ON DECK FOR WEDNESDAY, NOVEMBER 20

KEY POINTS:

- USD broadly strengthening on light developments

- Eurozone negotiated wages rise by most since 1993…

- ...but narrowly—and maybe temporarily—driven by Germany

- UK core CPI accelerates, trimming BoE rate cut pricing ahead of BoE-speak

- Inflation undershoots on eve of SARB’s decision

- BI holds with an ongoing eye on the rupiah

- Fed– and ECB-speak on tap, US & Canada auctions

- Nvidia releases in the after-market

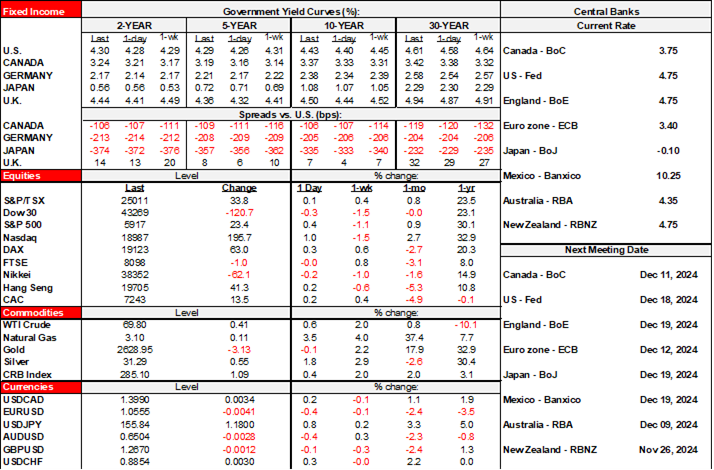

There is little movement across global asset classes other than currencies where the dollar is broadly stronger this morning. European curves are slightly cheaper following strong Eurozone wage gains and UK core CPI. South Africa’s curve is outperforming post-CPI and Indonesia’s curve is underperforming after BI held. Stocks are slightly higher across N.A. futures and European cash markets. There is only Fed– and ECB-speak on tap into the N.A. session as well auctions of Canada 10s and US 20s, plus Nvidia releases quarterly earnings after the close today.

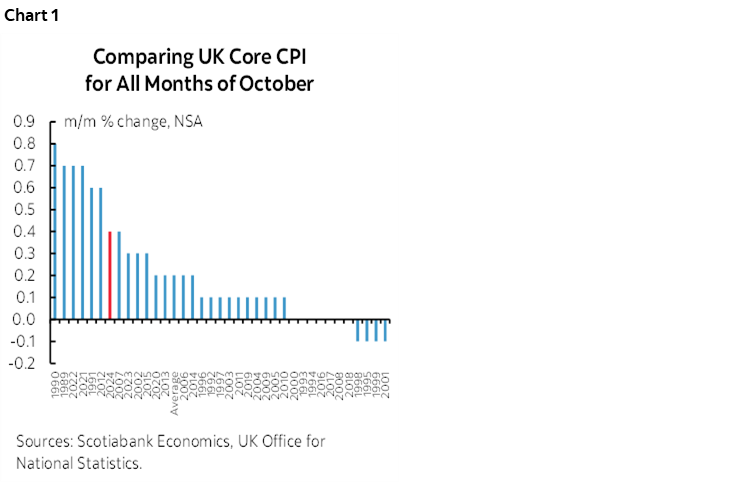

UK Core CPI Trims BoE Rate Cut Pricing

UK core CPI was up by more than expected for the month of October. The reading landed at 0.4% m/m NSA which was double the average for like months of October in history (chart 1). That drove the y/y core inflation rate up a tick to 3.3% (3.1% consensus). Headline inflation was up by 0.6% m/m (0.5% consensus) as Ofgem raised the regulated energy price cap by about 10%. It’s the core acceleration that is driving markets especially after the glimmer of hope the prior month when core CPI was among the weakest months of September on record. BoE’s Ramsden speaks later today (11amET).

As a result, while December was already priced for no action by the BoE before the data, February’s pricing was shaved by a few points to under 20bps of a quarter point cut.

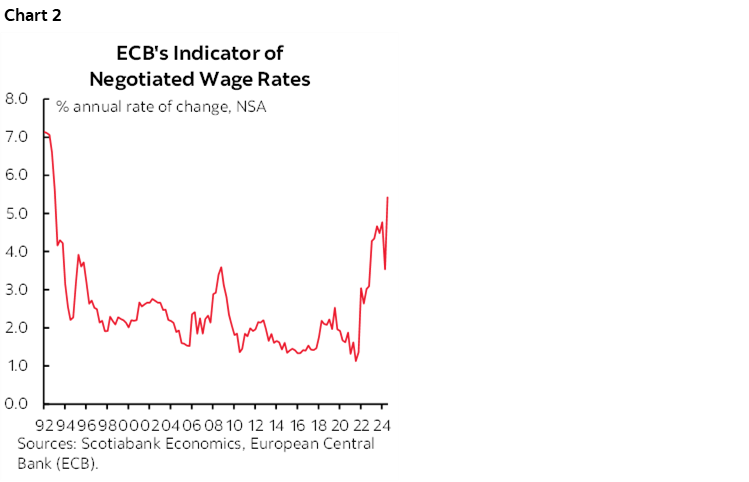

Spike in Eurozone Negotiated Wage Gains Shaken Off

The ECB’s negotiated wages indicator for 2024Q3 accelerated sharply to 5.4% y/y (chart 2). That follows a brief deceleration the prior quarter and takes negotiated wage growth up by the fastest pace since 1993Q1. The biggest driver was Germany where negotiated wages were up by 8.8% y/y as we learned yesterday morning. The concentration of the gain on Germany that was already known and guidance from the Bundesbank that it is unlikely to persist led to little reaction in ECB pricing. Markets are priced for more than a full quarter point cut on December 12th.

We’ll see what ECB officials think about the figures when Guindos (1pmET), Stournaras (1:30pmET) and Makhlouf (2pmET) speak.

Inflation Undershoots on Eve of SARB’s Decision

South African inflation weakened on the eve of SARB’s expected rate cut tomorrow. Headline CPI fell -0.1% m/m (+0.1% consensus) and the y/y rate dropped a full percentage point to 2.8% (3% consensus). Core inflation was up 0.2% on consensus and decelerated by two-tenths to 3.9% y/y, also on consensus. SARB is expected to cut by 25bps tomorrow as the whole yield curve shifted lower by 6–9bps post-data.

BI Holds in Defence of the Rupiah

Bank Indonesia left its policy rate unchanged at 6% as most had expected and retained a focus upon rupiah stability.

Nothing Material Out of N.A.

Fed officials will natter on with Barr (10amET), Cook (11amET), Bowman (12:15pmET) and Collins (4pmET) on tap but it’s hard to imagine what they may say that’s new. Canada auctions 10s at noon ET today and the US auctions 20s at 1pmET.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.