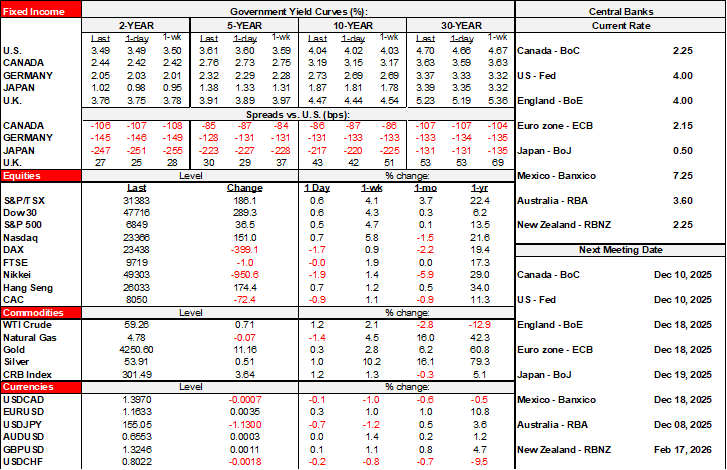

There are four catalysts to a negative start to December in terms of risk appetite: the Bank of Japan’s guidance, evidence of a softening Chinese economy, Black Friday sales results, and falling cybercurrency prices. See below for highlights of each driver. The US (ISM) and Canada will release manufacturing PMIs this morning.

The result is that the dollar is mixed but mostly a touch softer against the majors especially the yen. Sovereign bond yields are broadly but gently higher by low single-digit movements across most major global benchmarks as JGB carry effects from BoJ guidance sweep through markets. Equities are broadly lower with US futures down about ¾%, TSX futures down ¼% just before banks start releasing tomorrow, and European benchmarks ranging from flat (FTSE) to down (DAX -1½%). Japanese equities didn’t like the hike guidance with the Nikkei 225 down by nearly 2%.

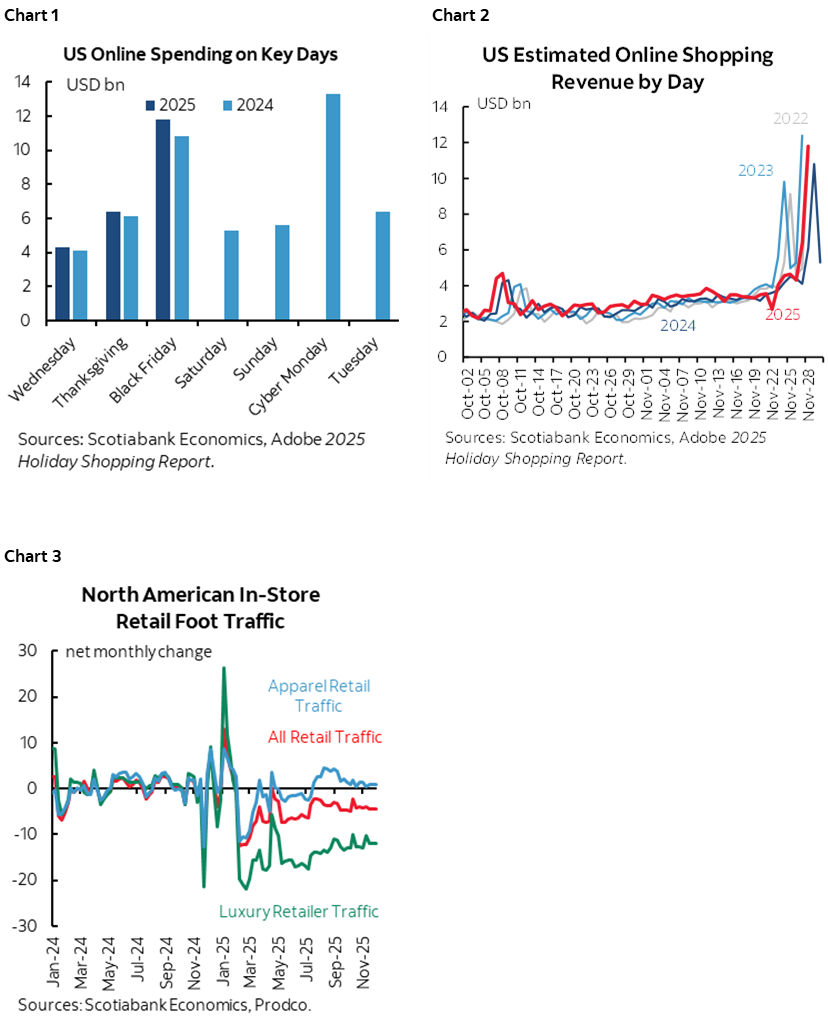

Black Friday Sales Volumes Appear to be Soft

Black Friday sales results were marked by two observations. One is that sales volumes were soft after taking account of higher prices. Two is that consumers avoided bricks-and-mortar retail in favour of online shopping. The various trackers offered mixed assessments. Given the focus upon online spending, today’s CyberMonday results may matter more. See charts 1–3 for some depictions along with the following assessments.

- Salesforce: Online spending was up 6% y/y globally and 3% y/y in the US. They say that prices were up 7% y/y with volumes down 1%. Here’s what they had to say:

- “Black Friday delivered an important signal for the U.S. economy. On the surface, sales were strong, hitting $18 billion, a 3% jump year-over-year. But with the average selling price for goods climbing 7%, U.S. shoppers continued to feel the bite of inflation.”

- Mastercard SpendingPulse: The value of sales ex-autos +4.1% y/y which probably implies weak volumes after taking account of higher prices. If that maps onto the Census Bureau’s retail sales report then it implies a slowdown since nominal retail sales ex-autos in September were up by 5.2% y/y. Almost all of the growth was in online sales.

- Adobe Analytics: E-commerce sales were up 9.1% y/y.

- RetailNext: In-store traffic fell 3.6% y/y.

- Pass-by: This company says retail store foot traffic was up by 1.2% y/y.

Bank of Japan’s Ueda Possibly Teed up a December Hike

The yen vaulted forward and the JGBs curve bear steepened with the two-year yield up 2bps and the long end up by 4–6bps. The catalyst was guidance from Bank of Japan Governor Ueda who intimated that a hike could be delivered at the December 19th meeting, earlier than some expectations for a hike the following month.

Ueda said the BoJ “will consider the pros and cons of raising the policy interest rate and make decisions as appropriate,” in reference to data dependency.

Pricing for the December meeting edged up by about 6bps from Friday to an over 80% chance of a hike.

Cybercurrency Prices Are Down Again

Several key cybercurrency prices are lower this morning. Bitcoin is off by over 5%. Ethereum is down by nearly 7%. XRP is more than 7% lower and Binance is down about 6%. Tether is flat.

Bitcoin—the largest by far—is down 31% from the peak in early October. The declining interest in cybercurrencies is not new but S&P’s warning about Tether’s dollar peg on November 26th is adding to negative sentiment. The warning brings back memories in the cybercurrency space of stablecoin Terra’s collapse in May 2022 when they lost their dollar peg and that hit everyone. Bitcoin, for example, fell by over half from early April to June 2022 by the time the dust settled.

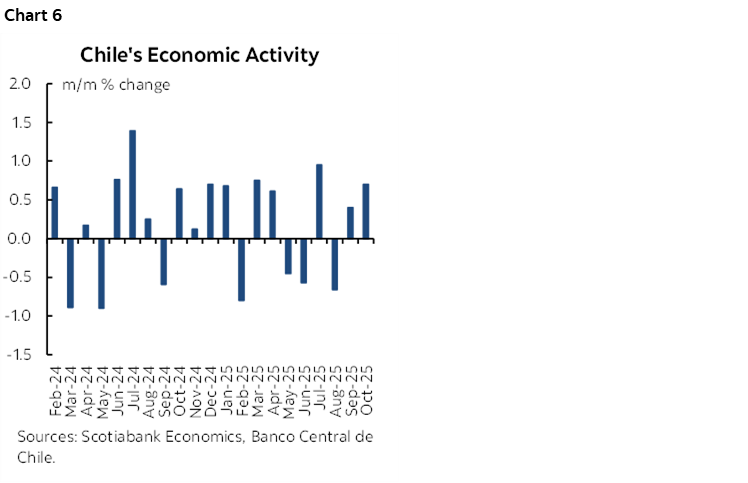

China’s Composite PMI Contracts for First Time Since Late 2022

China’s state purchasing managers indices signalled softness in China’s economy during November. The Saturday night (ET) release when no one was watching showed the composite slipped three-tenths to 49.7. While that’s a small move for soft data, it’s symbolic in that it’s the first sub-50 and hence contractionary reading since late 2022.

The manufacturing PMI was up two-tenths to 49.2 but the non-manufacturing PMI fell six-tenths to 49.5 and drove the composite weakness. Chart 4.

The private sector version of the manufacturing PMI fell by seven-tenths to 49.9. It is more heavily weighted toward smaller producers than the state PMIs that are more weighted to SOEs. The private composite PMI will be released tomorrow night. Chart 5.

US ISM-manufacturing Probably Remained Weak

US ISM-manufacturing for November is expected to remain in contraction with sharply rising prices and weak new orders and employment (10amET).

Light Data Due out of Canada

The S&P manufacturing PMI for November is due out this morning (9:30amET). It was already slightly in contraction ever since January but a poor indicator of the volatility in actual manufacturing output during the fits and starts of the tariff war being pursued by the US.

Chile’s Economy Beat Expectations

Chile’s economic activity index—a GDP proxy—surged by 0.7% m/m in October (0.4% consensus) with a minor downward revision to 0.4% growth in September (from 0.5%). Chart 6.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.