ON DECK FOR FRIDAY, AUGUST 22

KEY POINTS:

- Markets steady ahead of potential fireworks

- Chair Powell’s speech preview—it would be an odd time to pivot

- It’s not just about Powell

- Canadian retail sales tracking favourably?

- Japanese core inflation tumbles

Jackson Hole, Jackson Hole, Jackson Hole. That about sums up the end of the week. So raise a toast to it, with a little lemon twist of Canadian retail sales before the main event.

Into it all, I like the fact that markets have become somewhat more balanced on September pricing by knocking it down to about 17bps compared to briefly flirting with above 25bps at the peak just over a week ago. That opens up opportunity if he dovishly pivots, while containing some of the damage if he kisses a portrait of Paul Volcker on tv.

The full, formal agenda is available here and contained no material surprises. It includes the expected speech by Chair Powell this morning, and appearances by Lagarde, Bailey and Ueda on Saturday. The theme this year is ‘Demographics, Productivity and Macroeconomic Policy.” The topic definitely has the feel of being one that was chosen before the last six months felt like four years already.

Powell’s speech will be key at 10amET and should be available here. It’s usually short—last year’s was about 2300 words—and should be over in under 20 minutes or so if you are timing pricing or deals or when to grab a coffee. He will read it out in monotone fashion before an unexcitable bunch of central bankers and academics and then walk off the stage, sans Q&A, maybe with a celebratory bat flip. This one is deliberately titled “Economic Outlook and Framework Review.”

It’s possible that Powell may not even address nearer term monetary policy in favour of the medium-term outlook and the promised end-of-summer conclusions of the framework review before the communication tools are revisited later this Fall and perhaps including changes to the Summary of Economic Projections.

But I think he will find a way to opine on the nearer term monetary policy bias. He had a whole section on the “near-term outlook for policy” in last year’s speech. It would be kind of irresponsible to leave markets totally hanging now.

I expect him to resist validating a near-term cut at least for now. I would be concerned if he were to go against basically everything he has said up to now only to cave under very obvious pressure from the administration.

For one thing, he’d be somewhat silly to do so with major data releases still to come including another nonfarm payrolls print, PCE inflation, and another CPI reading.

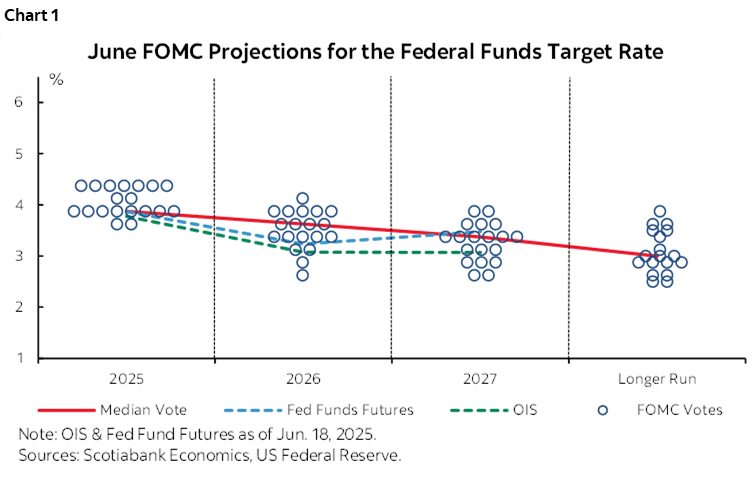

For another, the dot plot in June (chart 1) signalled two cuts this year over three meetings and only by a whisker as just one fewer dot leaned toward zippo. The tone of the FOMC minutes and remarks by Committee members since then suggest a lack of confidence in a sudden change. Powell and the Committee may prefer to take another full run at projections with more data in the September SEP and dot plot and hold off on anything until they are more fully armed with a fresh take.

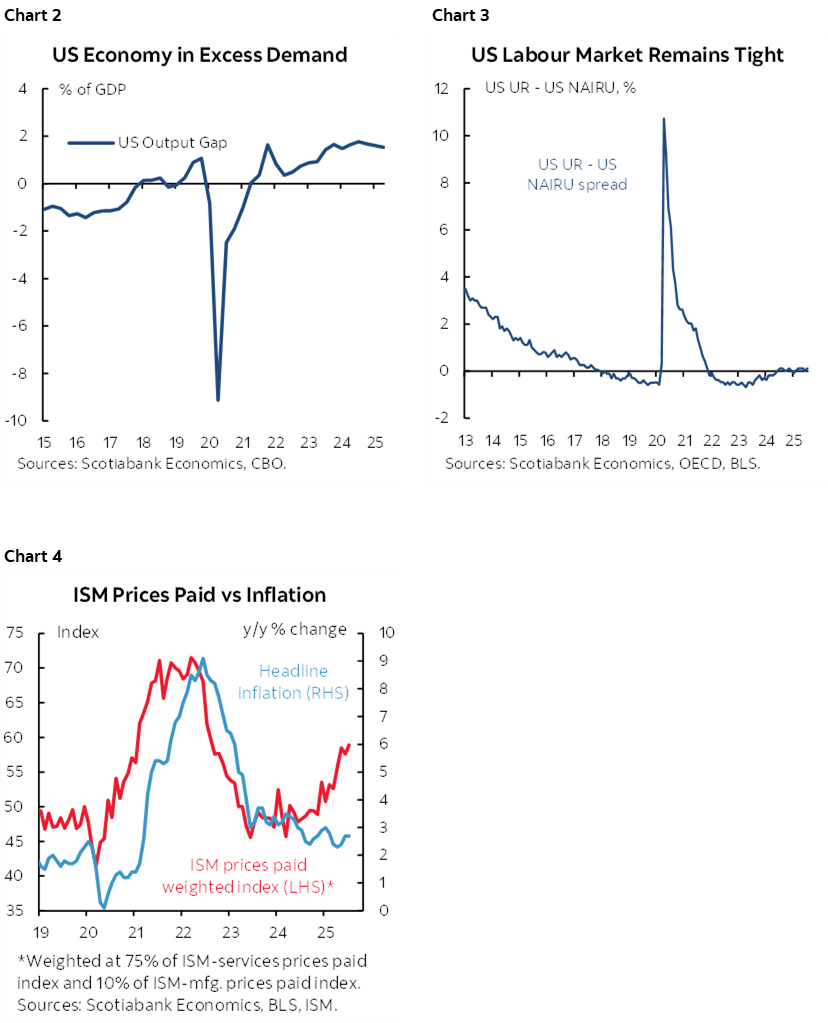

Further, the data to date and broad financial conditions don’t necessitate any rush to ease. GDP growth of 3% in Q2—albeit with softer details—and tracking 2–2.5% in Q3 and an economy that remains in excess aggregate demand (chart 2) do not cry out for easing. An unemployment rate of 4.2% is still signalling full employment or something very close to it (chart 3). Nonfarm payroll changes over recent months have only been slightly below estimates of monthly breakeven rates under tighter immigration policy. Core inflation has sent recent warning signs in core PPI and core CPI and probably next week’s core PCE. Advance price signals from ‘soft’ data sources like PMIs point toward rising price pressures over the duration of the year (chart 4). Company anecdotes pointing to pass through of tariffs have been significant. And throughout it all are very legitimate questions surrounding data quality including survey response rates that have been falling for a long time, proxy methods for estimating inflation in the face of BLS budget cuts, and questionable seasonal adjustment factors subject to a strong recency bias in their calculations. And who knows what data contortions lie ahead when the thoroughly unqualified E.J. Antoni takes over at the BLS—assuming he’s confirmed in the Senate.

None of which settles the debate over what might eventually happen. Yeah yeah, there are risks going ahead, the US economy might suddenly sputter, unemployment might spike—but how many times have you heard folks giving up prospects between the Gulf of Mexico (!) and the 49th only to be proven wrong? Powell doesn’t trust forecasts, and with considerable merit in doing so.

Key, however, is that Powell’s signalled reaction function is treating the impact of tariffs, immigration and other policies on the dual mandate as an empirical question to be settled over time. The forces cut in opposing fashion on the dual mandate by potentially raising unemployment and potentially raising inflation; which one deteriorates the most relative to 2% inflation and 4% unemployment goals will determine the appropriate course of action. Quibble with that all you want, but markets have been losing the fight against the Fed all year long.

All of which is to say that the conflicting signs in data are so far adherent to Powell’s concerns about how dual mandate goals might be at odds to one another and uncertainty toward what to do about it. If he’s been saying all along that he’s uncomfortable adjusting policy until he has more answers, then it would be an awkward time to pivot when he’s seeing the very evidence of conflicting effects that he warned us about all along—and still without answers on where the balance sits.

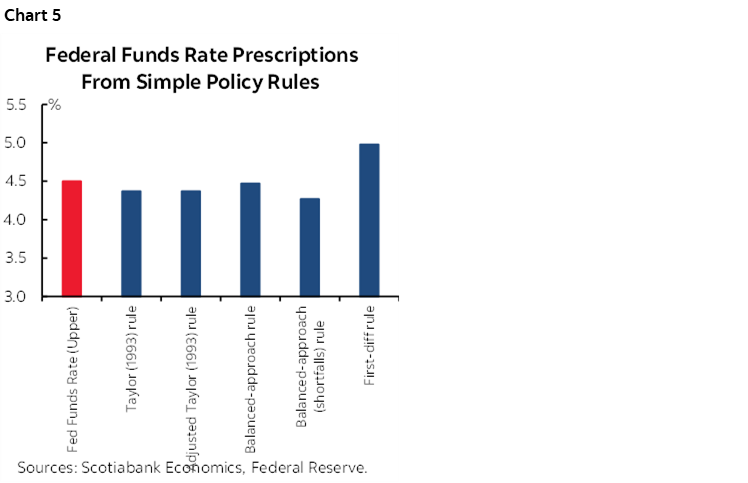

Powell has also consistently emphasized how every variation of the Taylor rule that the Fed’s economists run shows that policy is either about right or—in one scenario—supportive of tighter policy (chart 5).

Against this backdrop are added complications. Risk appetite needs no help; I view financial conditions as frothy.

Cut in September, and itchy trigger fingers hovering over those buy buttons will have their gotcha moment and the Fed could invite much further easing of financial conditions sooner than it’s prepared to court. Ergo, you’d better have high confidence in restarting cuts.

Moral hazard is an unspoken word in Fed-speak, but a sensible caution nonetheless; at issue is emboldening Trump’s protectionism as Powell leads the cavalry to his rescue. US macroeconomic policy is on awful foundations with an unsustainable fiscal path, rampant protectionism, contractionary immigration policy and with regressive consequences to the lifeblood of the American economy that is—and always will be—the middle-class consumer.

Other Stuff

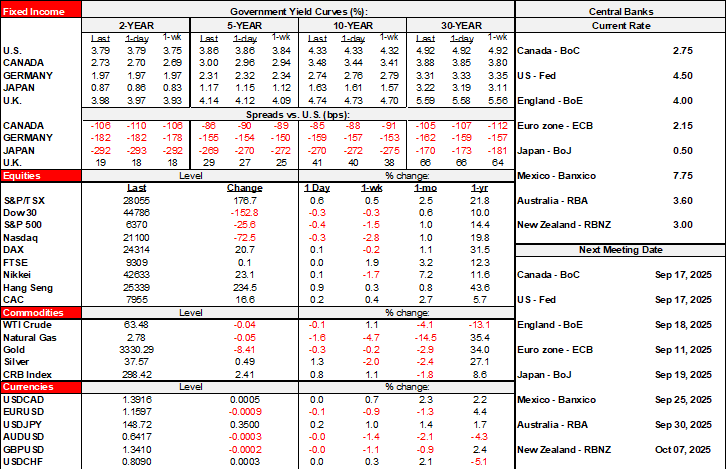

Canada updates retail sales for June and July this morning. June is expected to post about a 1½% m/m SA nominal gain based largely on Statcan’s advance guidance which can be subject to material revision. Details like volumes and prices and drivers will matter. We’ll also get the first reading for July’s nominal sales sans details.

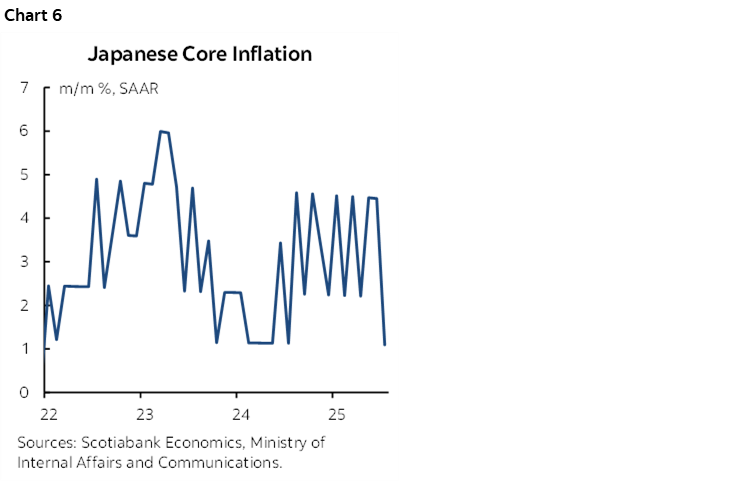

Japanese core inflation tumbled last month (chart 6). The rise of about 0.1% m/m SA nonannualized was the softest since last summer. There was no reaction in JGBs; markets had already digested similar information in the Tokyo CPI figures on July 24th for the same month.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.