| ON DECK FOR WEDNESDAY, MAY 8 |

KEY POINTS:

- Bond markets playing defence as central banks diverge

- BoJ’s Ueda ups his warning on the yen

- Fed’s nonvoting Kashkari plays up no move in 2024…

- ...which isn’t likely to be the Committee’s median projection in June

- Sweden’s Riksbank delivers a partially expected cut…

- …and unchanged forward guidance for mild easing

- Brazil’s central bank might downshift its pace of easing

- PSA: Canada to test alert system today

Central banks are stirring with comments and actions that are raising divergent stances. A relatively hawkish sounding BoJ Governor upped his warnings overnight. Fed speakers are stirring the pot in the tails of FOMC opinions. Sweden’s Riksbank delivered a partially expected cut and unchanged forward guidance. Brazil might downshift the pace of easing later today.

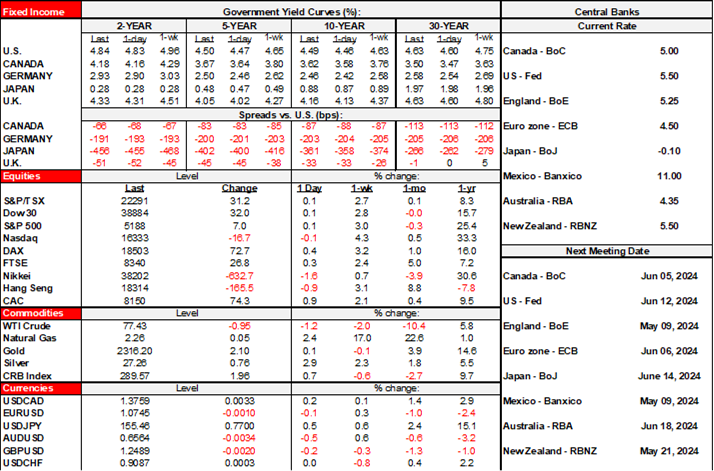

The net outcome of all of this has bonds playing a little defence this morning with a slight cheapening bias across most benchmarks and markets particularly in Europe that is catching up to yesterday afternoon’s Fed comments that came after Europe went home. US and Canadian equity futures are flat and European cash markets are mostly higher. The USD is broadly stronger against most major crosses except for little change in the euro and related FX crosses.

BoJ’s Ueda Ups a Warning About Yen Weakness

BoJ Governor Ueda jawboned the currency a little more aggressively, but markets paid little attention. He said last evening that “Foreign exchange rates make a significant impact on the economy and inflation. Depending on those moves, a monetary policy response might be needed.” That could include a variety of tools with a hike among them. The yen appreciated by about ½% or so overnight. Market OIS pricing for the target rate wasn’t materially affected across any of this year’s meetings that already had about 20bps of more hikes priced in by year-end. Japan’s 2-year yield only edged 1bp higher overnight. A surprise hike at the next meeting in June could rattle through global bond markets.

FOMC’s Kashkari Stirs the Pot

Minneapolis Fed President Kashkari whacked the beehive and ran yesterday afternoon. He said that “The most likely scenario is we sit here for an extended period of time” and then spoke to two tailed risks of cutting if inflation edges down and the job market weakens, versus the risk “that we need to go higher.” The US 2-year yield has increased by about 3–4bps since he delivered those remarks and cumulative pricing for cuts this year edged 2–3bps lower to just under half a percentage point. Kashkari doesn’t vote until 2026 which may lessen the discipline that he might apply to his views. These are his personal views that could be reflected in his being an extension of one of the two dots that were expecting no cuts this year back in the March dot plot. I wouldn’t expect wiping out cuts this year to be the median FOMC projection and think it’s more likely the median gets reduced from 75bps to 50bps.

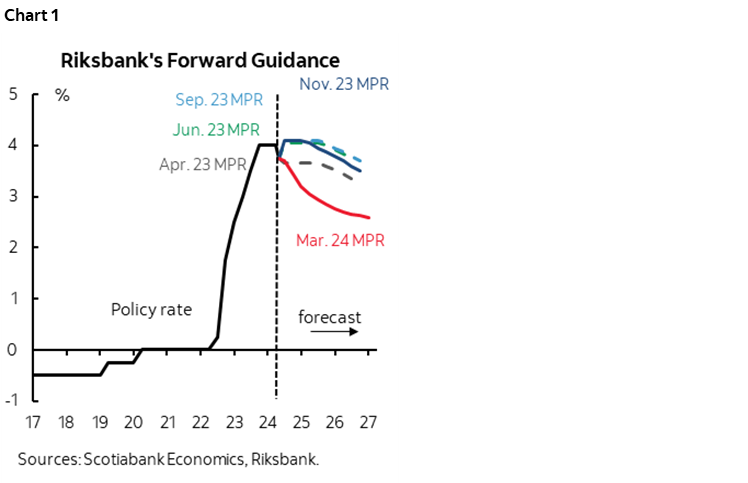

Sweden’s Riksbank Cuts, Delivers Unchanged Forward Guidance

Sweden’s Riksbank cut its policy rate by 25bps to 3.75%. The action was a partial surprise as it wasn’t fully priced and there was a significant minority within consensus that didn’t expect a cut at this meeting. The krona was the worst overnight performer to the USD among the majors and semi-majors. Sweden’s rates curve was nevertheless not really affected, given that the debate was centered on whether they would cut in May or June as opposed to not cutting at all. Forward guidance explicitly said that two more cuts are expected over 2024H2, largely ruling out a move in June and consistent with the rate path that they had published in March. Governor Thedeen advised that a June cut was unlikely and that “The adjustment of monetary policy going forward should therefore be characterized by caution, with gradual cuts to the policy rate.”

Brazil’s Central Bank Might Downshift the Pace

Brazil’s central bank is widely expected to continue easing later today (5:30pmET), but this time there is a more divided consensus on whether they will cut by 25bps or maintain the same 50bps pace at which they have been easing since they started in August. Currency volatility is one consideration in favour of less.

Little Else Going On

Recall that there is basically nothing interesting by way of US macro risk this week and in Canada it's all about Friday's jobs and wages.

Chile updates CPI for April shortly (8amET). It’s expected to tick higher to 3.8% y/y.

And as a PSA for colleagues and clients in Canada but outside of Ontario, just a heads up that your phones, TVs and other devices will be screaming today as they test the national alert system. Don’t worry, it’s not Comrade Freeland announcing a quadrupling of planned debt issuance to nationalize telecoms and grocers or anything crazier than hiking capital gains taxes. Nope, it’s just if you happen to be in a client meeting or call at that time. Ontario will test next Wednesday. Times are listed here.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.