ON DECK FOR WEDNESDAY, APRIL 23

KEY POINTS:

- The Trump-driven sucker trade is buoying equities

- Trust Trump? His China and Fed comments are being taken positively, for now

- EU actions against US tech and Tesla earnings are being shaken off

- Global PMIs barely elicited any local market responses

- Canada’s Conservatives offered shaky numbers…

- ...that are still more fiscally responsible with greater optionality than the Liberals’ plan

- Bank Indonesia held as expected given stability concerns

The Trump-driven sucker trade is driving equities higher this morning as markets largely ignore milder than feared EU measures against US tech companies, Tesla’s weak earnings, and global PMIs. Trump’s erratic ways are buoying sentiment given his comments late yesterday. Give it time, and he’ll be taking it all back again as trust has been seriously eroded. Equities are broadly higher with US futures up by 2½%+, European cash markets up by about 1–2% after Asian benchmarks moved similarly higher. Sovereign bond curves are flattening with two-year yields up by about 1–7bps across US and European benchmarks and the longer end of the US curve outperforming others with 10s and 30s down 10–13bps. The USD is mixed again.

TRUST TRUMP??

So, in Trump we Trust? Regular readers know what I think about that. And yet he did his best Boy Scout impression late yesterday by jawboning China tariff relief and deescalating his attacks on Fed Chair Powell. When speaking about China tariffs, he said “It will come down substantially but it won’t be zero,” and “we’re going to be very nice and they’re going to be very nice, and we’ll see what happens.”

Oh how nice. So, what’s Trump doing? It’s possible that he realizes he left himself no outs and seriously misplayed his hand. He may be trying to deescalate because China is digging in against tariffs, while the dysfunctional EU has predictably splintered in its response. It’s also entirely possible that Trump comes back tomorrow or at a later date and slams China again. For now, equities trust Trump, but perhaps they never learn.

And on the Fed, Trump said he has “no intention” of firing Powell. He can’t right now anyway. Trump v. Wilcox before the Supreme Court is what he may have in mind and so he is trying to deescalate his unglued rhetoric since the end of last week. That’s the pending case that is likely to be addressed before the Court adjourns for summer break in late June and that will address whether Trump has the power to fire agency heads including the Fed Chair. Maybe his advisors said to knock it off less he wants the Court to fully rule against him.

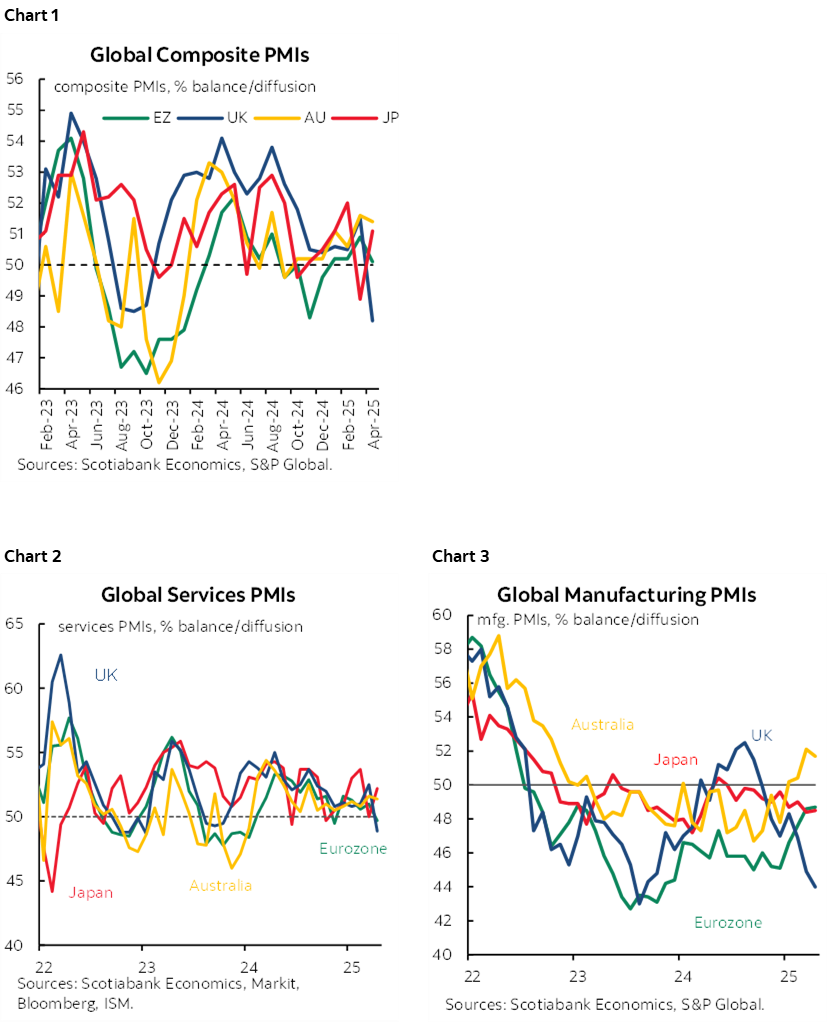

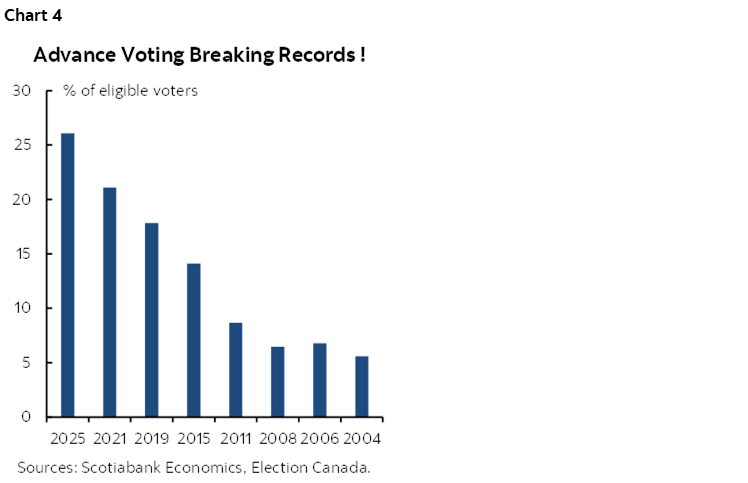

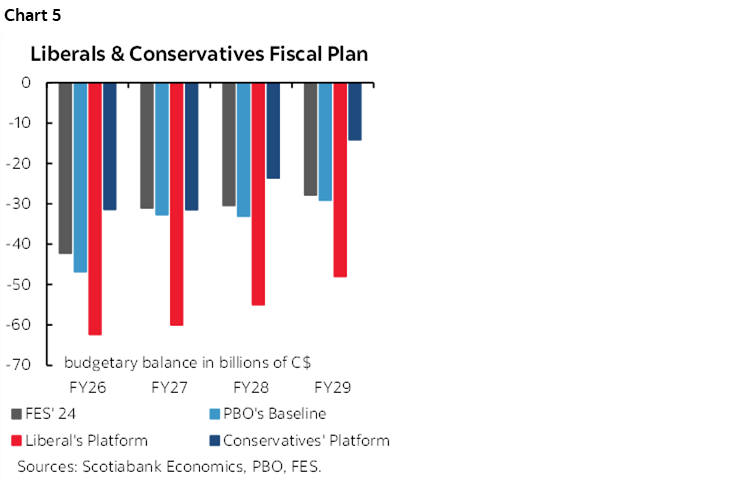

MARKETS PAID LITTLE ATTENTION TO GLOBAL PMIS

A wave of global purchasing managers indices hardly caused a ripple across local markets that are more focused upon the aforementioned issues (charts 1–3). Here’s the rundown.

Australia’s composite PMI held steady given margins of error around soft data (51.4, 51.6 prior). There were small changes in the manufacturing and services PMIs that remain in mild growth territory. The A$ rallied from the point of release onward and is leading gainers to the USD while the Aussie front-end underperformed most other markets with a 7bps rise in the two-year yield.

- Japan’s composite PMI increased back into above-50 expansion territory at 51.1 (48.9 prior) with services leading the way (52.2, 50 prior) as manufacturing remained in contraction (48.5, 48.4 prior). There was little reaction across Japanese financial markets.

- The Eurozone’s composite PMI slipped a bit to 50.1 (50.9 prior) because services decelerated (49.7, 51 prior) while manufacturing remained unchanged in mild contraction. Germany’s composite PMI fell by the most (49.7, 51.3 prior) but France’s remains in deeper contraction (47.3, 48 prior). Minimal market reactions were overshadowed by broader drivers of market sentiment.

- The UK composite PMI fell into contraction (48.2, 51.5 prior) led by a drop in services (48.9, 52.5 prior) but manufacturing also fell a bit further into contraction (44.0, 44.9 prior). The UK front-end is cheapening by less than other benchmarks.

- India’s composite PMI edged a bit higher (60.0, 59.5 prior) led by a 0.6 rise in services to a 59.1 reading.

The S&P versions of the US PMIs will be updated later this morning (9:45amET).

OTHERWISE LIGHT OVERNIGHT DEVELOPMENTS

Bank Indonesia held its policy rate unchanged at 5.75% as widely expected given concern about the rupiah and broader stability.

The ECB’s trade surplus widened in February by about 50% to €21billion with the rise led by a bigger surplus with the US. Surpluses mean little to nothing without understanding the drivers at the best of times. This time is likely being driven by tariff front-running.

CANADA’S CONSERVATIVES’ SHAKY NUMBERS ARE STILL MORE FISCALLY RESPONSIBLE

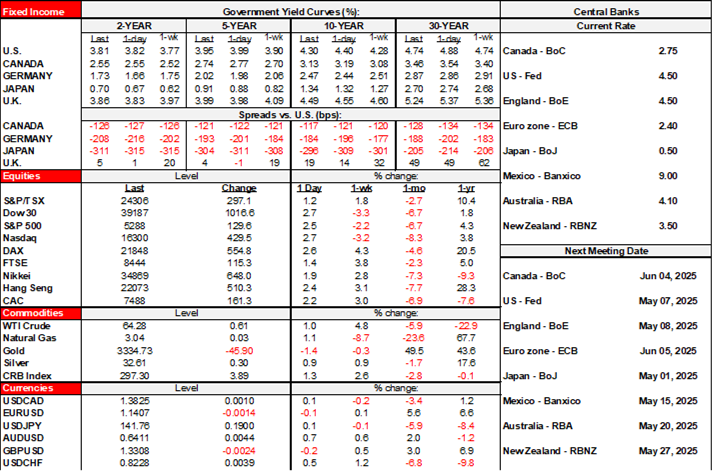

As advance voting breaks records (chart 4), it’s shameful that both leading parties released their costed platforms after the end of early voting. I don’t like seeing the electorate manipulated in such fashion by both parties.

Chart 5 compares deficit projections now that we finally have the fully costed plans from the Liberals and Conservatives in the dying days of the campaign. They rely on PBO costing of individual proposals (here).

Cumulative projected deficits over the next four years have gone from $131B in the Fall Economic Statement delivered in December, to $142B in the Parliamentary Budget Officer’s baseline projections in March before adding campaign pledges, to $225B under the Liberals’ plans and $100.6B under the Conservatives’ projections.

They're all made-up numbers and promises to be frank. For one, each plan is based upon sketchy macroeconomic assumptions that are dated because they pre-date the dramatic escalation of US measures on ‘Liberation Day’ and thereafter. There is so much uncertainty toward the outlook that we need to be very careful not to attach too much significance to the numbers beyond the general signal.

I wrote about the Libs’ plans yesterday (here). As for the Conservatives, I generally agree with sentiment expressed by many (such as here) that they have overreached on the revenues and multiplier effects they are booking. Unfortunately, articles like that failed to also mention the likely overreach in the Liberals’ numbers such as vague efficiency savings, and probably grossly underestimating infrastructure costs and project lengths as argued in my note yesterday. Unfortunately, efforts to adjust the Conservatives’ numbers for assumed misdeeds are not accompanied by analysts’ efforts to adjust the Liberals’ numbers for aggressive assumptions that understate their projected deficits. That’s unfortunate.

In any event, the Conservatives are making pretty aggressive assumptions on revenue multipliers derived from policies like ending the EV mandate, axing the carbon tax in full, scrapping emissions caps, cutting red tape and reducing regs, and going after criminal tax evasion and tax havens. For that, they must be held accountable.

Even at that, however, the deficits and debt issuance from the Conservatives' plans would still be considerably smaller. If we negate all of the debatable revenue lines—which is going too far—then the Conservatives’ plan would still retain about half of the narrower $124B cumulative projected deficits relative to the Libs’ plan. In reality, their cumulative deficits are somewhere well under half of the difference to the Liberals’ plans and potentially much lower if the Libs’ greater emphasis upon infrastructure spending is being lowballed as per the historical tendency for large scale project costs.

So what? Maybe the Liberals are correct in assuming this is the worst crisis of our lifetimes (again, but I’m counting three in a decade and a half which is multiple lives!) but I find the Conservatives’ numbers to be more prudent in light of the uncertainty, warts and all. A more measured fiscal plan leaves open greater policy optionality relative to going too far with expensive, long-tailed commitments that put at greater risk the Bank of Canada’s policy rate and overall borrowing costs. If this really is a permanent crisis with no off-ramp, then policy optionality can ramp things up. If it’s not, then at least another fiscal policy overshoot won’t have to be sterilized by monetary policy and market responses.

So overall, neither of the two main parties’ numbers are terribly credible and there are pluses and minuses to both platforms, but I'm personally more nervous about overdoing fiscal stimulus yet again by assuming a permanent crisis with no fiscal optionality along the way.

One thing I don't like about the Conservatives' plans is the requirement to hold a referendum before ever raising taxes while they are in power. Referendums are a dangerous tool not to be used lightly; ask the UK or think of Quebec. The answer you'd get is pretty obvious. If it's a tax hike on the relatively well off, Canadians would probably vote for it given the electorate’s average tendencies, but not if it's on the middle class and lower income earners. A referendum is a dangerous, populous cop out in many contexts and reduces what could be important flexibility.

Also check out Rebekah Young’s opinions on the two platforms here that was published last night.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.