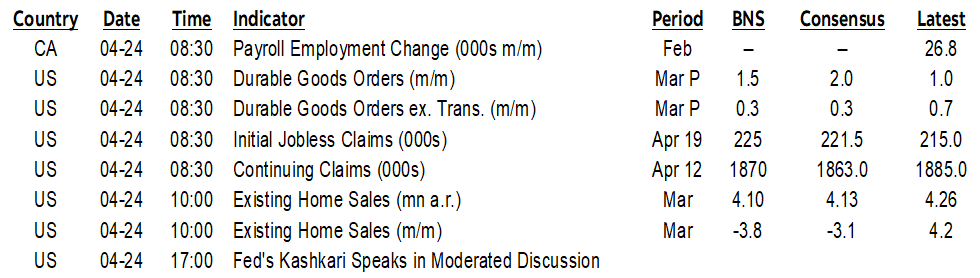

ON DECK FOR THURSDAY, APRIL 24

KEY POINTS:

- Antsy markets second guess trade progress

- China rejects US trade talks

- Bessent, Trump downplay China offer

- Trump renews insulting attacks on Canada, threatens higher auto tariffs

- US to update capital goods orders, home resales, claims

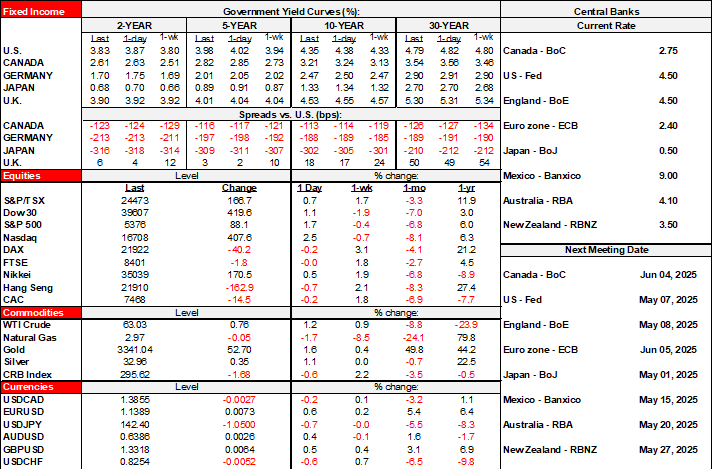

Very mild risk-off sentiment is pushing equities slightly lower across US and Canadian futures and European cash markets. Sovereign bond yields are gently lower across maturities and countries. Against a traditional risk-off set of moves is dollar weakness.

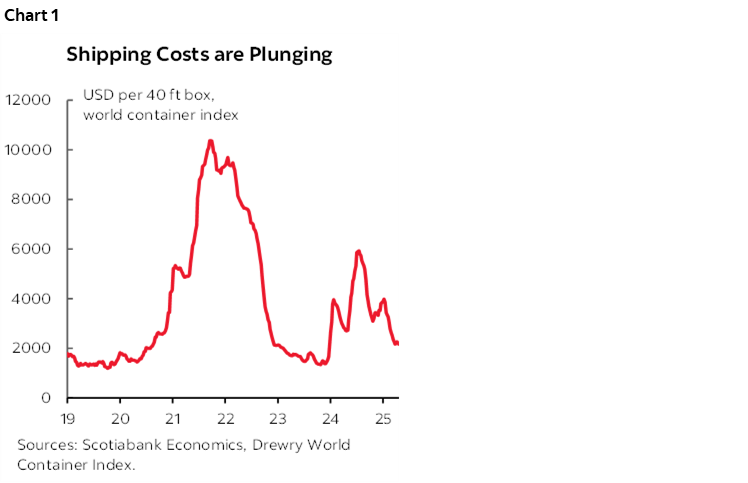

As for catalysts, it seems that nobody wants to play along with Trump’s hardball tactics on trade while his erratic ways are back on display as demand for shipping containers falls (chart 1). Call it the art of the misdeal and how the rest of the world believes the US administration isn’t playing with a full deck. A Chinese Commerce Ministry spokesman said China demands all US unilateral tariffs be removed before trade talks while saying “any reports on developments in talks are groundless.”

Speculation in the press by those mischievously labelled “people familiar with the matter” that the US was backing off tariffs was shot down by Bessent and Trump yesterday. Treasury Secretary Bessent said earlier in the day that there was no unilateral offer from the US to lower tariffs on China and insisted that there had to be agreement by both countries to de-escalate their trade war which China clearly rejected this morning. Then Trump said late yesterday that he was not considering lowering auto tariffs.

Trump also hurled fresh insults at Canada and indicated auto tariffs on the country could rise. He said “I have to be honest, as a state it works great.” Clearly honesty isn’t Trump’s thing, but he went on to repeat made-up nonsense about how the US “subsidizes” Canada by $200 billion per year, and grossly exaggerated the significance of US trade to Canada by saying “95% of what they do is they buy from us and they sell to us” which is several multiples of the actual trade share of Canadian GDP with the US. Trump is easily baited, and so in response to a question on whether he could raise tariffs on Canada he said “At some point, it could go up. All we’re saying is we don’t want your cars with all due respect.” Respect?? Trump??? Bwah.

Other overnight developments were light. German IFO business confidence was little changed in April even in terms of expectations. South Korea’s economy shrank by -0.2% q/q SA nonannualized (+0.1% consensus).

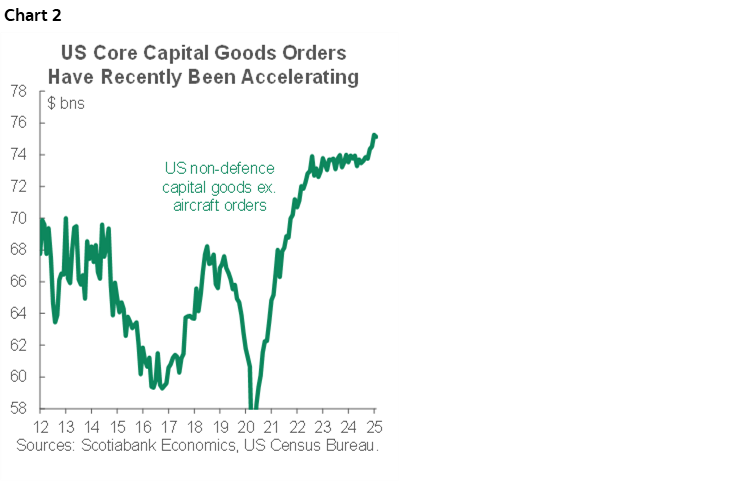

On tap in the N.A. session will be US macro reports including recently rising big-ticket core durable goods orders (chart 2) for March (8:30amET), US existing home sales for the same month (10amET), and weekly jobless claims (8:30amET). Canada refreshes the lagging and incomplete payrolls report for February (8:30amET); the timelier LFS jobs report for April won’t arrive for another two weeks.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.