ON DECK FOR TUESDAY, AUGUST 26

KEY POINTS:

- Risk-off sentiment is being driven by political developments

- Trump’s firing of Governor Cook has nothing to do with mortgage law

- Trump is escalating tariff threats since Powell increased moral hazard

- CAC40 continues to underperform on French government stability concerns

- Gilts underperforming on concerns over budget imbalances

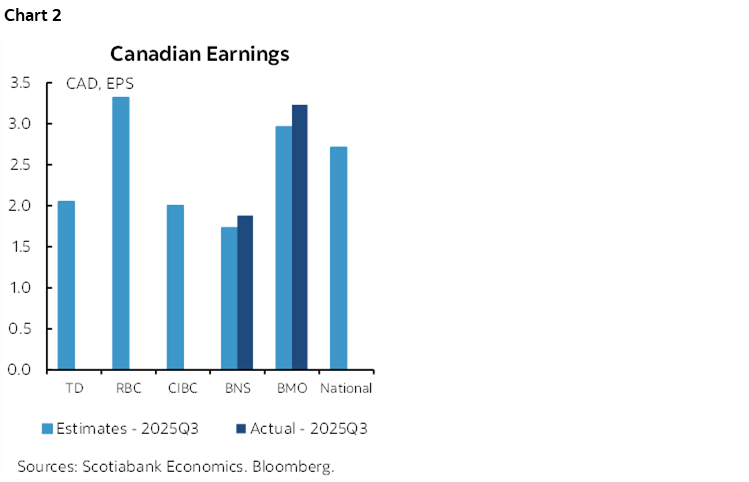

- Canada’s Q3 bank earnings season is off to a roaring start

- BoC’s Macklem to speak on flexible inflation targeting

- US data: confidence, durables, house prices, Richmond

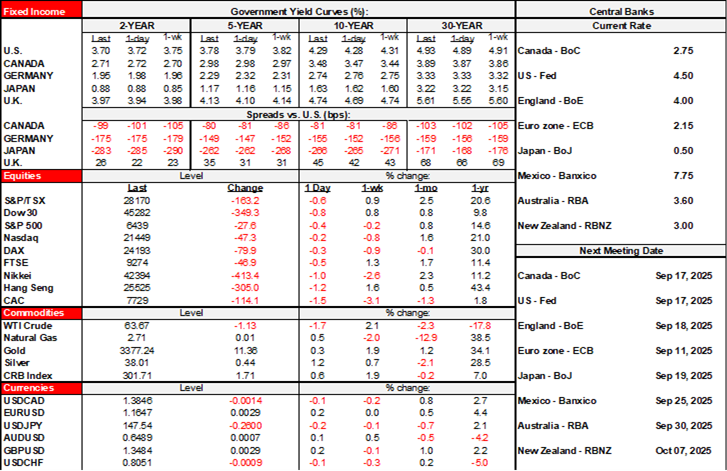

Risk off sentiment is marked by slight weakness in N.A. equity futures and slightly larger declines in European cash markets following losses across most Asian exchanges. Catalysts may include Trump’s additional tariff threats related to countries with digital service taxes last evening after escalating pharma tariff warnings and furniture tariff threats, Trump’s move to fire Fed Governor Cook, and perhaps market concerns about the French government’s viability into a confidence vote on budget measures (chart 1). The CAC40 is falling by 1½% this morning and French 10s are once again underperforming bunds. Gilts are underperforming sovereign bond rallies elsewhere as uncertainty rises over potential measures to rein in fiscal imbalances ahead of Chancellor Reeves’ autumn budget likely by late October. The dollar is depreciating against most of the majors. An otherwise light overnight session for calendar-based risk is giving way to several US releases, a speech by BoC Governor Macklem and the start of the Q3 Canadian bank earnings season.

FED UNDER ATTACK

Trump’s announced firing of Fed Governor Cook sets in motion a legal spat as both sides dig in. Next steps are unclear including whether she succeeds in filing an injunction and how legal actions subsequently unfold. One would be naïve beyond belief in thinking this is about enforcing mortgage law. The goal is for Trump to wind up stacking the Fed with 5 out of 7 Board spots. It is Democrats that are being targeted with mortgage charges with others including Adam Schiff and Letitia James. It is Bill Pulte—the homebuilder in charge of the FHFA housing finance regulator and Trump’s pitbull—who is leading the charge. Controlling the Fed and dirty, vindictive, partisan politics are the motives.

CANADA’S BANK EARNINGS SEASON OFF TO A ROARING START

The Q3 Canadian bank earnings season got off to a good start this morning against analyst expectations that seasonally unadjusted earnings would be lower than the same period a year ago. BNS beat with adjusted EPS of C$1.88 (consensus $1.73) and revenues also beat expectations. BMO also beat with adjusted EPS of C$1.88 (consensus $1.73). Very good to see as a riding tide lifts all boats and particularly in the case of my employer. So far so good with the rest on tap over the remainder of the weak (chart 2).

BoC’S MACKLEM TO RELEASE SPEECH

Macklem’s speech will be a text only affair, with no presser and no Q&A (2:45pmET). The topic is ‘flexible inflation targeting in a more shock-prone world.’ It could just be to fete Banxico on its 100th anniversary. It could harken back to when Carney was BoC Governor and Macklem was his SDG and they worked the target range more openly. There is the risk of policy related remarks, but I doubt it. Macklem tends to speak in riddles even more than most central bankers and his forward guidance isn’t terribly useful even when he isn’t afraid of publishing a forecast.

US DATA RELEASES

Several US data releases are due out this morning.

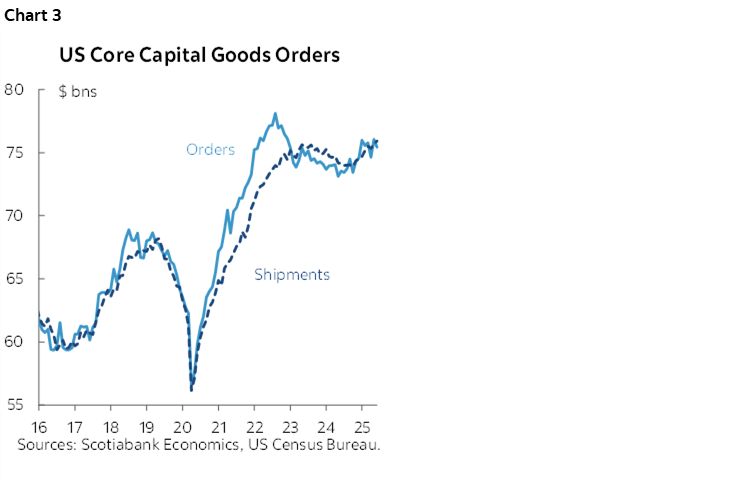

US durable goods orders probably fell in July (8:30amET), given what we know about volatile aircraft orders that have been see-sawing and that fell sharply in July. Boeing reportedly has an order backlog of 11.5 years; order all you want, but production constraints get in the way of how fast they show up in the shipments and GDP figures. Nevertheless, key will be orders ex-defence and air as a proxy for equipment spending. They have been volatile but down in three out of six months this year including a 0.8% drop in June. Smoothing through the noise shows a sideways trend this year after a spurt of equipment orders late last year into very early this year (chart 3). The pattern going forward is among the litmus tests for c-suite confidence.

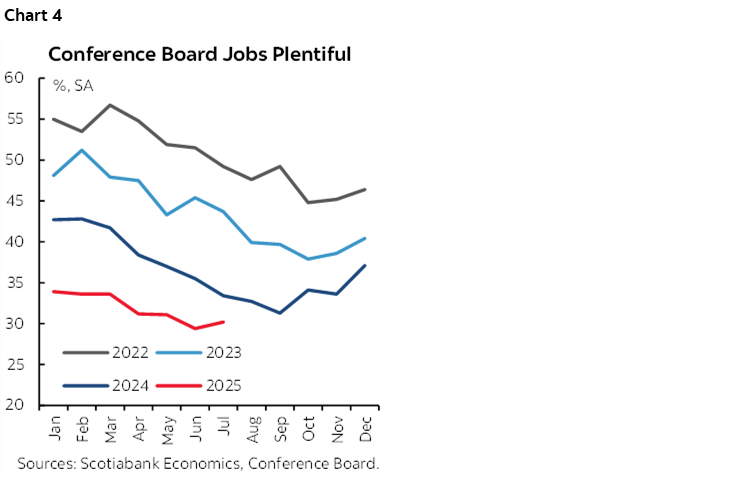

US consumer confidence is also on tap and expected to slip a touch in August’s reading (10amET). Consensus expectations rarely mean much for this reading, but it’s more labour market related than UofM sentiment and so potentially more vulnerable to the sudden softening of the job market. For pre-nonfarm job market signals, watch the ‘jobs plentiful’ gauge that has been on a downward trend since its early 2022 peak. That comes with the caveat that it has residual seasonality in recent years (chart 4). It starts high at the beginning of the year and then wanes even in SA terms in a steady pattern from 2022–25. It’s one of many examples of how seasonality got messed up by the pandemic and the aftermath.

Repeat sale home prices in June (9amET) and the Richmond Fed’s manufacturing index in August (10amET) will round it all out.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.