ON DECK FOR WEDNESDAY, APRIL 30

KEY POINTS:

- Dizzying data dump drives mixed global markets

- It’s month-end—and the end of Trump’s disastrous first 100 days

- US auto tariff rebates layer on complexities as the administration bullies retailers

- China’s PMIs signal weakening growth on trade wars

- Eurozone CPI is tracking hotter than expected

- Eurozone growth was a bit firmer than expected, but it’s history

- European consumers didn’t engage in tariff front-running

- Chile’s central bank held, Thailand’s cut—both widely expected

- BanRep: hold, with cut risk after a previously close decision

- South Korean factories front-loaded production, Japanese ones did not

- Aussie CPI was warmer than expected

- Mexico’s economy probably posted little if any growth in Q1

- US ADP private payrolls don’t matter

- US Q1 GDP: Why there are wide ranging expectations for a soft quarter

- US core PCE probably ended Q1 on a soft note ahead of coming price pressures

- Canadian GDP: Soft February, March and Q1 expected

- US ECI likely to continue to showcase employment cost pressures

- US consumer spending probably ended Q1 on firm foundations ahead of downsides

- BoC’s little watched Summary of Deliberations probably won’t garner attention

Global markets are cautiously going into month-end. US and Canadian equity futures are mildly lower and European cash markets are mixed. The very mildly cheaper US Treasury front-end is slightly underperforming small rallies across European curves. The dollar is mixed; CAD continues to show absolutely no reaction to the Canadian election as a middle of the pack performer to the USD. Oil and gold prices are a little lower.

Aside from month-end and the conclusion of Trump’s disastrous first 100 days, there was a massive overnight data dump ahead of an equally massive North American data dump this morning. I say disastrous because his trade policies are fruitless and dragging everyone down including the US economy, by his own words he is at best “months” away from a budget bill given deep divisions within the GOP, nothing has been achieved on regulatory fronts, immigration policy is error prone, US relations with allies are in tatters, and markets are paying a steep price for all of this.

There continues to be evidence that Trump is backing down from flabbergasting tariffs to only absurdly high ones with his latest executive order that applies complex rebates to some of the auto tariffs. The calculations around what it means are complicated and layer on regulatory costs rather than just admitting the US administration is messing up and doing away with its tariffs. Europe and China are not calling to negotiate. And the administration’s pressure against retailers like Amazon not to disclose the tariff effect on prices smacks of a bias toward 1970s price controls whether explicit or implied.

RECAP OF HEAVY OVERNIGHT RELEASES

Here’s a recap of overnight releases and developments before turning to expectations for N.A. releases:

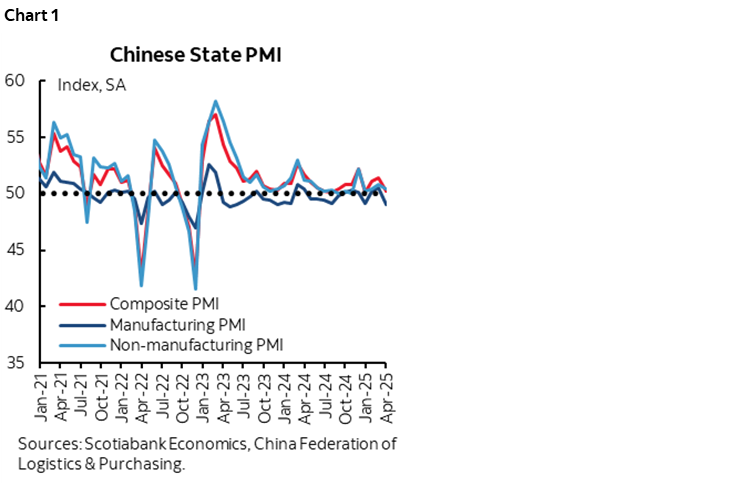

- China’s state PMIs slipped again (chart 1) as the US-driven global tariff war is taking its toll. Just wait until the next rounds as orders dry up ahead of empty store shelves appearing in the US. The composite PMI fell 1.2 points to 50.2 and hence on the border between growth and contraction. The manufacturing PMI fell into sub-50 contraction at 49.0as export orders fell while the non-manufacturing PMI slipped by 0.4 to 50.4. The private version of the manufacturing PMI fell 0.8 points to 50.4; unlike the state PMI that is more skewed toward SOEs, the private one is more weighted toward smaller producers in more export-oriented coastal cities.

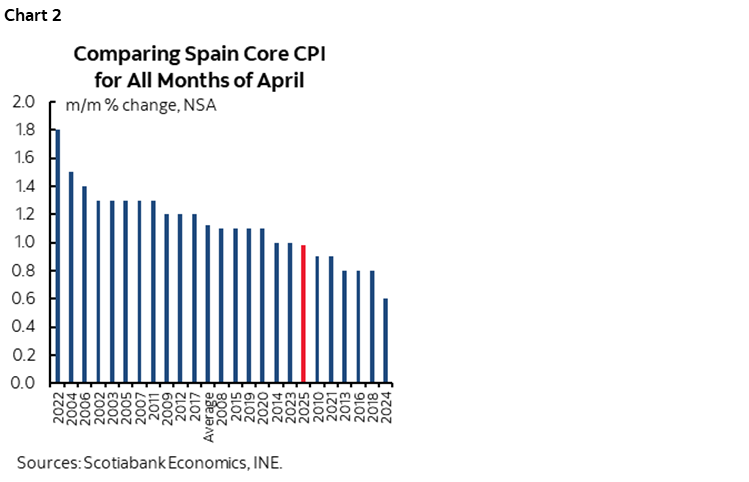

- The full eurozone tally for CPI doesn’t arrive until Friday, but it’s looking like consensus expectations are a little light based on the fact we now have the biggest countries’ figures. German CPI in April is tracking a little warmer than expected based on the release of figures across individual states ahead of the national reading a little later this morning. The states posted CPI increases of between 0.4–0.5% m/m. Consensus was expecting 0.3, or 0.4 on an EU-harmonized basis for the national reading. France’s CPI figures for April were also hotter than expected at 0.6% m/m (0.4% consensus). Italian CPI was a smidge lighter than expected at 0.5% m/m (0.6% consensus). Also recall that Spain’s figures yesterday morning doubled consensus expectations at 0.6% m/m but the core CPI measure was on the lighter side of history in seasonally unadjusted terms when comparing like months of April (chart 2).

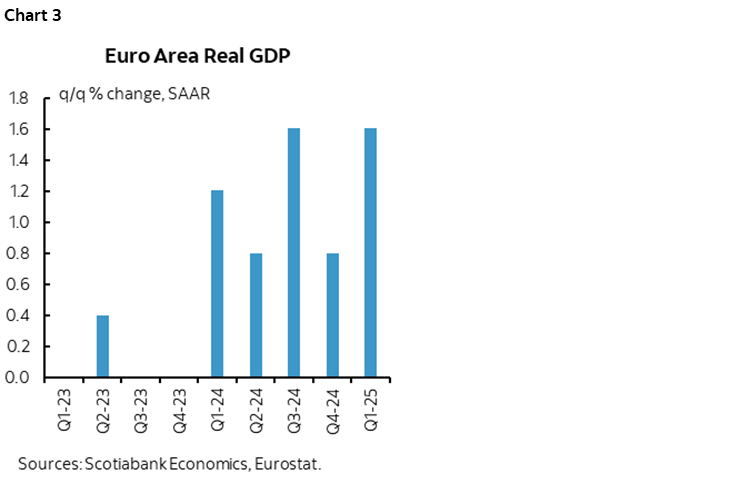

- Eurozone growth was a little firmer than expected at 0.4% q/q SA (0.2% consensus) in Q1. It’s just a footnote as trade wars will drag down everyone’s growth going forward. The annualized growth rate was low but tied for the second warmest reading in recent quarters (chart 3).

- There wasn’t any clear evidence of tariff front-running by European consumers in March. French consumer spending fell -1.0% m/m after being little changed the prior month. Germany retail sales volumes slipped -0.2% which was a bit less of a drop than expected, but the prior month was revised down 0.6 to 0.2% m/m.

- Chile’s central bank held its policy rate unchanged at 5% as widely expected.

- The Bank of Thailand also met expectations by cutting its benchmark rate 25bps to 1.75%.

- South Korean factories were a beehive of activity in March, driving industrial output up by 2.9% m/m after a prior gain of 1.4% that was revised up from 1.0%. Tariff front-running was a likely driver.

- Japanese industrial output did not reflect the same front-loading. It was down 1.1% m/m in March but following a larger 2.3% rise the prior month. Retail sales were also down 1.2% m/m.

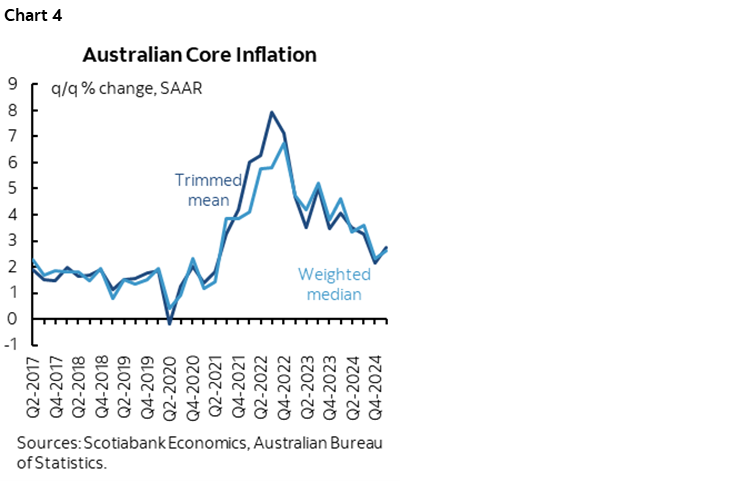

- The A$ appreciated and short-term Australian yields rose a touch on the back of firmer than expected Australian CPI inflation. Total CPI was up 0.9% q/q SA nonannualized in Q1 (0.8% consensus). Chart 4 shows a pick-up in core measures. Trimmed mean CPI was up 0.7% (0.6% consensus, 0.5% prior) and weighted median CPI was up 0.7% matching consensus but accelerating from an upwardly revised 0.6% (from 0.5%).

N.A. DATA DUMP—US GROWTH AND INFLATION, CANADIAN GROWTH TO DOMINATE

Here are brief highlights of the coming data dump this morning in chronological order.

- Germany releases the national CPI figure shortly (8amET)

- Mexico’s economy probably posted very little if any growth in Q1 with consensus estimating 0.1% q/q SA nonannualized (8amET).

- US ADP private payrolls are due out at 8:15amET for the month of April. They’re not a useful guide to nonfarm private payrolls that arrive on Friday. Consensus expects +120k with Scotia’s estimate at 145k.

- Q1 US GDP is due at 8:30amET. Consensus is at -0.2% q/q SAAR. Scotia’s estimate is -1.1%. The range within consensus is from -2.4% to +1.7% with most estimates between -1% and +1%. The Atlanta Fed’s ‘nowcast’ excluding the distorting effects of gold is -1.5%. The wide range of estimates is due to the fact there is a lot of missing data at a critical juncture for when tariff nonsense heated up at quarter-end. Scotia Economics is the only group in Scotia that uses a large-scale macroeconometric model devised by one of the country’s best modellers and supplements this with judgement, narrative-based economics and in-quarter data tracking. If I say there is greater than unusual uncertainty into these numbers given this best-efforts approach then it should be respected.

- US Q1 core PCE is also due out (8:30amET) and based on data to February and expectations for the March release of PCE inflation figures (10amET) Scotia expects a reading of about 3% q/q SAAR. March is expected to come in at -0.1% m/m SA for headline PCE and +0.1% for core.

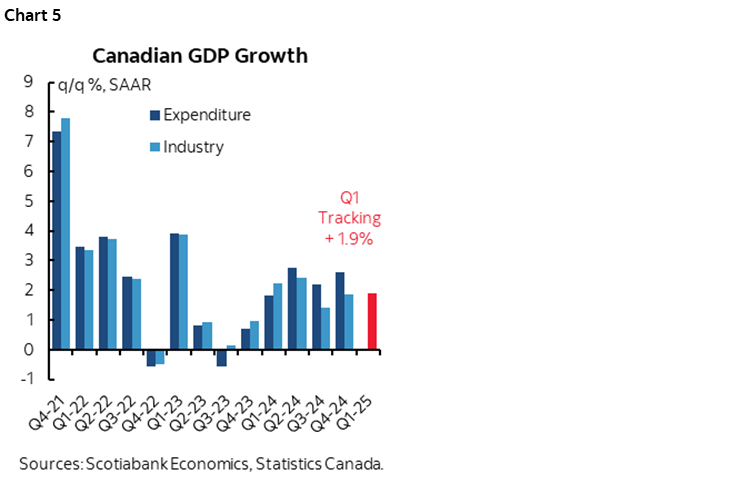

- Canada refreshes GDP figures for February and March (8:30amET). February was initially guided to be “essentially unchanged” by Statcan way back on March 28th which could mean anywhere from -0.1% to +0.1% m/m. I went with -0.1% and my simple regression model based on partial data leans toward a bigger drop. March is expected to be little changed with a slight nod toward a small gain based on a rise in hours worked and limited other readings. If such expectations are on the mark and there are no major revisions, then Q1 GDP growth on a production accounts basis is likely tracking around 1½–2% q/q SAAR (chart 5).

- The US Employment Cost Index for Q1 (8:30amET) that combines all elements of compensation is expected to post another nonannualized q/q gain of about 1% SAAR. This, along with nonfarm business GDP in today’s GDP accounts, will serve as input into expectations for next week’s Q1 productivity and unit labour costs.

- US nominal consumer spending (10amET) is expected to post solid growth based in part on the known 0.4% m/m gain in the retail sales control group for March plus an expected gain in services. Consensus is at 0.6% m/m and Scotia’s estimate is 0.5%. Personal income is expected to grow a little slower than spending which implies a modest dip in the saving rate.

- US pending home sales for March are due at 10amET.

- The BoC’s little watched Summary of Deliberations to the discussions leading up to the April decision is due at 1:30pmET. I still long for a disclosed vote and formal meeting minutes in keeping with best practices at other global central banks.

- Colombia’s central bank is expected to hold its policy rate at 9.5% with our LatAm economists in the minority expecting a 25bps cut partly based upon how close the vote was the last time (2pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.