ON DECK FOR WEDNESDAY, AUGUST 27

KEY POINTS:

- US markets await key earnings

- How the MAGAfication of the Fed could hit the district banks

- BoC’s Macklem set low expectations for the coming mandate review

- Canadian GDP got a slight boost

- Australian CPI surprises higher

- Canadian bank earnings season continues

US Ts are slightly underperforming European yields and the dollar is stronger across the board. Equities are little changed across major global benchmarks. There is very little by way of fresh developments to consider with just an Australian inflation surprise, more bank earnings in Canada, more tariffs and ongoing concern about Fed independence. Nvidia releases earnings in the after-market today.

RBA WATCHERS GOT A RUDE SHOCK

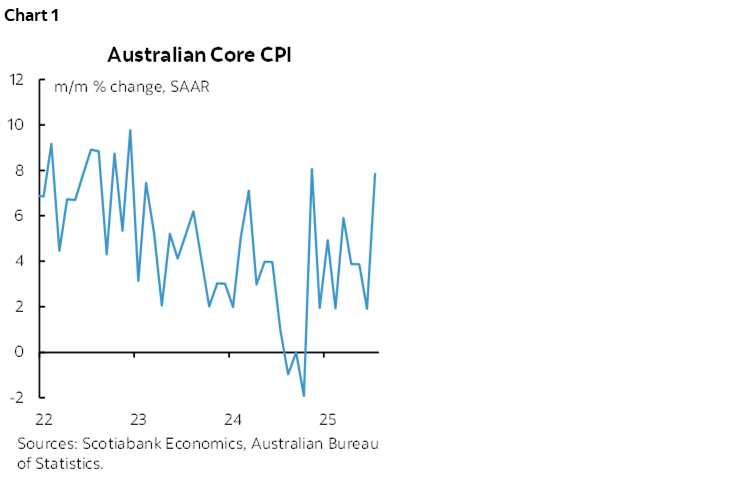

Australian CPI surprised to the high side of expectations. That drove yields a bit higher across the Australian rates curve with 2s about 3bps higher. CPI landed at 2.8% y/y (2.3% consensus, 1.9% prior) with trimmed mean CPI up six-tenths to 2.7% y/y. Traditional core CPI jumped seven-tenths to 3.2% y/y. It wasn’t just about year-ago base effects as the m/m seasonally adjusted and annualized rate of core inflation took off (chart 1). Housing, clothing and footwear, and recreation components were the main culprits.

AMERICANS TO PAY MORE FOR INDIAN CLOTHING ETC

Trump carried through on threats against India by imposing a 50% tariff rate on about half of Indian exports to the US on the theory it may dissuade India from buying Russian oil. I doubt it. Americans will pay more for items like clothing.

CANADIAN BANK EARNINGS SEASON CONTINUES

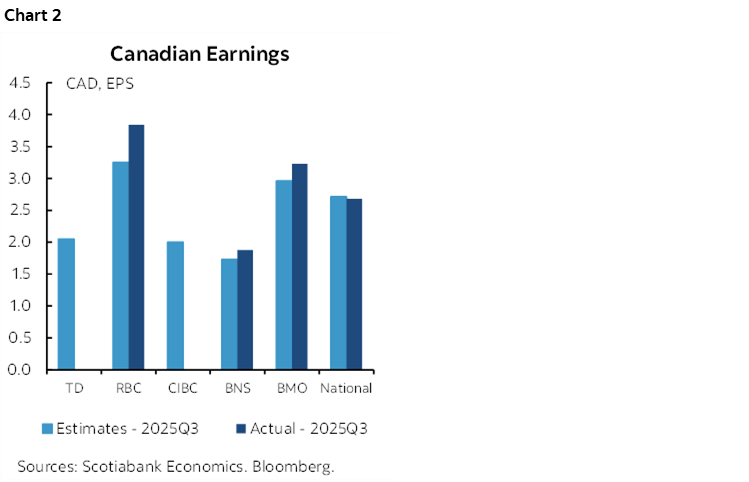

Most Canadian bank earnings are crushing it this season. RBC reported Q3 adjusted EPS of C$3.84 (consensus $3.25) with solid beats on both revenues and provisions for credit losses. National Bank slightly disappointed with EPS of C$2.68 (consensus $2.70) and a small miss on revenues. Both follow beats by BNS and BMO yesterday such that three out of four banks are beating expectations ahead of two more tomorrow (chart 2).

HOW THE MAGAFICATION OF THE FED COULD HIT THE DISTRICT BANKS

Former Fed Vice Chair and Treasury official Lael Brainard brought a fear about Fed independence out of the shadows of blogs and whispered murmurs into the mainstream yesterday. She did so by flagging the risks surrounding how the Trump administration could launch an all-out assault on the regional Fed Presidents and not just the Board of Governors.

How so? This theory has been floating around for months but was never really treated seriously in mainstream commentary. The issue is that all 12 regional Fed Presidents are up for renewal at the end of February in years ending with a 1 or a 6—ergo 2026 this time. Normally it’s largely a rubber stamp affair that doesn’t get much notice. This time could be different given the MAGA politics.

Each district bank has 9 board members. Of the 9, three are appointed by the Fed's Board of Governors, with the remaining six drawn from the community and member banks in the district and appointed by the member banks. The Chairs of the regional district boards are picked from the 3 appointed by the Fed's BoG. Therefore, the BoG can have material indirect influence upon the choice of President of the regional district bank. First stack the BoG with Trump’s chosen ones, then perhaps reshape the district boards with new appointments while perhaps applying pressure on the member banks that sit on the boards of the Fed's district banks. Then presto, pick new Presidents or apply pressure on existing ones to comply with Trump’s wishes.

Can they do that? It’s unclear and trying to do so could unleash more legal battles, not that it would stop Trump who loves having lots of lawyers hanging around. Here’s what the Brookings Institution recently wrote about the issue:

"Presidents of the 12 regional Fed banks are up for reappointment every five years. The Fed Board of Governors in Washington could replace any of them, though it hasn’t ever done so. A 2019 opinion by the Justice Department’s Office of Legal Counsel—never tested in court—said that the Fed Board of Governors can remove a Fed bank president “at will.” The law is unclear. The Federal Reserve Act, 12 U.S.C. § 248(f), says, “To suspend or remove any officer or director of any Federal reserve bank, the cause of such removal to be forthwith communicated in writing by the Board of Governors of the Federal Reserve System to the removed officer or director and to said bank.” The use of the word “cause” suggests there has to be one. A different section, 12 U.S.C. § 341 (Fifth), however, says that the board of directors of a regional Fed bank can dismiss any officer “at pleasure.”"

Obviously, any sensible Fed Governor would be highly reticent to do this. The question is therefore two-fold in nature. First, how sensible will these Governor appointments prove to be? Miran wouldn't hesitate imo and Trump mused yesterday that his spot to fill in for the departed Governor Kugler could be converted to a longer term position and his Senate confirmation hearing is to be held next week. Trump has a pattern of trying odd duck nominees who lack credibility (Judy Shelton, Miran) and could well continue the pattern.

Second, what 'cause' arguments would be cooked up by the administration and MAGA types to assault the regional presidents, perhaps forcing the Board's hand? I hope the regional Presidents are squeaky clean in terms of mortgage apps, anything else in their backgrounds, their favourite flavours of ice cream etc.

Obviously all of this isn't a base case at this point. Then again, none of this was. It's prudent to be mindful toward next steps over coming weeks and months. Such a scenario—stacking the Board and regional Presidents—imo risks a severe blow to confidence in US markets.

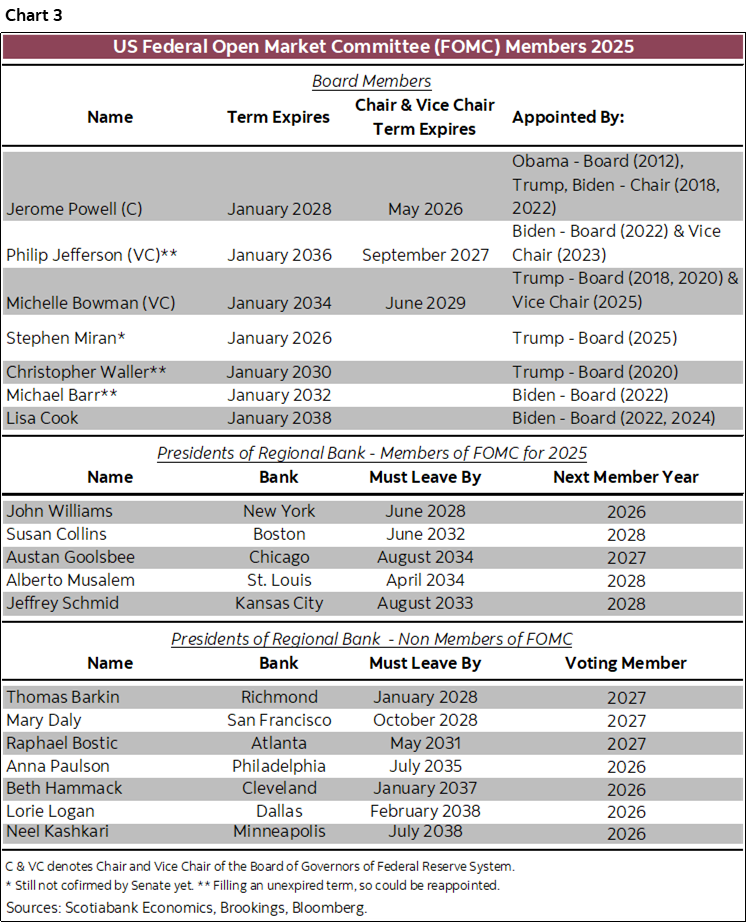

As added input, see chart 3 that is a summary table of the dates for Federal Reserve officials that doesn’t include the five year reviews of the regional Presidents but only the expirations of their terms assuming they pass each review.

WHAT WE LEARNED FROM MACKLEM’S SPEECH

BoC Governor Macklem’s speech yesterday (here) contained nothing of direct relevance to nearer-term monetary policy considerations. I think the only takeaway was to basically declare that next year’s mandate review is going to be a dud.

The speech was partly about setting low expectations for material changes in the next framework review in 2026. Unlike the fake 'horse race' they ran in the past review to see if something was better than 2% flexible targeting only to do what they’ve always done which is to say ‘nope’, this time he's explicitly saying they won't change anything material and won’t even waste anyone’s time pretending that it’s an option. Quote:

“We’ve considered whether the target should be lower or higher. We’ve also weighed alternatives to inflation targeting, including price-level targeting and nominal GDP targeting. Each time, we’ve concluded that Targeting 2% inflation is the right framework for us. The experience since the last renewal in 2021 has only reinforced this conclusion. The 2022 spike in inflation was a painful reminder of just how much Canadians don’t like high inflation. We also know that Canadians generally understand and support the 2% target. That familiarity has helped anchor inflation expectations through thick and thin, including through the pandemic crisis."

Of course, that last part is a little rich. Macklem blew it on inflation risk with all of his transitory talk and didn’t listen to warnings.

There was also added reason to think that maybe the BoC is revisiting the best ways to measure core inflation. This has been understood to be a consideration for a little while and here’s his general remark:

"Second, with more supply shocks and greater volatility in inflation, what is the best way to measure core inflation? At the Bank of Canada, we’ve used various measures of core inflation over the past few decades. And in practice we often use an even broader range of indicators to assess underlying inflation. Going forward, what’s the best approach—narrow or broad—and what are the best indicators?"

Former Governor Poloz introduced trimmed mean, weighted median and common component CPI as alternatives to traditional core CPI ex-food and energy. He overcomplicated inflation. Since then, common component has become a dirty phrase in Canadian monetary policy circles. It may well be that traditional core CPI remains best.

CANADIAN GDP GOT A SLIGHT BOOST

Canadian GDP in July got a bit of a boost yesterday morning ahead of Friday's numbers for Q2, June and July GDP.

Statcan's advance indicator for manufacturing sales in July was reported to be up by 1.8% m/m SA in nominal terms. The advance indicator for nominal wholesale trade in July was reported up 1.3%.

After adjusting the nominal readings in order to get volume estimates and pushing it through a simple equation that I run I get 0.2% m/m GDP growth in July. That's mainly based on housing (starts higher, ancillary housing services to be lifted by resales) and these numbers, but I would lean more to downside than upside risk to that estimate given that hours were slightly softer, retail volumes slipped after a powerful surge in June and wildfires could have exacted a minor toll.

Still, Q3 GDP is getting a bit of baked-in momentum so far based on what probably happened to the way Q2 ended and very preliminary tracking into July.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.