ON DECK FOR TUESDAY, APRIL 29

KEY POINTS:

- Canada’s election poses more questions than answers...

- ...with CAD and rates unchanged as expected

- Carney’s Liberals look set to win a minority with counting ongoing…

- ...but the country is deeply divided

- Don’t rule out Canada returning to the polls…

- ...as the Liberals will have to thread the needle with unpalatable governing choices…

- ...amid highly uncertain steps forward for trade negotiations and fiscal policy

- What will orphaned NDP MPs do?

- Seat projections failed in a big way this time

- Voter turnout started high, then fizzled

- Conservative leader Poilievre lost his seat, faces uncertain future

- NDP loses official party status, Singh also loses and resigns

- US softens auto tariffs

- US JOLTS, consumer confidence on tap

- EGBs ignore warmer than expected Spanish CPI

Right now, Canada’s Liberals are tracking a minority win that is a few seats short of a majority but there remain several close seats with vote counting continuing. The C$ is flat to the USD and very slightly outperforming other crosses on a morning of broad dollar strength. BoC pricing is unaffected by the election results. The Canadian rates curve is performing in line with US Treasury yields. The lack of clear market reactions was expected given a) important external factors, b) key risks ahead including trade negotiations and fiscal policy, and c) uncertainty around the outcome itself.

Overall, it’s a strong reversal compared to what had been the tracking of a massive Conservative majority not long ago, but it’s well shy of the sizeable majority that the Liberals were expecting and that both 338Canada.com and the CBC’s poll tracker were estimating (charts 1, 2). That leaves both main political parties thankful that neither of them got blown out while lamenting what could have been. If current results roughly stand, then the Liberals will be roughly twenty seats below what 338Canada and CBC’s poll tracker were projecting.

Chart 3 shows voter turnout with 99% of polls counted. After a record share of eligible voters cast their ballots in advance polling, turnout fizzled on game day. The result is higher turnout than the weak numbers in 2021, but well below what momentum could have driven. Sadly, not enough folks could bother getting off the couch to vote on election day itself.

As shown in maps of the vote outcome by region, Canada is a highly divided economy in need of skilled consensus building on key issues. Hubris is out, negotiating is in. Chart 4 shows that it was Ontario that held the Liberals back from a majority as they won fewer seats in that province than in the 2021 election.

Minority governments tend to be short-lived in Canada and usually last about 2½ years or just months in some cases (chart 5). If this Parliament yields an unworkable consensus around key policy matters, then we cannot rule out a need to go back to the electorate again if agreement on key steps forward becomes unachievable. It’s not hard to think of scenarios where there would be deep divisions in Parliament on, say, trade and fiscal policy matters.

Another risk is what the orphaned 5 elected NDP MPs and 2 others who are leading decide what to do now that their party is, well, no longer officially a party and without a leader. I doubt they would cross the aisle to join the Liberals to craft a majority which would fully destroy the NDP versus staying alive for future fights, but monitor this issue and I wouldn’t be surprised if the Liberals sought their support. They certainly will on individual votes.

Here's where things stand now in terms of seats as shown in chart 1.

- Liberals elected 155, leaning 13, total 168

- Conservatives elected 133, leading 11, total 144

- BQ elected 21, leading 2, total 23

- NDP elected 5, leading 2, total 7

- Green elected 1, leading 0, total 1.

And here are the figures for vote shares as shown in chart 2:

- Libs 43.5%

- Cons 41.4%

- BQ 6.4%

- NDP 6.3%

- Green 1.2%

Key Takeaways:

- It’s a Liberal minority at this point as they remain a few seats shy of the magic number of 172 for a majority.

- Conservative Leader Pierre Poilievre lost his seat by a 50.6% to 46.1% margin to the Liberal candidate. His future is unclear at this point.

- NDP leader Singh also lost his seat and announced his resignation as party leader. He placed a distant third in his riding with 18.1% of the vote versus the Liberal leader at 42.1%.

- Carney handily won his seat.

- The BQ’s Blanchard won his seat.

- The NDP is well shy of the 12 seat minimum for official party status. They won 25 seats in 2021.

- The BQ has also suffered a significant setback compared to winning 32 seats in 2021.

- The Conservatives look set to improve upon their 2021 outcome when they won 119 seats with 33.7% of the vote.

- The Liberals are tracking a little better than in 2021 when they won 160 seats but with about 11 points higher share of the vote this time than in 2021.

- CTV jumped the gun declaring a Liberal minority last evening but may ultimately be proven correct. CBC has yet to call anything other than a Liberal victory but is holding off on the minority or majority call.

- A minority outcome presents no realistic prospects for a formal coalition. It would be anathema to partner with the BQ and forget about a formal coalition between the two main historic rivals. Instead, an issue-by-issue approach to governing that relies upon vote support from the Conservatives and/or BQ lies ahead. That magnifies risk around trade negotiations and fiscal policy efforts.

- With the election over, the focus now turns to what really matters including trade negotiations with the US and how to craft fiscal policy with a minority government.

OTHER OVERNIGHT DEVELOPMENTS

Other overnight developments were light. A reason for broad dollar strength is that the Trump administration is back pedaling on auto tariffs somewhat.

Overnight releases were largely ignored, including slightly firmer than expected Spanish CPI (0.6% m/m, 0.4% consensus) and core CPI (2.4% y/y, 2.3% consensus, 2.0% prior). Spanish GDP also started Eurozone GDP tracking but with a miss (0.6% q/q, 0.7% consensus) and a slight downward revision to the prior quarter (0.7% from 0.8%).

Eurozone inflation expectations edged up a tick in the 3-year measure (2.5%, 2.4% prior) and up three-ticks to 2.9% for the 1-year measure.

US DATA ON TAP

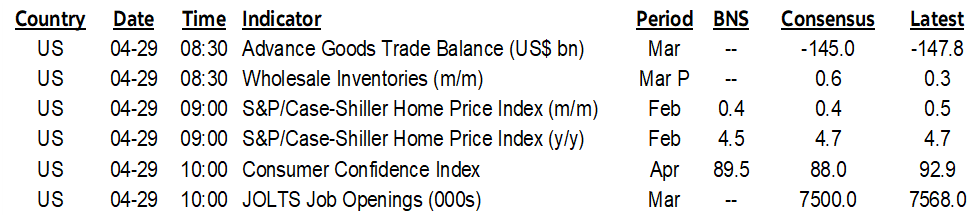

On tap into the N.A. session will be several US releases with the main focus on JOLTS for March and consumer confidence in April, both at 10amET. The US advance merchandise trade figures for March (8:30amET) and repeat-sale house prices in February (9amET) are also due out.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.