ON DECK FOR THURSDAY, APRIL 17

KEY POINTS:

- Markets await the ECB

- ECB to cut, sound guarded on the bias

- Trump’s attack on Chair Powell makes clear his intent…

- …which should influence the Supreme Court’s pending Trump v. Wilcox decision…

- …as granting power to fire the Fed Chair could prompt a financial market crisis

- The first of Canada’s election debates was a yawner

- Aussie jobs rebound, markets didn’t care

- NZ inflation surprises higher, NZ 2s cheapen

- Yen slips as US-Japan trade talks didn’t raise revaluation

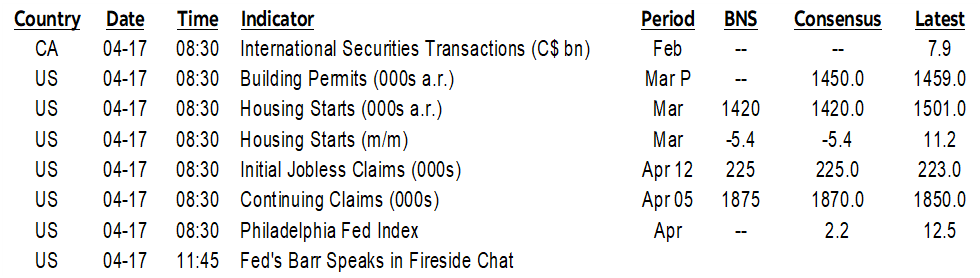

- Light US data on tap

- Early bond market closes in Canada and US

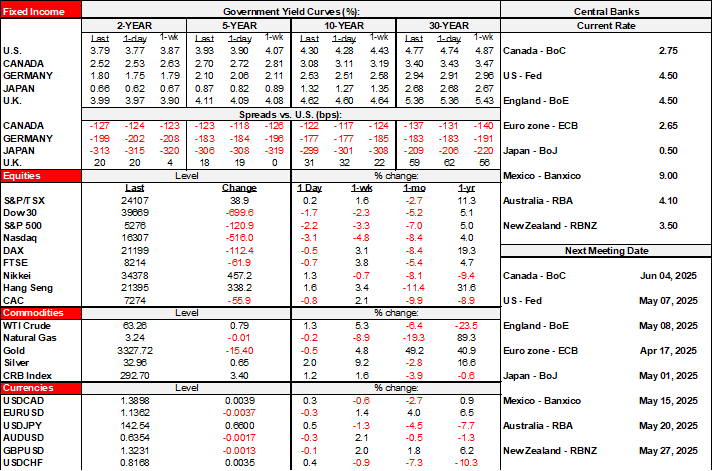

Stocks are mixed heading into the long weekend and early bond close (1pmET Canada, 2pmET US). US equity futures are up by nearly ½% to 1% while European cash benchmarks are down by +/-½% as they catch up to yesterday afternoon’s US sell off and its drivers such as Powell’s incrementally hawkish talk. Sovereign yields are gently higher across benchmarks in the US and Europe. The dollar is mildly stronger except against the Scandies and with sterling holding its own. There were light overnight developments ahead of the ECB as the day’s key calendar-based risk.

The yen is leading decliners to the dollar allegedly because US-Japan trade talks didn’t mention the yen and that has markets thinking the US isn’t pushing for it to be strengthened. I found the Japanese trade negotiator to be much more careful with his guidance on the prospects for a trade deal with the US than the US administration that sounds desperate for somebody to call them out on a date.

TRUMP’S ATTACK ON POWELL MAKES INTENTIONS CLEAR IN SUPREME COURT CASE

Trump’s remark this morning that Federal Reserve Chair “Powell’s termination cannot come fast enough!” puts added pressure on the Supreme Court to make clear in its pending ruling on Trump v. Wilcox that the Federal Reserve is exempt from Trump’s quest to have the authority to fire agency heads including the Fed Chair without cause and to therefore preserve the Fed’s independence. To so politicize the Fed would be strong cause for selling US assets and could engineer a financial crisis.

HUM DRUM CANADIAN ELECTION DEBATE

The first of two Canadian leaders debates was held in French last night. We learned nothing new by way of their policy stances. Carney pledged to release the Liberals’ fully costed platform this weekend and Poilievre said their platform would be arriving in coming days but didn’t mention costing. Watch for polls in the aftermath, mainly in Quebec. I didn’t think any of them really made much progress, but we’ll see. The highlight to me was watching Singh lose his cool at the moderator. I’ll focus on their platforms and next steps in my weekly later today.

AUSSIE JOBS REBOUND, MARKETS SHAKE IT OFF

Australia’s job market rebounded but there was minimal and short-lived reaction by the A$ and Australian rates largely because it was expected and bigger issues are ahead. 32k jobs were created in March of which 15k were full time and 17k were part time. The participation rate ticked up to 66.8% and the unemployment rate increased a tick to 4.1% due to a downward revision to the prior month’s reading.

NZ CPI WAS WARMER THAN EXPECTED

NZ CPI was a toucher warmer than expected and that drove the two-year NZ yield up by about 4bps post-release. CPI was up 0.9% q/q SA nonannualized. Tradeable CPI that is more influenced by external conditions was up 0.8% and non tradeable CPI was up 1.1% and more of a reflection of domestically generated pressures. Details were mixed, with price increases led by food, followed by transportation, housing and utilities, but with little pressure from clothing and footwear, healthcare and recreation/culture categories.

ECB TO CUT

The ECB is expected to cut by 25bps to a deposit rate of 2.25% and may be guarded on the bias (8:15amET). The policy rate is mildly restrictive into trade wars that overshadow lagging plans to ramp up defence and infrastructure spending. Still, much like the tone we heard from the BoC yesterday, I wouldn’t expect Lagarde to display much of any conviction on the path forward in her press conference (8:45amET) since, well, that depends upon having confidence in the US administration’s stability.

LIGHT US DATA ON TAP

Light US data includes weekly claims and starts, both at 8:30amET.

We also released our monthly forecast update last evening. On the markets side of things, staff and clients can direct questions on the BoC, Fed, US and Canadian yield curves to me. For FX exchange rates, it’s Shaun Osborne who champions them.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.