ON DECK FOR TUESDAY, APRIL 22

KEY POINTS:

- Markets are relatively calmer

- Light US, Canadian data and Fed-speak on tap

- Why Canada’s Liberal platform sounds like it’s 2020 all over again

- Two reasons why Trump has been attacking the Fed

- Global Week Ahead — Promises, Promises! (here)

This morning’s relative calm is somewhat welcome after yesterday’s drubbing. Fresh catalysts are unclear. S&P and TSX futures are ¾% to 1% higher which would still leave the S&P down 15% since Trump escalated trade wars and markets finally clued into what he stood for beginning in later February. European cash markets are underperforming with a mixture of flatness to declines of -½% to -1% small losses as they catch up to developments after being closed yesterday. Sovereign yields are slightly lower across most European benchmarks as they catch up, while the US front end is reversing some of yesterday’s rally. The dollar is mixed this morning, but still weaker since last Thursday’s pre-holiday close.

LIGHT DEVELOPMENTS

There were no material overnight releases or developments. Light data is due out of the US and Canada along with several Fed speakers. Canada updates producer prices for March that might show some tariff and currency effects (8:30amET). The US updates the Richmond Fed’s manufacturing index for April (10amET). The Fed’s Jefferson (9amET), Kashkari (1:40pmET), Barkin (2:30pmET) and Kugler (6pmET) all weigh in.

CANADA’S CONSERVATIVES TO LAY OUT THEIR PLAN

Canada’s Conservatives will finally release their costed platform today, one day after advance polls shut (and when I voted) and with less than a week before election day. The time isn’t clear, but the itinerary shows an event at 6pmET for what that’s worth.

TWO REASONS FOR TRUMP’S ATTACKS ON THE FED

As for Trump’s attacks on the Fed and Chair Powell, there are two reasons that are not getting enough attention. First, it’s a classic Trump-style diversionary tactic. Trump’s tariff plans blew up in the administration’s face, and his fiscal plans are on ice. This is a well-worn playbook; divert attention from areas of sharp criticism by launching attacks on something else. Second, Chair Powell goaded Trump into attacking him with comments Powell gave last Thursday. I think that may have been intentional in order to make clear to the Supreme Court what was at stake in Trump v. Wilcox if the Court doesn’t at least carve out the Fed if it grants approval for the President to fire agency heads. Trump fell for it.

WHY THE LIBERALS’ PLATFORM SOUNDS LIKE 2020 REDUX

The Liberals’ platform has several attractive features that are largely consistent with what has been pre-advertised, but key is its reliance upon the assumption of a permanent crisis in order to justify very high spending and years and years of bigger deficits while its other assumptions contradict this perspective.

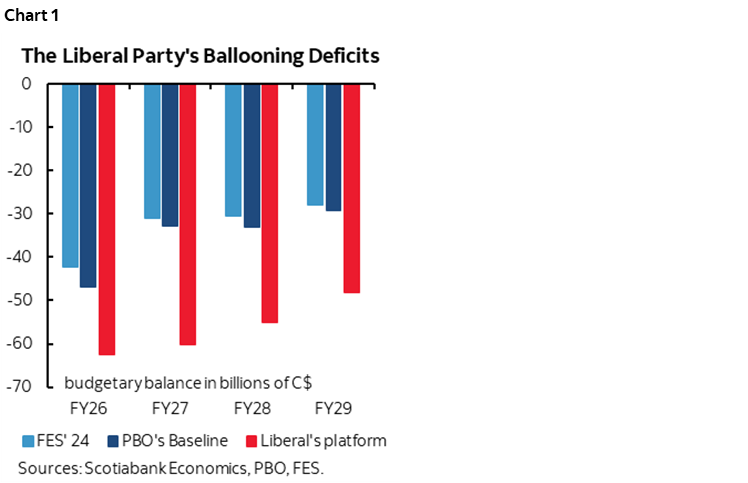

Chart 1 shows the rapid explosion of deficits over a very short period of time starting with the Fall Economic Statement’s projections that were delivered on December 16th, then the PBO’s baseline projections for the deficit before incorporating party platforms as delivered on March 24th, and then the Liberals’ platform projections that were shared on Sunday.

Those deficits are understated in the first couple of years because they are costed using stale PBO macro assumptions from March 5th before everyone started to downgrade forecasts particularly for next year’s growth. Further, if not for estimated tariff revenues, the federal government’s deficit this year would be well over $80 billion which is getting into the ballpark of what I warned about early this year. I wouldn’t be the least bit surprised to see that figure turn out to be higher yet.

The deficits may be understated even beyond the nearer term if the assumption of a sustained crisis comes to fruition because the PBO’s GDP forecasts assume steady growth throughout the next several years; nominal GDP growth is projected to be in the 3–4% range throughout the projection period which would mean relatively buoyant revenues throughout.

A US-motivated crisis is indeed upon Canada and that naturally tends to play to the Liberals’ polling advantage. Division within the Conservatives hasn’t helped that party. Taking far too long to establish key policy views beyond axe-the-tax and opposition to Trudeau also hindered the Conservatives’ polling.

But if Canada is to embark upon the path laid out in the Liberal Party’s platform, then we need to fundamentally ask whether it is prudent to assume that crisis will be a permanent fact of life throughout the four-year term of a new Canadian government. Will trade wars and a shrivelling US economy persist over the next four years? Maybe that’s what happens, or maybe Trump backs off into midterms which would be a replay of his 2018 moves. If he doesn’t deescalate before, then the damage to the US economy, labour market and inflation could result in GOP senators and representatives getting a thorough thrashing one year from November.

An alternative approach would be to include policy optionality given that it’s highly unclear how long a trade war will persist. The BoC uses scenarios and throws its hands up by declaring it doesn’t know what will happen. Frankly, we have little confidence in our own projections given the enormous uncertainty. Yet the Liberals’ strategists and the same overall composition of the federal party assume that a crisis will persist for many years despite using underlying projections that don’t really show a true crisis. To show a crisis, use forecast assumptions that show shrinking real GDP, or at least very minimal nominal GDP growth. Not the PBO’s.

The second assumption behind the platform is that only government can fix a crisis. Therefore, the two key assumptions being made in the Liberals’ plan are a perma-crisis and that only government can fix it.

In that sense, the Liberals’ plan sounds awfully like 2020 all over again to me. The error of applying too much stimulus for too long on the assumption that better days would never return was ultimately one factor that cost Canadians in terms of inflation and borrowing costs. When better days returned, everyone but Ottawa and the governments across provincial capitals pivoted. Persistent fiscal easing aggravated other drivers of inflation from the supply side and the rapid recovery of the demand side.

As a consequence, markets began tightening financial conditions through rising bond yields in anticipation of tighter monetary policy. Then the BoC began hiking aggressively once they eventually caught on to what was happening.

If that’s the path we’re on again, then the curve is too richly priced in Canada. Fiscal easing swaps out for monetary easing and market pricing for two more rate cuts this year and a below-neutral policy rate for years to come could have the market doing the same mistake all over again. Tariff pass through will be modest in Canada, supply chains face upheaval at least in the nearer term of the years of fiscal projections and then permanent fiscal easing negates much of any need for monetary easing and may pivot us back toward tightening all over again. Toss in the bond issuance required to make this plan sing and the combination of inflation risk and risk to Canada’s term premia make the whole curve look like it may be rather richly priced.

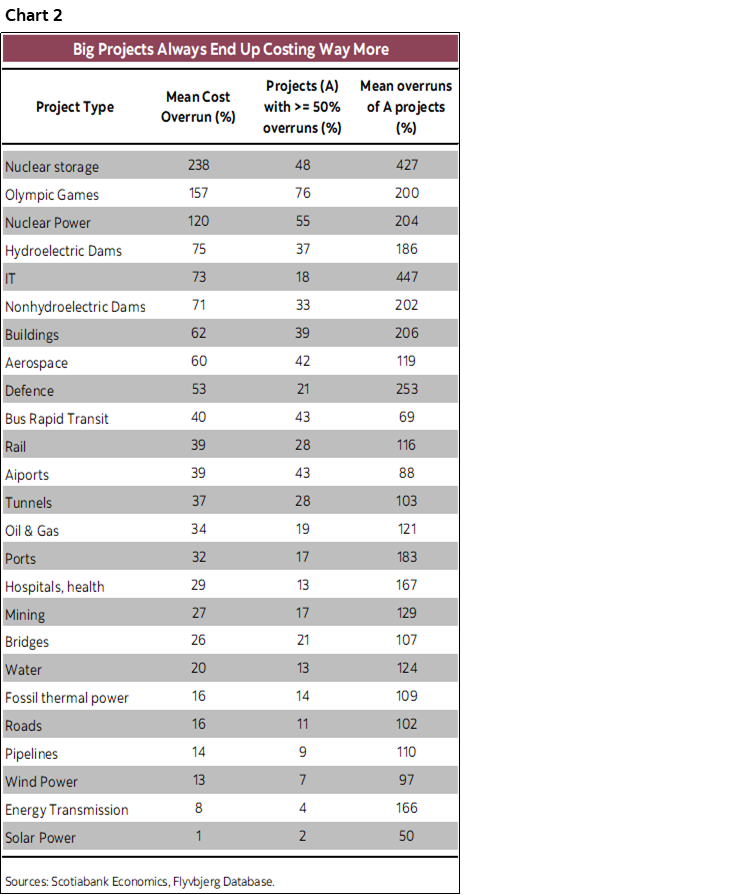

One possible offset to this narrative may be the greater emphasis within the Liberals’ platform upon investment and hence the supply side, versus the Trudeau administration’s emphasis upon social program spending and transfers. There are two caveats to this argument. First, the program spending is still being maintained with operating spending planned at a 2% annual growth rate. Second is the assumption that all investment is good for the supply side by way of unleashing more potential GDP growth and greater productivity. That’s unclear to me based upon the types of investment contained within the plan. Further, project cost overruns are the norm (chart 2) and with that go potentially much bigger deficits than projected. The history of these projects is that they tend to take much longer to develop than advertised and cost an awful lot more. The outgoing Liberal government tended to take delayed expenditures and turn them into social program spending which could also inflame deficits if that pattern persists.

To be sure, election platforms are full of promises that often don’t get realized, or when they do, are realized in a vastly different shape, form and timing. Nevertheless, assumptions across platforms, forecast inputs and financial market positioning should at least line up. I’m not sure they do.

It will take some time to evaluate the composition of risks to US policy, and how Canadian policy actually evolves, but at this juncture the market assumption that BoC easing and possible federal fiscal policy will join hands once again may be more vulnerable than it was the last time.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.