ON DECK FOR MONDAY, APRIL 28

KEY POINTS:

- Higher bond yields greet Canadian voters

- It’s Election Day in Canada

- When polls open, and when to expect results

- Like the UK, whomever wins Canada’s election may not claim broad support

- Expected election results…

- ...and yes, the seat mapping sites can and have been wrong

- Both parties underestimate what they would do to fiscal deficits…

- ...but the Liberals’ numbers are probably far bigger by assuming a long crisis

- Six reasons why it’s a waste of time predicting election effects on markets

- Why a surprise minority would probably be more unworkable this time

- Global Week Ahead—Only, 1,287 More to Go! (here)

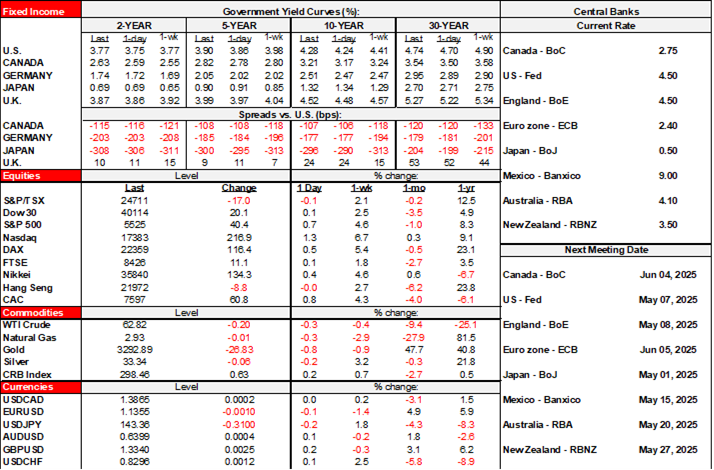

It’s Election Day in Canada. Finally. Frankly, nothing else much matters given a paucity of other considerations to start the week. How appropriate that sovereign bond yields are under mild upward pressure in the US, Canada and Europe given the likely debt issuance that may follow. US and Canadian equity futures are slightly lower while Europe is rallying by about ¾% across exchanges. The dollar is mixed. Oil and gold prices are gently lower.

WHEN POLLS OPEN?

About one-quarter of eligible voters voted in the advance polls. For the rest, polls opened first in Newfoundland at 7amET and then the rest of Atlantic Canada at 7:30amET. They will be followed by Ontario, Quebec, Manitoba, Saskatchewan and Alberta at 9:30amET, and then BC at 10amET. It’s a big country with lots of time zones.

WHEN TO EXPECT RESULTS

We should have results later tonight. Results will start rolling in shortly after polls close in Newfoundland at 7pmET and then the rest of Atlantic Canada after 7:30pmET. Key will be when Ontario, Quebec and the prairies begin reporting after 9:30pmET and then if it’s close, after BC begins reporting after 10pmET. I would guess that we’ll probably know by 11pm, maybe a little earlier or a little later. If the seat mapping sites are close to the actual outcome, then their projected tallies could make BC’s outcome count.

WHOMEVER WINS, BE HUMBLE!

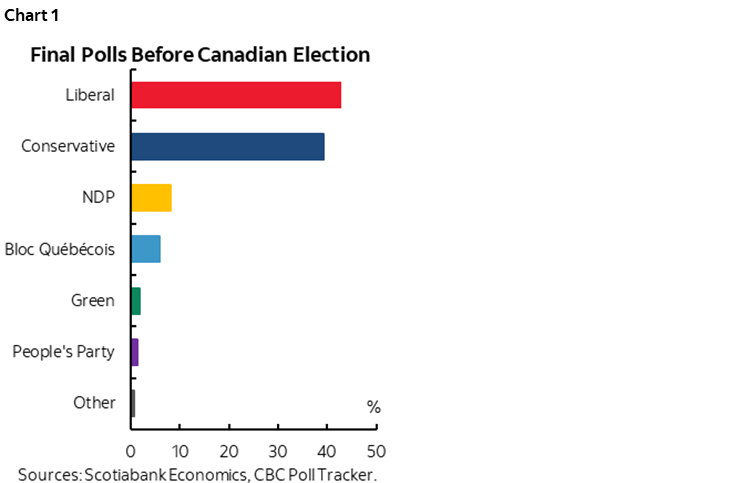

Whomever wins—most likely the Liberals—will not have the support of a majority of Canadian voters (chart 1). Roughly six-in-ten voters will choose another party, according to the polls. The country is likely to remain highly divided, so can any hubris about getting a clear mandate to govern from a majority of Canadians. The outcome will speak more to the political divisions within a first-past-the-post parliamentary system. Ask the UK about that one, after Labour’s massive 2024 majority (411 out of 650 seats) was won with just about one-third of the popular vote.

THE EXPECTED OUTCOME

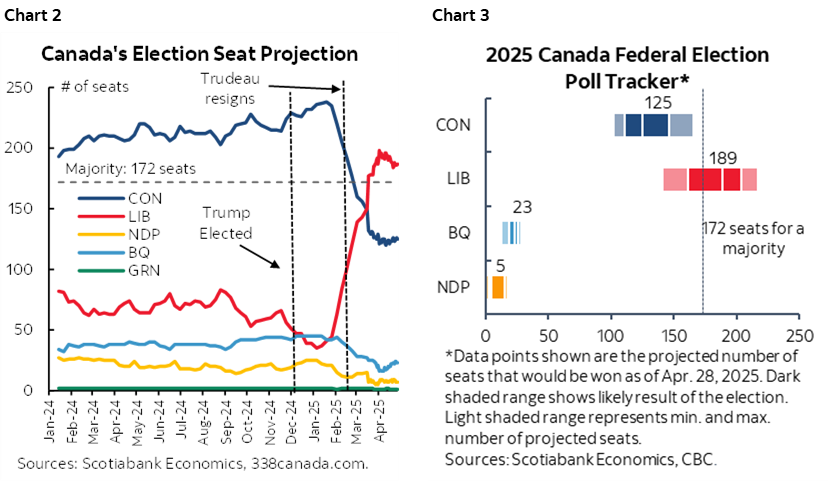

Charts 2 and 3 show expected outcomes using the two main seat mapping sites. 338Canada projects a 15-seat Liberal majority with 187 seats, versus 125 for the Conservatives, 23 for the BQ, 7 for the NDP and 1 for the Greens. They estimate 42% support for the Liberals and 39% for the Conservatives.

CBC’s poll tracker estimates a Liberal majority with 189 seats versus 125 for the Conservatives, 23 for the BQ, 5 for the NDP and 1 for the Greens. The estimate about 43% support for the Liberals and 39% for the Conservatives with 8.1% for the NDP, 6% for the BQ and 1.8% for the Greens.

Note the lines on chart 2 for when Trump got elected versus when PM Trudeau resigned. The US-centric American media thinks this is all about Trump’s influences. Astute observers know it is at least as much about voter dissatisfaction with the ten years of former PM Trudeau’s administration and evaluating policy pivots by the current Liberals and the Conservatives.

YES, THESE SITES CAN BE WRONG

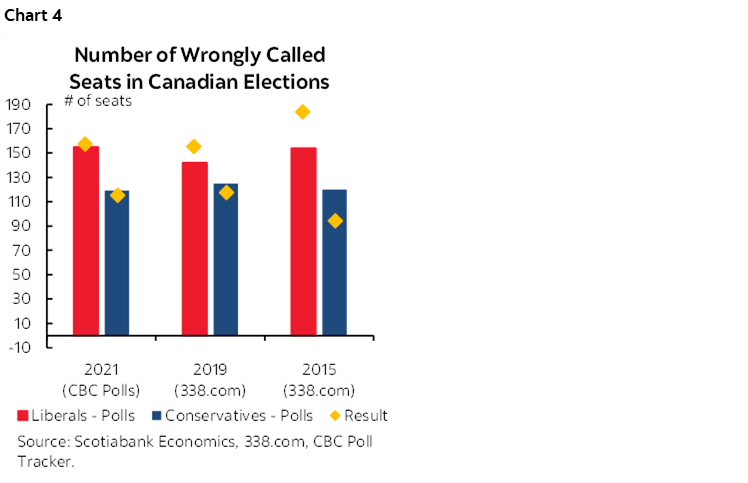

Seat mapping sites have been wrong as shown in chart 4 that displays the incorrectly estimated number of seats won by party in each of the past three elections. 2021 was close. 2019 under-predicted the number of Liberal seats won in their minority, and 2015 sharply under-predicted the Liberal majority. The site creators say their models are better now, but they could still be prone to error.

A MINORITY WOULD BE MORE AWKWARD THAN USUAL

The seat mapping sites given ranges around their projections which is natural given the polling uncertainty. Those ranges overlap around scenarios that involve both Liberal and Conservative majorities. Minorities can be tenable if a suitable supporting partner is available. That may not be the case this time. Unless polls are massively off base, then the NDP is likely to be reduced to a bit player. It would be anathema to both political parties to strike a coalition with the BQ that a) has no interest in governing, b) is merely a regional Quebec-based party, and c) champions interests that are often misaligned with the rest of the country.

SOMEONE’S GONNA BE TICKED

There will be stark regional differences. If the polls and seat mapping sites are anywhere close to being correct, then a Liberal majority will be overwhelmingly driven by voters in Ontario and Quebec. The Atlantic provinces are expected to strongly vote Liberal. Races in BC and Manitoba look closer. Alberta and Saskatchewan won’t be pleased, given strong Conservative leanings.

MARKET EFFECTS? DON’T HOLD YOUR BREATH

As for market effects, don’t hold your breath for the following reasons that also emphasize how the election only begins the potential effects in the weeks and months ahead.

- Election effects on markets are notoriously difficult to anticipate and usually wrong even if the outcome is as predicted.

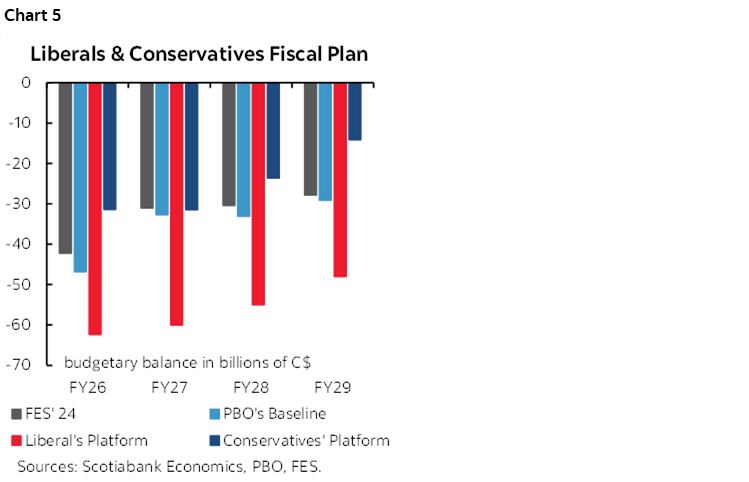

- Election platforms are often notoriously different from what actually gets delivered. Promises, promises! Take chart 5. Deficits keep ballooning from the Fall Economic Statement in December to the Parliamentary Budget Officer’s now stale baseline based on outdated macro forecasts in early March, to the costed numbers offered by the parties in their election platforms. The Liberals promise massive deficits for years to come. The Conservatives also project sizeable deficits. The Conservatives’ numbers are probably understated because of dynamic revenue scoring and the use of stale macro inputs. Fair and balanced commentary should also note that the Liberals’ deficits may also be sharply underestimated by using the same stale macro inputs that overstate growth, because their promise to hold operating core program spending gains to 2% per year will be believed when seen given their free spending track record by what is largely the same cast, and because their plans are heavily reliant upon heavy infrastructure spending that notoriously lowballs ultimate project costs given evidence from the literature on final tallies versus initial estimates. The Liberals assume a permanent crisis requiring years of much greater government intervention which may or may not be correct. Neither party has much fiscal policy optionality around what might actually happen, but the bigger commitment by far is within the Liberals’ plan.

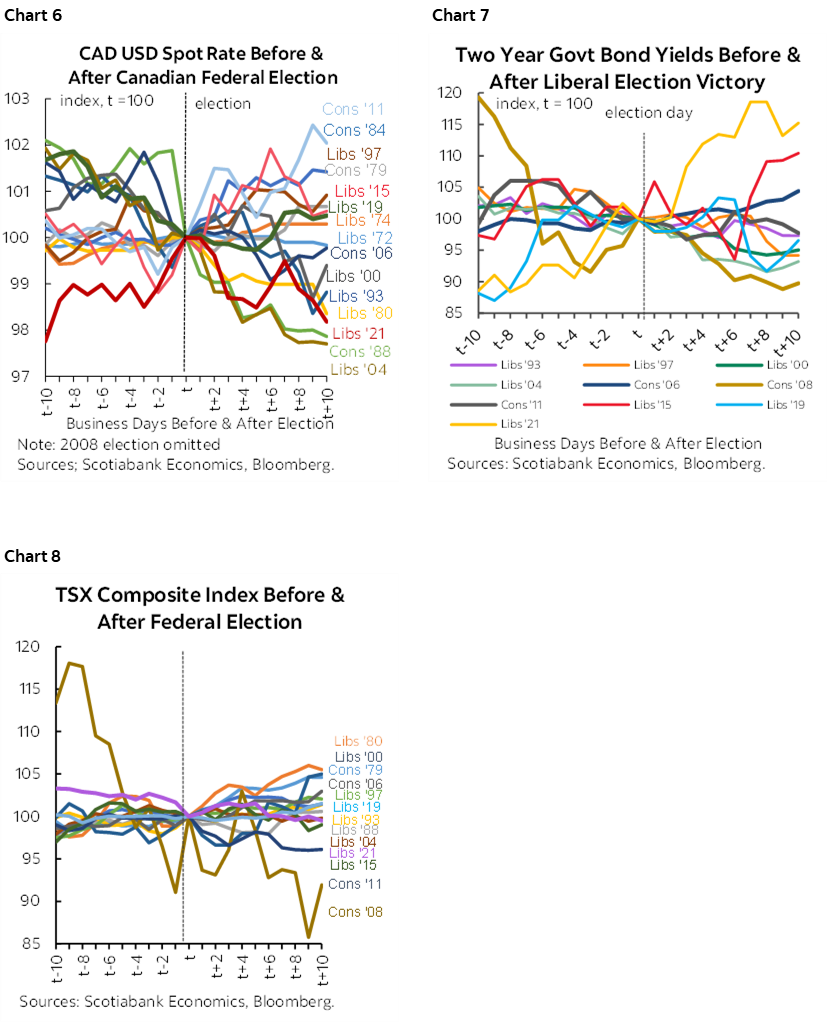

- Charts 6–8 show what happens to USDCAD, bond yields and the TSX after past elections. Good luck discerning any reliable pattern. All elections present differing policy options, but good luck if you’re looking for a clear outcome once uncertainty about the results abates.

- This week is packed with developments in Canada and abroad. That could mean that market participants will be highly guarded in anticipation of nonfarm, PCE, US and Canadian GDP, the BoJ, and multiple other global releases and developments plus the usual noise out of the US administration. Canada is a modestly sized, open economy that is a price taker for many of the goods its produces which means it is often heavily driven by global factors.

- Other than near-term calendar-driven effects, external developments are likely to continue to be more important to the Canadian dollar than domestic politics, at least for a while. The appreciation of CAD to the USD from its peak weakness in late January and through its accelerated appreciation in April has been driven by USD weakness as markets heaped on an extra 50bps or so of Fed rate cuts by year-end to 3–4 cuts now, and as reduced appetite for US securities amid severe policy dysfunction in the US weighed on the dollar. And yet, CAD has underperformed other major crosses throughout this period.

- As for domestic drivers of domestic financial markets, they’re not about the election per se. They are about the path ahead into highly uncertain trade negotiations with the US and to what extent fiscal stimulus arrives while introducing trade-offs for monetary policy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.