ON DECK FOR TUESDAY, AUGUST 19

KEY POINTS:

- Markets treading water until Jackson Hole

- Canadian CPI may spice up near-term market volatility…

- …but take it in stride with a lot more evidence ahead of September’s BoC decision

- The costly macro context to ongoing labour strife in Canada

Canadian CPI will be the main event today after a light overnight session with no truly fresh developments. More broadly speaking, all we’re largely doing is treading water until Chair Powell’s speech on Friday morning.

I’m sure we’ll get some market noise in the aftermath, but nothing about September’s BoC decision hangs in the balance on just this one reading. It is just one of two CPI readings before the next BoC decision on September 17th with the next one arriving the day before. A lot more data lies ahead including GDP for Q2, June, and July that we get a week from Friday, plus another jobs report, plus potential further developments in trade and fiscal policies among other factors.

My estimate is for a 0.5% m/m seasonally unadjusted rise in headline CPI based on limited observables such as gas prices, seasonal influences, and some housing and food price tracking. That could translate into about a 0.3% m/m seasonally adjusted rise based on the fact that SA factors for the month of July in recent years have been among the lowest on record due to the recency bias in how they are calculated. The median estimate is 0.3% m/m NSA with several in the 0.4% camp. As always, the consensus isn’t known when we submit our numbers and frankly should never be a factor in anyone’s own homework. There is high uncertainty into the reading not only due to normal uncertainty given limited observability of price components, but also because of potential tariff effects.

But headline is not what matters. It’s too distorted in y/y terms by the ongoing effects of the elimination of the consumer portion of the carbon tax in early April and it’s too volatile in m/m terms given swings in food and energy prices.

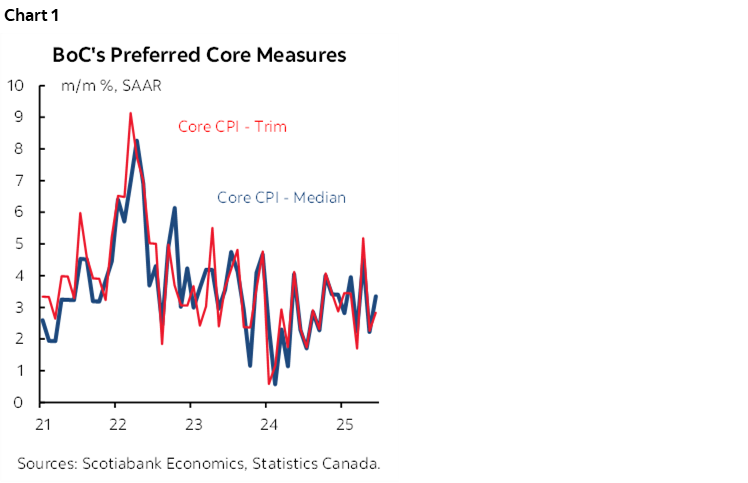

What will matter, however, is what will happen to the average of the two preferred core inflation readings used by the BoC that have remained hot and are impossible to estimate in advance in m/m SAAR terms. Over five dozen prices go into their calculations and what falls out of trimmed mean after lopping off the top and bottom 20% of prices, or exactly where the weighted median price sits, are both highly sensitive to the exact distribution of those prices. Forecasting y/y trimmed mean and weighted median CPI is largely just a matter of rotating out the first of twelve months and rotating in a guess at the latest month since they are not spot y/y calcs, but rather weighted m/m compounded annually readings. If you want a fresh measure of price pressures at the margin, then that’s why I always argue you should use m/m SAAR and smooth it a bit.

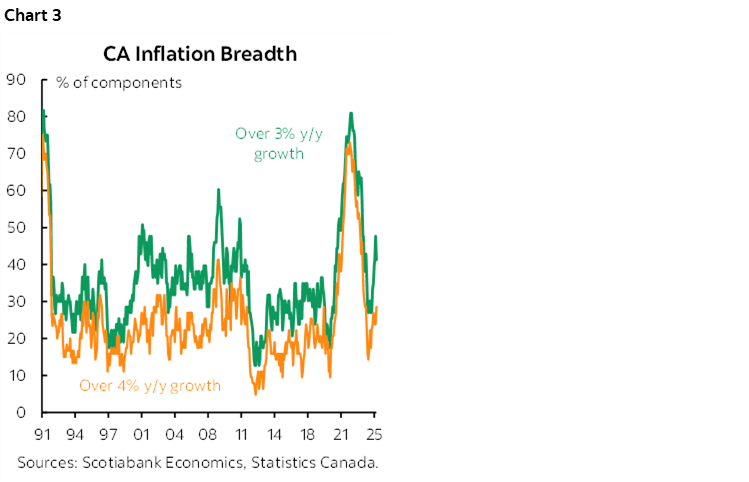

Yet the core readings have averaged 3.4% m/m SAAR over the past three months. Chart 1 shows the m/m SAAR pattern and chart 2 shows the numbers that have been elevated for a long time. Service price inflation has been trending warmly, the breadth of price pressures has been rising (chart 3), and key may be any early tariff effects on some goods prices both directly—through Canada’s limited retaliatory measures— and indirectly—through supply chain effects. The core measures exclude tariffs, but not the possible pass-through incidence effects.

Other than that, we’ll only get US housing starts and a pair of events featuring dovish Fed Governor Bowman—ever thankful to Trump for her posting and perhaps with an eye on Powell’s job.

THE MACRO CONTEXT TO CANADIAN STRIKES

Labour strife is alive and kicking in Canada. We see that in the Air Canada strike that may have come to an end with tentative acceptance of a fresh offer by the union at a presumably higher gain than the 38% lift over four years including 25% in the first year that was rejected earlier. The agreement still has to go to a vote.

Good for them. Workers have been challenged by cost of living pressures over the years. Who can fault folks for seeking and getting higher pay if someone is willing to give it especially if creeping hours worked are being unpaid. I suspect that on the latter point the labour minister may have opened a whole can of worms by announcing a probe into unpaid hours; the line-up out the door is likely to be rather long.

But there is a broader macro context that isn’t getting emphasized in the coverage. Canada is going through the ongoing effects of the pandemic in resetting contract wages higher and causing 1970s style workplace disruptions. Like everything in economics, there is a benefit and a cost and both have to be explored given a variety of interests and angles on the issues at hand.

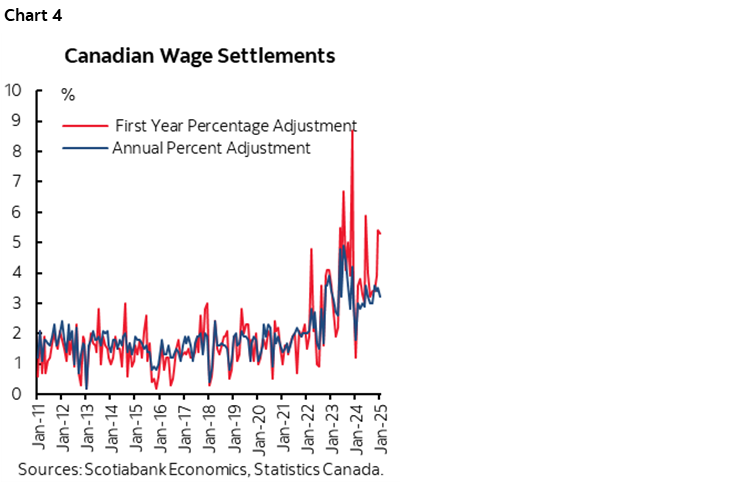

Enter chart 4. It shows wage settlements being achieved in collective bargaining agreements in both the first year and on average over the typical 3–4 year contract period. The data is lagging because the government folks who update this site have once again stopped updating it and have not responded to two requests to do so. Statcan needs to take over this source as it’s too untimely and unreliable but hopefully not politicized. Still, the point is that wage settlements are continuing to push through catch-up pay gains in the wake of the pandemic’s disruptive effects. This is important in Canada where about one-in-three workers are unionized versus about 10% in the US.

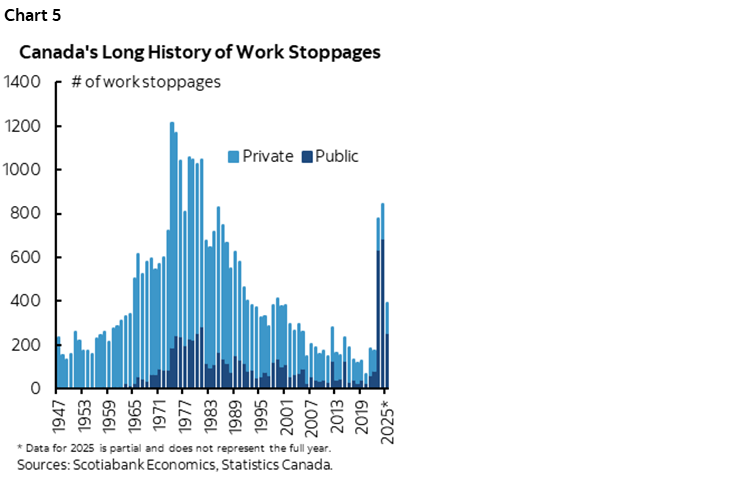

The effects are also causing 1970s-style work stoppages (chart 5). This data comes from the same department that hasn’t updated the wage figures since January but makes the point about disruptions to employers including ones that are directly impacted and those that are indirectly affected when what are basically essential services go on strike.

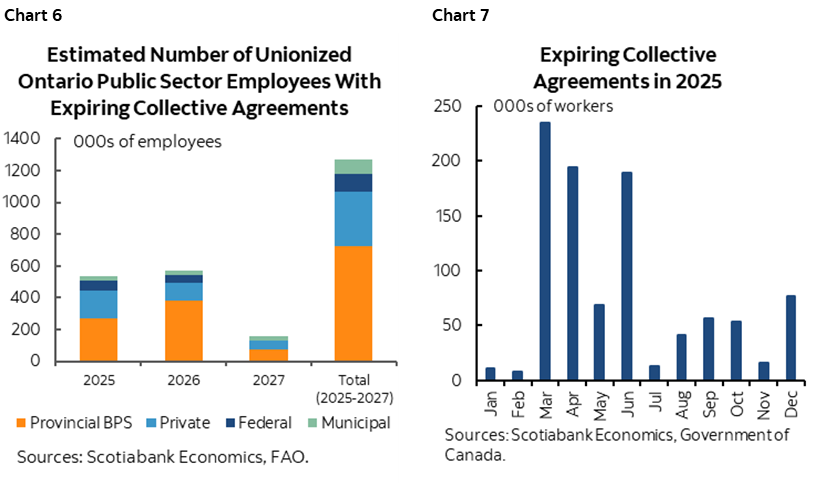

And it’s not over yet. In just Ontario alone, about 1¼ million workers are under expiring contracts over 2025–27 (chart 6). Many—not all—are in the public sector with another example being support workers at Ontario’s struggling community colleges. Chart 7 shows the number of affected workers under expiring agreements by month nationwide.

What happens in the collective bargaining sector can carry spillover effects in other parts of the labour market by raising everyone’s wage pressures. Again, workers rejoice, but here’s the clincher.

Canada is not getting the labour productivity gains to go along with such explosive real wage gains. Most economists would argue that real wage gains (ie: inflation adjusted) that are not accompanied by productivity gains can feed inflation risk. More inflation risk, means relatively more pressure on borrowing costs since the Bank of Canada’s job is to manage inflation risk. Wage settlements on their own won’t carry the day for the BoC outlook, but they serve as a cautionary flag on the rates outlook. More pay, pay more in interest.

They could also serve to make the household sector relatively more resilient in the face of tariffs and other pressures. That’s a plus for consumer spending and housing markets—but not necessarily housing affordability—at least in the relatively short- to medium-term. Over time, productivity gains must catch up to such real wage pressures. If not, then competitiveness deteriorates even more and with that could be a more vulnerable labour market especially in the face of trade threats. Canada may not be helping itself here.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.