| ON DECK FOR FRIDAY, APRIL 4 |

KEY POINTS:

- Sharp risk-off sentiment as China retaliates

- China announces tariffs, critical minerals restrictions, company restrictions

- Where will Chair Powell land in balancing risks to growth, jobs and inflation?

- Nonfarm payrolls preview, but who cares

- Ditto for Canadian jobs

- Otherwise light overnight releases

Markets continue to mourn the economy we used to know. Trump lit the trail of gun powder and we have no idea where it’s leading and how many times it may branch off. Stocks are under pressure yet again as the Trump tariffs continue to destroy wealth and as China imposed massive retaliatory moves against the US. So far, US and Canadian equity futures are down by nearly 3%+ and falling and European cash markets are down by between 4–7%. US equity wealth has dropped by about US$7 trillion and counting in about six weeks. US economic policy from the dark ages including tariffs and broader US policy uncertainty are proving to be the ultimate wealth killers.

Sovereign bonds are rallying hard. Multiple global benchmarks across US Treasurys, gilts and EGBs are down double digits including 19 big ones in US 2s. It’s unclear that the dollar is back as the CHF and yen are outperforming again while the euro is holding its own. Oil prices are down another 6%+ and gold has clawed its way back from earlier losses overnight to post a small gain following the China headlines.

CHINA RETALIATES

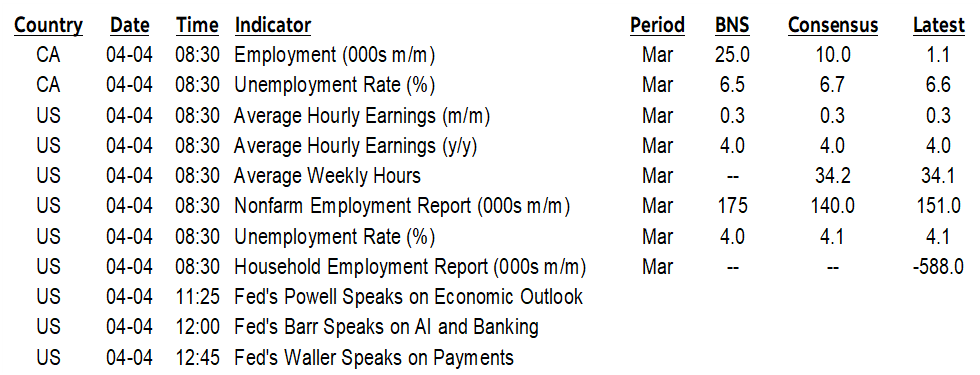

China announced a 34% tariff on imports of US goods, export controls on rare earth minerals, an import ban on some targeted items like poultry and sorghum, added 11 US companies to a list of unreliable entities, and threw 16 US companies on a restricted list for ‘dual-use’ items that are goods, software, and technology that can be used for both civilian and military applications. Chart 1 shows the bilateral goods trade figures.

Otherwise, there was very little by way of new developments overnight other than stale data. Light data showcased weak German factory orders, softer than expected Swedish inflation for Riksbank followers, and weak Asian inflation readings for March. In all cases, the narrative has been reset by tariffs.

CHAIR POWELL’S SPEECH MAY BE KEY

This is when a leader shines. Hopefully. Chair Powell’s speech on the economic outlook arrives at 11:25amET and hence after payrolls. He’s got to sound much more cautious toward the outlook. But cautious how so?

It’s obvious this is all very bad for US and world growth. No Nobel prizes to be had there. The uncertainty factor alone is resulting in investors and c-suites aggressively pulling in their horns.

But key is what does he say about dual mandate pressures. Yes, the outlook for payrolls beyond this morning’s backward look is to the downside, but nonfarm breakevens are moving lower with tighter immigration policy. My bias is toward much more inflation for longer and that will make him at least somewhat balanced. Key is where he positions the pendulum between growth and employment downsides, versus inflation upsides all the while aware of the fact that emboldening Trump’s severely misguided trade policies would be the granddaddy of all moral hazard issues.

A pair of other BoG members will also speak after Powell including Barr (12pmET) and Waller (12:45pmET). Waller may be most likely to offer narrative twists.

NONFARM PREVIEW

Oh but nonfarm payrolls and Canadian jobs are coming due. Bwah! Talk about missing the forest for the trees if anyone thinks March numbers will settle much of anything. See my Global Week Ahead for fuller perspectives.

March payrolls and related figures arrive at 8:30amET. This is one of two payrolls reports before the May 7th FOMC. It’s just on the heels of massive US tariffs and retaliatory moves by China, Canada, and with Europe waiting in the wings. It’s just before Powell speaks. Treat accordingly!

Consensus: 140k

Scotia: 175k (I’m ranked 5th of 75)

Range: 80k – 200k (most within 110–180k)

Whisper number: 120k

Std dev: 24.8k

90% confidence band: +/-130k

UR: 4.1% unchanged / Scotia 4.0%

Wages: 0.3% m/m SA

Rationale:

- Some say weather will give a lift. That’s possible imo for the household survey, not so much for the payrolls report. The measures of how jobs were impacted by weather differ sharply in the two reports. A weather-induced rebound in household employment more than the LF is the theory behind the dip in the UR derived from the household survey.

- it’s likely too soon for federal government jobs to be a big drag. Maybe some, but most of that is ahead, and hiring by state and local governments has been strong and may continue to be an offset for now.

- There were about 20k striking workers through the whole February nonfarm reference period and then only 5k through the March reference period. This should be a modest return to payrolls.

- March is a normal seasonal up-month for hiring. The SA factor is expected to be quite weak and tamp that down.

- on tariffs, it’s likely too early to see much of an effect to the lagging consequences. They could perversely buoy hiring in the short-term through tariff front-running and hesitation to invest which tilts the capital-labour ratio toward labour.

- As for advance indicators, they’re mixed and it would be irresponsible to read too much into them as nonfarm predictors. Here they are:

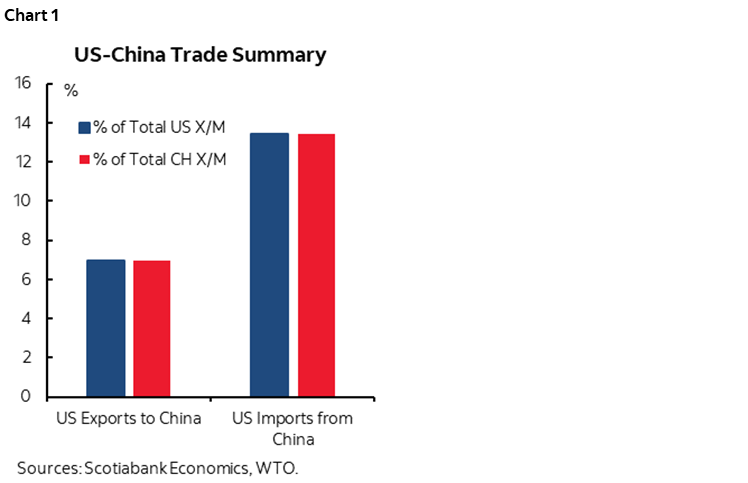

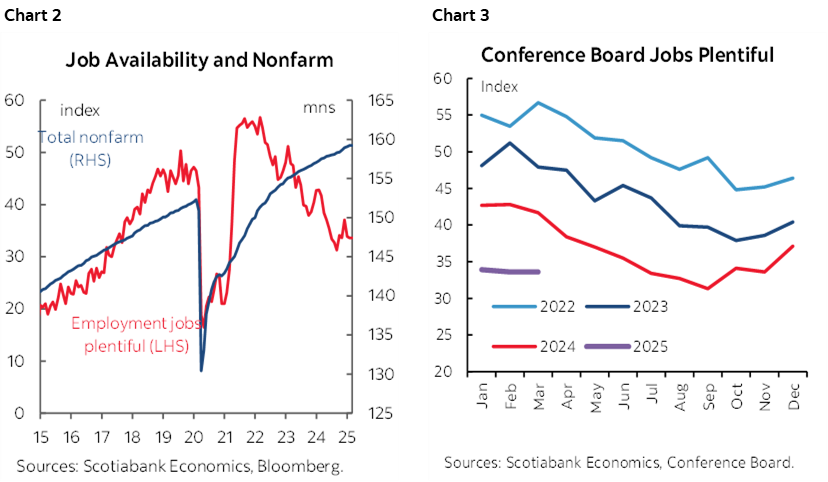

- consumer confidence jobs plentiful was stable. Take little comfort in that (chart 2), but recognize that it is shifting down year after year (chart 3).

- initial jobless claims between reference periods were stable to slightly lower.

- ADP was 155k but offers a poor track record for initial ADP prints versus initial private nonfarm prints.

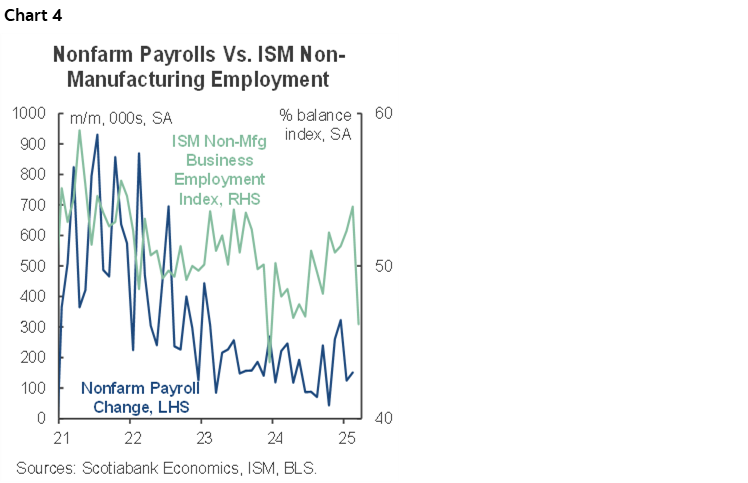

- ISM-services-employment fell 7.7 points to 46.2 and into contraction. Having said that, ISM-services has indicated contracting payrolls with sub-50 readings on the employment subindex 7 times in the 11 months since the start of last year and yet payrolls have never once declined. You figure out a pattern in chart 4.

- ISM-mfrg-employment fell to 44.7 from 47.6

- JOLTS slipped to 7.568 million in February from 7.762. I wish I had a nickel every time someone told me that mattered and it didn’t.

- Challenger job cuts soared to 275k in March from 172k. They were heavily skewed toward federal government layoffs, but that is unlikely to translate into nonfarm at this point. Many layoffs are deferred, or packages will take some time to show up as payroll declines.

CANADIAN JOBS PREVIEW

Canada’s Labour Force Survey for March arrives at 8:30amET. Irrrrrrrelevant! Whether or not it sparks market wiggles, it doesn’t matter amid intensifying forward-looking risks to the whole global economy.

Consensus: 10k

Scotia: 25k (I’m ranked 1st of 12)

Range: -20k to +25k (most within about 10–20k)

Whisper number: n/a

Std dev: 10.9k

95% confidence band: +/-57k

UR: 6.7% from 6.6% / Scotia 6.5%

Wages: 0.3% m/m SA

Some rationale:

- This is the last set of job market readings before the BoC’s April 16th decision.

- Weather might lift Canadian jobs. This was a worse than recently normal February. Lost hours due to weather soared. Jobs during the reference week also probably paid a price in some categories.

- There are precious few advance signals to go by in Canada. The CFIC indicates that hiring plans among small businesses over the next 3–4 months have cooled but that doesn’t necessarily impact March. ‘Indeed’ job postings have recently trended a little lower.

- March is a normal seasonal up-month for jobs, but the SA factors for March have been the lowest on record in recent years when comparing like months of March.

- Tariff front loading might lift employment in the short-term.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.