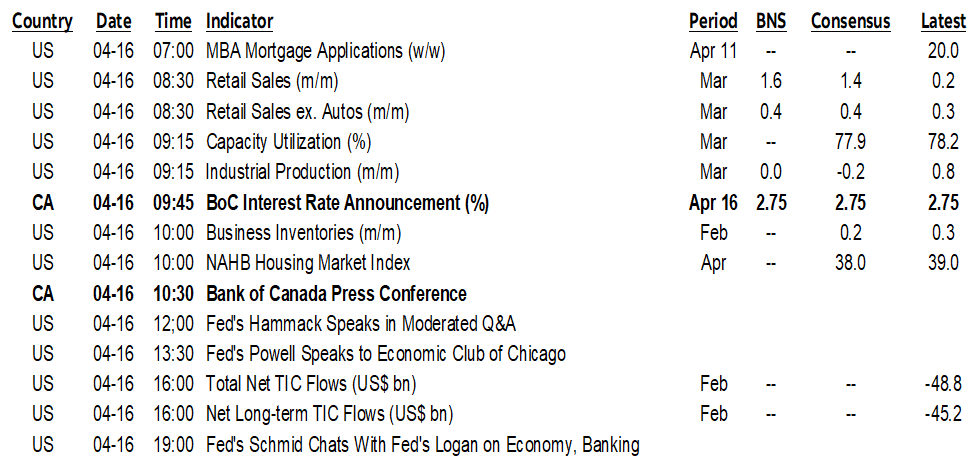

ON DECK FOR WEDNESDAY, APRIL 16

KEY POINTS:

- Risk off sentiment has several drivers all centered upon misguided US tariffs

- EU guides that a long trade war is likely

- US announces chip restrictions on Nvidia in China

- US takes a truly odd step toward critical minerals tariffs

- US commences pharma investigation to pave way for tariffs

- A glimmer of hope? California sues US administration over tariffs

- BoC day expectations—will a history of surprises repeat?

- Canadian tariff remediation won’t affect the BoC’s stance

- Powell’s latest outlook has probably changed very little in a short time

- US retail sales: will tariff front-running spill into core?

- The first of Canada’s election debates is tonight; or watch the Habs

- China’s GDP disappointed, and momentum into Q2 will fade

- Soft UK core CPI was shaken off by sterling, gilts

Risk off sentiment is dragging equities mildly lower across global benchmarks. US equity futures are down between ¾% for the S&P and 1½% for the Nasdaq, while European cash markets are off by around ½%. Sovereign bonds are benefiting with yields down a bit across the US front-end as well as the gilts and EGB curves. The dollar is feeling no love as all majors are up against it.

As for the catalysts, there are plenty. One is that the EU guided yesterday afternoon that it expected a long trade war based on little progress in talks with the US which should surprise no one. My narrative remains focused upon European dysfunction as the vast differences across the EU will restrain their ability to either retaliate or negotiate.

The drop in S&P futures had been larger before headlines hit that China is open to trade talks but subject to a list of what are likely to be rather difficult demands to meet. One caution is that this is “according to a person familiar with the Chinese government’s thinking” and so take it with a lot of salt. Second is that the person that could be anyone from a senior official to Xi Jinping’s driver signalled that China wants respect from the US administration, consistent communications from US cabinet members by reining in pointed insults (looking at you Navarro…), and to address concerns on Taiwan and sanctions. Good luck!

Another factor weighing on sentiment is that late yesterday, the US imposed China restrictions on H20 chips from Nvidia which is hitting their shares.

Also late yesterday was the announcement that the US is starting a Section 232 critical minerals probe that possibly paves the way for tariffs. This is rather odd given US reliance upon critical minerals from abroad (here) and how there is very limited potential to ‘bring home’ such production.

If that’s not enough, then recall that on Monday, the US also commenced a national security study into pharma supply chains that may set up tariffs on drugs. I’m sorry, but how dumb is that. The US already faces the highest drug prices basically anywhere. Tariffs on imports will drive those prices higher. More people—who already face big gaps in access to and affordability of health care—will die of cancer and other ailments.

The state of California announced this morning that it is suing the Trump administration by contesting its ability to impose tariffs. This could be interesting in that it has long been thought that someone would step forward to challenge the abuse of past pieces of US legislation that Trump has used to declare national emergencies as justification for tariffs. And California has deep enough pockets to see it through in a legal system in which money definitely talks! There are four legal challenges underway now including others such as the Koch family’s challenge.

Overnight data didn’t really matter. The main focus into the N.A. session will be the BoC, plus it’s doubtful that Powell will have much to say that is new about the outlook this afternoon after US retail sales.

BANK OF CANADA—HOLD OR CUT?

Then it’s the BoC’s show from 9:45amET through to about 11:30amET. The statement lands at 9:45amET along with the MPR that includes forecast ranges and scenarios this time plus Governor Macklem’s opening remarks to his press conference that itself begins at 10:30amET. There may also be a technical paper that updates staff estimates of the neutral rate range that to now has been 2.25–3.25%.

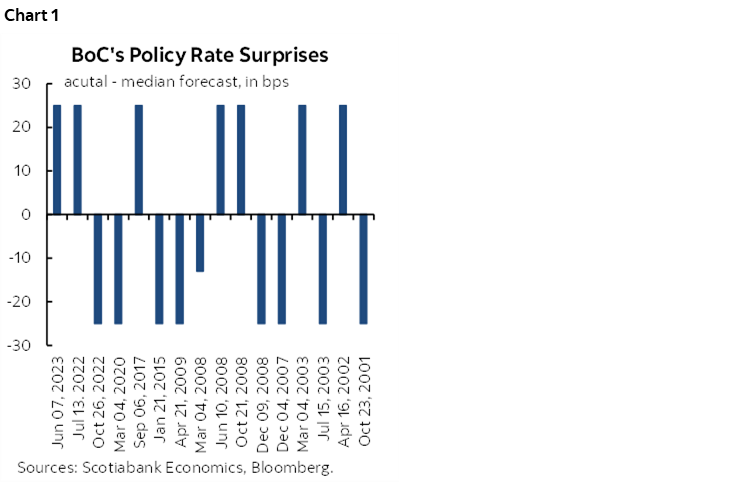

A hold is fairly widely expected but it’s a close call and this central bank loves a good surprise every now and then. Chart 1 shows a sampling of times when they have surprised. They’ve ended QT and controlled CORRA so there should be nothing to see other than the policy rate, likely a careful bias, and forecast ranges plus a probable re-estimation of the neutral policy rate. See my weekly (here) for comparisons of the hold and cut cases that I won’t repeat here.

TARIFF REMEDIATION WON’T AFFECT THE BOC

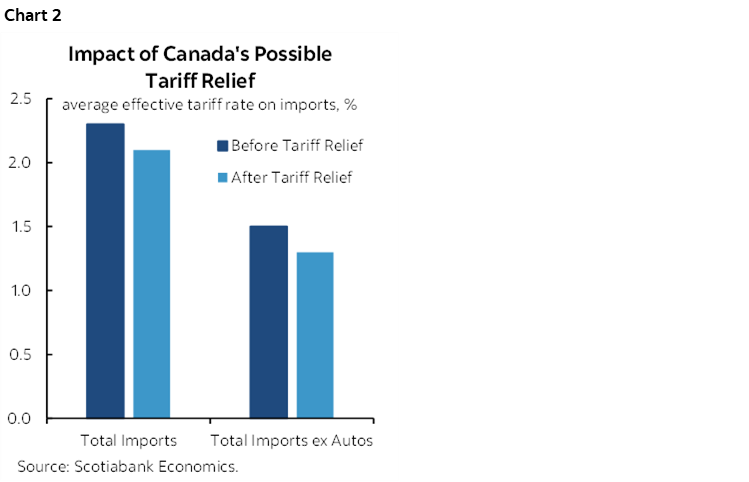

As for yesterday’s new tariff relief announcements from Canada (here)? The timing—coming a day before the BoC—raised some eyebrows with some clients, but they won’t matter to the BoC based on our rough guesstimates that the impact on Canada’s average effective tariff rate would be a rounding error plus uncertain future effects on Canadian tariffs on imported US vehicles. Chart 2 shows John McNally’s calcs for the effective tariff rate on Canadian exports and Canadian imports both before and after yesterday’s announcements. Particularly hard to estimate, however, is the effect of the autos announcement since we need to monitor pledges from auto companies to keep production in Canada as a condition for tariff relief.

The Government of Canada is expected to offer more details on yesterday’s tariff announcements at 2pmET today.

POWELL TO UPDATE HIS OUTLOOK BEFORE COMMUNICATIONS BLACKOUT

And then Powell gets the last and perhaps most impactful word when he speaks on the economic outlook in Chicago (1:30pmET). Maybe he’s got something to say before the communications blackout two Saturdays from now. I doubt his message will change from the April 4th outlook and I highly doubt he’ll echo Waller’s talk yesterday.

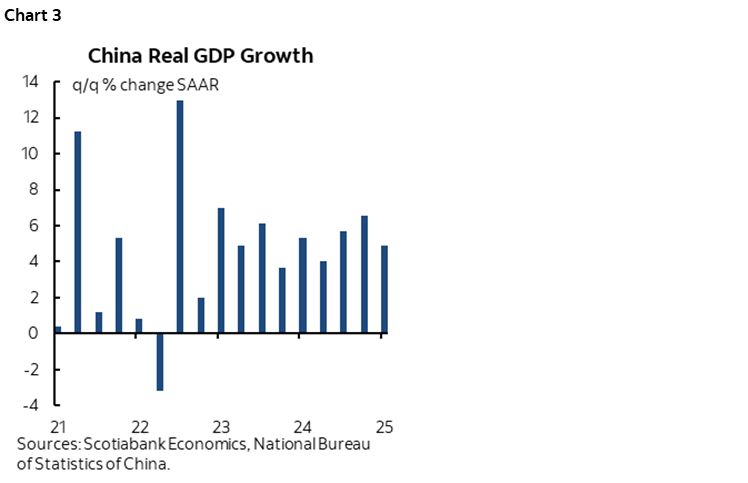

CHINA’S ECONOMY—Q1 DISAPPOINTS, SIGNALS MOMENTUM INTO Q2 THAT WILL FADE

A blast of macro releases out of China started the fun last evening. All of the releases were stale given downside risks ahead.

Q1 GDP grew by 1.2% q/q SA (1.4% consensus) which is the slowest in three quarters (chart 3). The quarter ended on an upbeat note in terms of higher frequency data, perhaps on tariff front-running effects. Retail sales were up 5.9% y/y (4.3% consensus) and industrial output grew by 7.7% y/y (5.9% consensus). Those readings will offer a favourable jumping off point for Q2 growth, but it’s likely all downside from there.

Chinese home prices continue to decline with new homes down -0.1% m/m and resales down -0.2%. Both have been falling each month throughout the past two years, but the pace of decline was ebbing before trade wars (chart 4).

UK INFLATION—CORE MATCHED EXPECTATIONS, MARKETS SHAKE IT OFF

UK CPI then took the baton with CPI figures for March that had little effect on UK markets. Key is that at 0.5% m/m, core CPI in m/m NSA terms matched the average compared to like months of March in history (chart 5). That dragged the y/y core CPI reading down a tick as expected to 3.4%. Headline CPI was up 0.3% m/m (0.4% consensus). Services CPI was softer than expected at 4.7% y/y (4.8% consensus, 5% prior).

US RETAIL SALES ON TAP—WAS TARIFF FRONT-RUNNING ABOUT MORE THAN JUST AUTOS?

US retail sales for March (8:30amET) are expected to be strong in terms of the autos contribution that most think could drive a gain of over 1% m/m, but key will be ex-autos as potential further evidence of any tariff front-running versus confidence effects. The US also updates industrial output that is expected to be soft for the month of March (9:15amET)

THE FIRST CANADIAN ELECTION DEBATE

Last, how Canadian is this. The first of the leaders debates was brought forward to 6pmET tonight in Montreal in French because they didn’t want it to conflict with Montreal’s final regular season game that will determine whether they get a wildcard spot in the playoffs. Love it! The English debate is tomorrow night.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.