ON DECK FOR THURSDAY, AUGUST 21

KEY POINTS:

- Mild risk-off sentiment on the eve of Powell’s speech…

- ...and with global PMIs signalling resilience and less pressure to ease monetary policy

- Be careful with tariff-related interpretations of the PMIs

- NOK outperforms as GDP growth doubles expectations

- US PMIs, home sales on tap

- Of course the attacks on Fed Governor Cook are partisan! And here’s what’s at stake

It’s T-1 and counting until Powell. Markets are in slight risk-off mode with equities broadly but gently lower. Sovereign bond yields are broadly but gently higher. Currencies are mixed.

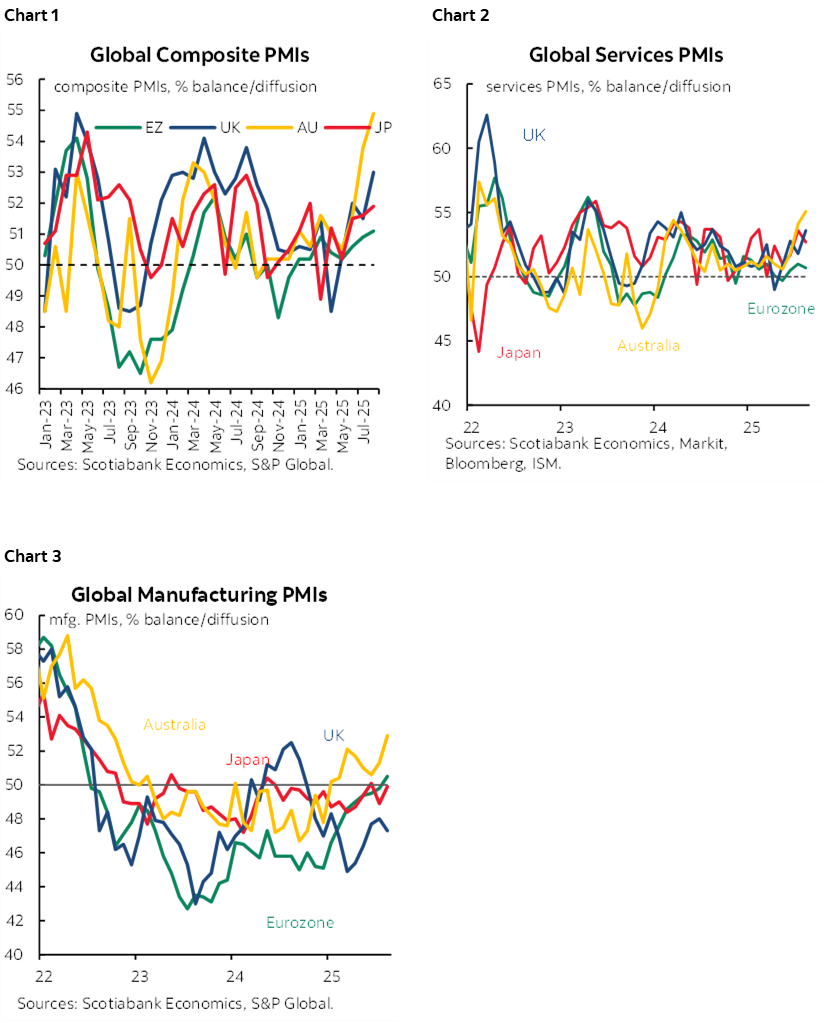

Uneven Evidence Across Global PMIs

Perhaps what markets don’t like is evidence of economic resilience amid some price pressures, although the evidence across global PMIs was uneven in both regards.

Across the PMIs evidence, services accelerated in the UK, Australia and India, but decelerated in the Eurozone and Japan. Manufacturing grew faster in the Eurozone, Japan, India, and Australia, but slowed in the UK. Output price inflation picked up in India, the Eurozone and UK services but not manufacturing, and decelerated in Japan and Australia. Charts 1–3 shows the results.

As a broad point, be careful with some of the headlines seeking to spin a tale about what this means in terms of tariff effects. One reason for that is because services volatility played a large role and so it wasn’t just about manufacturing across these countries. Another reason is that the first and starts with which tariffs have been threatened, delayed, and ultimately applied makes for caution toward reaching conclusions. Bursts of tariff front-running in ordering activity to exploit windows of opportunity to stock inventories before most tariffs became more binding may be created a false sense of comfort with the overwhelming bulk of the tariff effect still ahead.

Here are the results by country:

- Japan’s composite PMI inched higher to 51.9 from 51.6 although that gain probably isn’t statistically significant. Services decelerated (52.7, 53.6) as manufacturing moved up a point to almost the 50 line that demarcates balance. Input price inflation accelerated but output price inflation decelerated.

- India’s composite PMI jumped higher by 4.1 points to 65.2 with a 5.1 point rise in the services PMI leading the way to a robust 65.6 as manufacturing edged slightly higher to a solid 59.8 (59.1 prior). Output prices climbed “much faster” than input costs.

- Australia’s composite PMI climbed 1.1 points to 54.9 with a one-point rise in services (55.1) combining with a 1.6 point jump in manufacturing (52.9, 51.3 prior). Both input and output price inflation eased.

- The Eurozone’s composite PMI was little changed at 51.1 (50.9 prior) as a seven-tenths rise in manufacturing slightly into expansion territory (50.5) was held back by a slight deceleration in services (50.7, 51.0 prior). Both input (fastest in five months) and output (fastest in four months) price inflation accelerated.

- France’s composite PMI remained slightly in contraction while Germany’s composite PMI remained slightly in expansion territory.

- The UK composite PMI jumped higher by 1.5 points to signal quicker expansion (53.0) entirely due to quicker growth in services (53.6, 51.8 prior) as manufacturing slowed (47.3, 48 prior). Input price inflation was the highest since May. Output price inflation accelerated in services but decelerated in manufacturing.

NOK Outperforms on GDP Beat

Non-PMI developments were light. NOK is outperforming all other majors this morning after Q2 GDP growth doubled expectations, coming in at 0.6% q/q SA nonannualized. Growth was led by investment and net trade with small contributions from consumption and government.

US Data on Tap

Light data is on tap into the N.A. session with the focus on the US S&P PMIs (9:45amET) and existing home sales during July (10amET) plus initial jobless claims (8:30amET).

Ongoing Fed Drama

The controversy surrounding Fed Governor Cook continues. She said last night that she wouldn’t be “bullied” into resigning. Good for her. That is indeed what she’s dealing with. In fairness, however, she also promised to show her version of the facts, so let’s see them as this may not simply go away. Meanwhile, Bill Pulte—the homebuilder turned head of the FHFA (a home financing regulator) and one of Trump’s pitbulls—claims his singling out of Cook among reportedly tens of thousands—maybe more—who reportedly do similar things with their mortgage applications isn’t partisan. If that’s the case, then tell the Attorney General to launch a broad investigation and pursue everyone who does this and without bias because, as he says, Pulte is merely interested in enforcing the laws of the land.

The bigger stakes here are represented by the potential for Trump to stack the Fed’s Board with five partisan Governors including Waller, Bowman and Miran if he passes the Senate, Powell’s successor, and potentially Cook if this controversy has legs. The bigger stakes from a market standpoint are represented by concerns around Fed independence.

A very high starting point for valuations, efforts toward easing capital constraints including GSIBs eSLR and SLR relief that brings more money into Treasuries that permeate most other asset classes, and efforts to force the Fed to become much more dovish could backfire in the bond market for two reasons. One is if such a policy stance is viewed as politicized and not driven by the merits of such actions. Two is because those of us who’ve been around a while have seen this movie before. Risk managers, be prepared to widen those longer-run brackets around all projections.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.