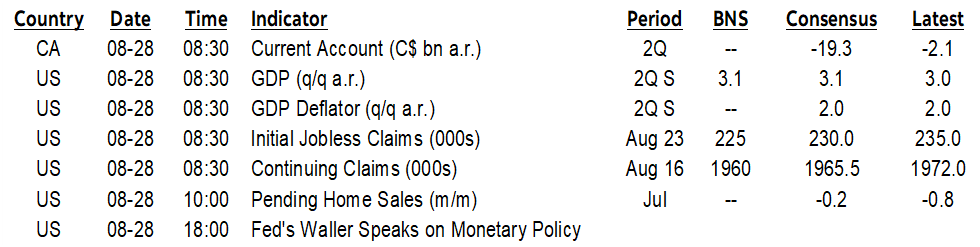

ON DECK FOR THURSDAY, AUGUST 28

KEY POINTS:

- USD softening into US data

- Canada’s bank earnings season humbled analysts

- US GDP, core PCE may be revised, claims and pending home sales on tap

- Why you should just ignore Canadian payrolls whatever the number

- A pair of Asian central banks sounded more cautious on the rate bias

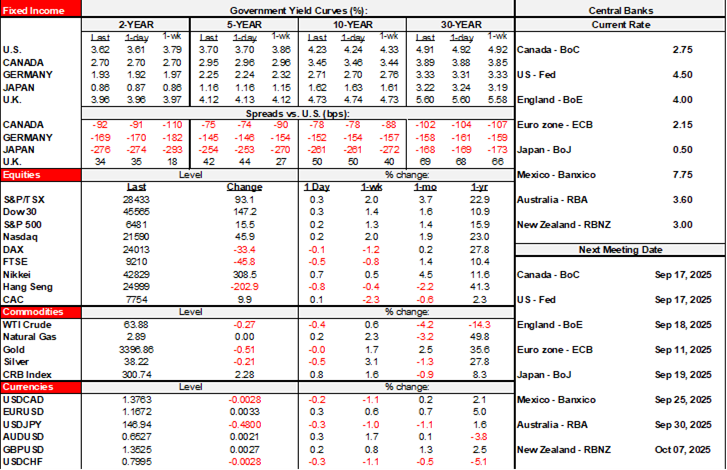

Markets are largely shaking off any broader impact of Nvidia’s results that disappointed in terms of the guidance. N.A. equity futures are little changed and European cash markets are mixed. There is very little change in sovereign bond yields and slight softening of the USD. Modest US data risk lies ahead this morning. The ‘big six’ Canadian bank earnings season concluded with another pair of beats and ignore Canadian payrolls when they arrive this morning.

MORE GUARDED FORWARD GUIDANCE FROM ASIAN CENTRAL BANKS

Asian central banks met expectations overnight. Bangko Sentral ng Pilipinas cut by 25bps as universally expected. The policy rate was described as at a ‘goldilocks’ level and a “sweet, sweet spot for both inflation and output” according to Governor Remolona with a less dovish stance than previously while not shutting the door on additional data dependent easing.

The Bank of Korea held at 2.5% as expected with only a slim chance at a cut but mixed guidance had markets emphasizing the Governor’s caution on additional easing. The won is outperforming all other major crosses. Five out of six board members said they were open to further easing by year-end but only one voted to do so this time. The central bank is pausing because of uncertainty around household debt risks and hence stability concerns, plus the impact of US tariffs. Governor Rhee sounded a little more hawkish, however, by stating that “an additional rapid rate cut could trigger stronger side effects, such as higher housing prices and greater household debt, outweighing the positive impact on growth.”

CANADIAN BANKS HUMBLED THE ANALYSTS

Canadian bank earnings continue to beat with five out of six banks beating expectations with only National Bank slightly missing this time (chart 1). CIBC beat with adjusted Q3 EPS of C$2.16 ($2.00 consensus) and announced intentions to buyback up to 20 million shares. TD Bank also beat with EPS of C$2.20 (consensus $2.05).

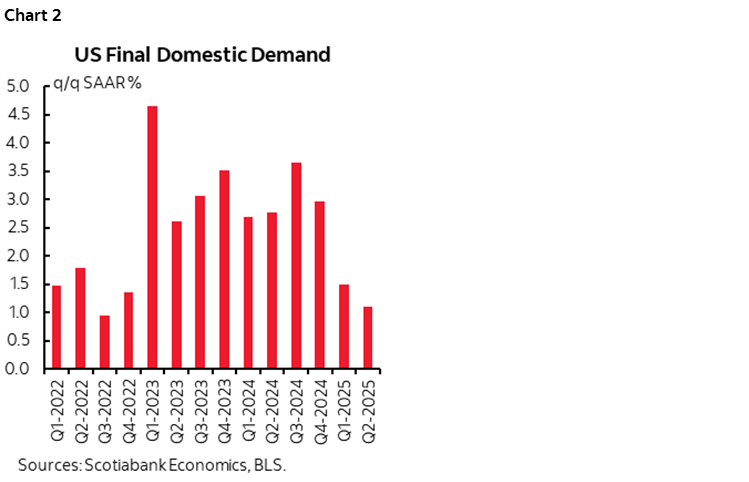

US GDP, CORE PCE REVISIONS ON TAP

US Q2 GDP might be revised up (8:30amET) on revisions since the first estimate on July 30th to consumption, industrial output, possibly construction spending given revisions to housing starts etc. Q2 GDP growth of 3% masked a softer underlying domestic economy as consumption added only 1% to the 3% growth rate, while a drop in imports added 5.2 ppts to GDP growth. Growth of final domestic demand—which adds consumption plus investment plus government spending and is a key gauge of the domestic economy—has been on a softening trajectory (chart 2). The next and hence third revision on September 25th is often where I often see more uncertainty as the quarterly services spending figures get incorporated. Also possible is a minor upward revision to core PCE inflation in Q2.

The US also refreshes weekly initial jobless claims (8:30amET). Key is whether a mild rise the prior week may have legs to it. Pending home sales for July arrive at 10amET.

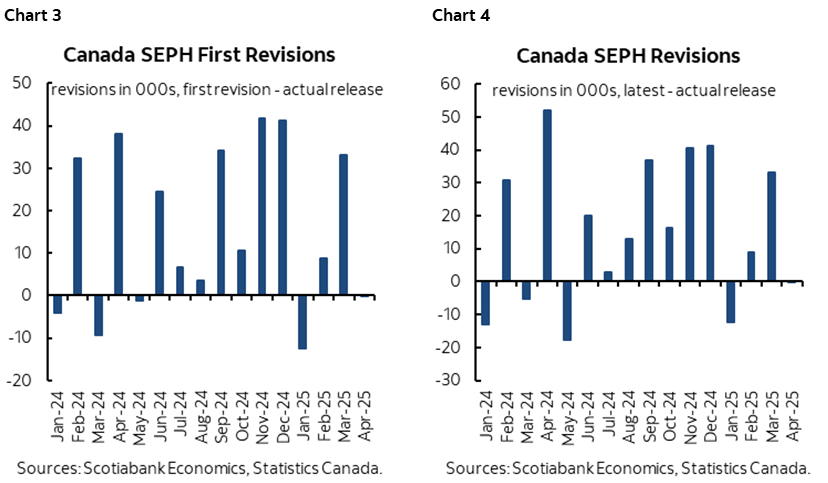

IGNORE CANADIAN PAYROLLS

Canada updates payrolls for….wait for it….June (8:30amET)! Whippee. The SEPH report is inexcusably lagging (we get LFS for August next Friday), is only focused on payrolls whereas LFS also includes off-payroll workers, and SEPH is subject to massive monthly revisions that make it unreliable. Chart 3 shows revisions to payroll changes on the first pass at them one month later, and chart 4 shows cumulative revisions to initially reported changes in payrolls using fully revised data as it currently stands. Overall, the payrolls report isn’t terribly useful.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.