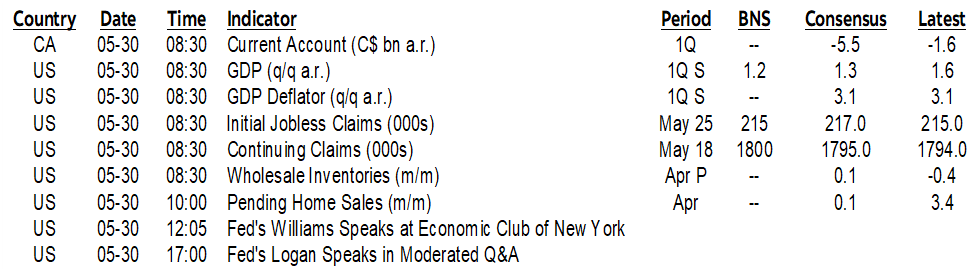

ON DECK FOR THURSDAY, MAY 30

KEY POINTS:

- Markets stabilize ahead of tomorrow’s big data and month-end effects

- US Q1 GDP may be revised lower, could undershoot Canadian growth

- Any US Q1 PCE revisions may influence hand-off influences on tomorrow’s April PCE

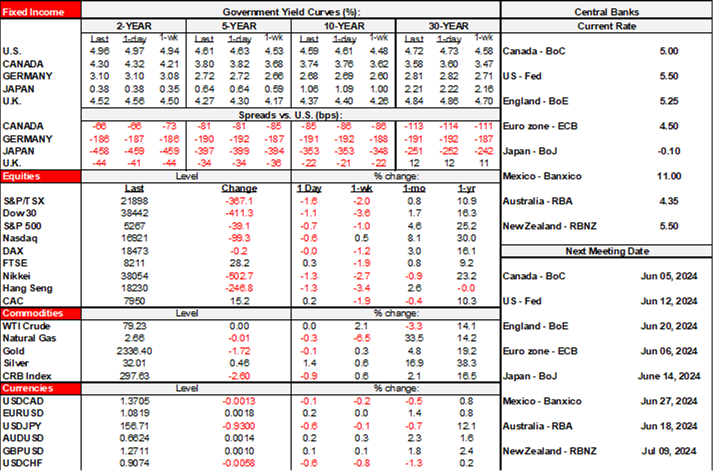

- US auctions are over for this week, Canada to auction 2s

- Easier financial conditions in Canada than the US should keep the BoC cautious

- Advance indicator points to still sticky Canadian inflation expectations

- Spanish core CPI was a touch warmer

- Fed’s Bostic open to Q4 cut

- Most Canadian banks beat expectations in Q2

- CHF appreciates on GDP beat

- Krona outperforms on GDP beat despite soft details

- Kiwi curve relieved that bigger Budget issuance was no worse than expected

- Rand depreciates as the ANC loses majority, SARB on tap

Markets are a touch more stable on balance this morning and in a bit of a holding pattern as US auctions are done for this week and markets await bigger developments when heavy data arrives into month-end. Sovereign yields are gently lower across most US and European benchmarks. S&P futures are down another ½%, TSX futures are flat and European cash markets are mostly a little higher. Idiosyncratic risks are driving divergent currency moves.

Today’s developments should be relatively light ahead of tomorrow’s potential macro fireworks when US core PCE for April, Canadian GDP for Q1, March and April, Eurozone CPI for April and China’s state PMIs get released.

US GDP, PCE Revisions on Tap

US GDP and PCE revisions for Q1 may be impactful (8:30amET). This will be the second swing at the US Q1 GDP estimate and data since the first estimate of 1.6% suggests a modest downward revision. It’s possible Canada posted stronger growth in Q1 than the US in a switch over and with Canada having momentum into Q2 based upon limited readings like hours, alt-data and some flash guidance on a few indicators.

No revisions are expected to the 3.7% q/q SAAR core PCE rise but are always possible and could affect expectations for Friday’s core PCE print for April by way of any changes to hand-off effects.

The US advance merchandise deficit in April (8:30amET), weekly jobless claims (8:30amET) and pending home sales in April (10amET) probably won’t have much effect on markets.

Canada to Auction 2s, Misguided Views on Relative US-Canadian Inflation Risk

Canada auctions C$5.5 billion of 2s today after light data (12pmET). The view that Canada faces less inflation risk than the US is already fully priced in everything and should not be further reinforced by premature easing, and I continue to disagree with it anyway. The BoC already sits 50bps below the Fed. The whole Canadian rates curve is beneath the US. The Fed is dealing with a strong currency, the BoC is dealing with a weak one. Canadian oil prices matter more to Canada’s economy than the US and Canada’s key oil prices (eg. WCS) have outperformed WTI. Overall, financial conditions are broadly easier in Canada than the US. Now, since it’s already fully priced across every measure of financial conditions, then the BoC shouldn’t feel compelled to add to this by front-running the Fed in a hurry to cut. The market effects of potentially moving next week wouldn’t stop with just a single quarter-point cut. Based on in-person meetings and calls with global clients that I’ve been having, there is a wave of buying of the Canada curve just waiting for the first cut to be delivered. Some of the feedback from clients has been nuanced, some has been explicit and it comes from a cross section of institutional clients from hedge funds, to global life cos and central banks. A June cut would trigger pricing for a July cut and a potential tsunami effect into the Canadian front-end.

Cutting next week would also be a further blow to the BoC’s maligned forward guidance tool. Macklem said in two rounds of parliamentary testimony that the decision on when to cut would be informed by “months” of evidence, not one month. Since it was only one month before the June 5th decision, the Governor would violate his own carefully chosen written words if he were to cut one month after saying this.

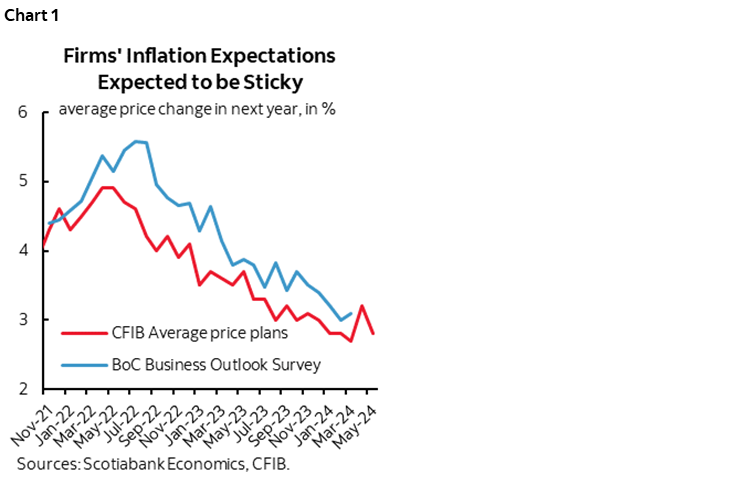

Sticky Canadian Inflation Expectations

The small business association in Canada publishes a measure of members' price plans over the coming year that is highly correlated with the BoC's business survey measure of inflation expectations that we won't get until July. This morning's update of that small biz gauge suggests that the BoC's measure will remain sticky and around the upper end of the BoC's 1–3% inflation target range (chart 1). That’s especially since the small biz measure tends to track a little below the BoC's measure that is more skewed toward larger companies.

Canada also updates payrolls at 8:30amET, but the long lag (it’s only March data) and the fact that by definition it excludes off-payroll jobs that are important in Canada mean that it does and should get little attention ahead of next Friday’s Labour Force Survey.

Canadian banks posted a pair of earnings beats this morning. RBC’s Q2 EPS was C$2.92 ($2.76 consensus) and CIBC’s was C$1.75 ($1.65 consensus). The more the merrier! So, BMO was the only clear miss, TD beat but faces other challenges, and each of BNS, RBC, CIBC and National beat.

Other Overnight Stuff

There were no major overnight developments, but here’s a run down of what unfolded.

- Atlanta Fed President Bostic (voting 2024) said last evening that “if things go according to what I expect” then a first cut could be delivered in Q4 and that “many” inflation measures are moving toward target. He’s probably among the relatively more hawkish members on the FOMC. We’ll also hear from the Fed’s Williams (12:05pmET) and Logan (5pmET).

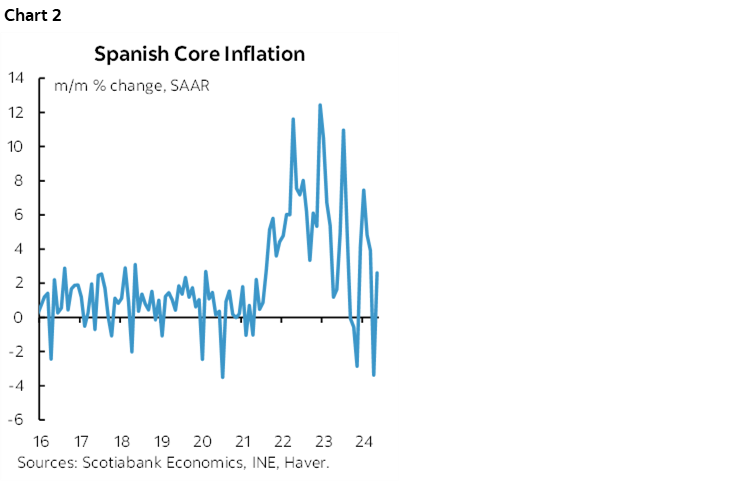

- Spanish CPI inflation was on the screws at 0.2% m/m NSA on an EU-harmonized basis during May. Core inflation was up by 3% y/y (2.9% prior) because it was up by 0.3% m/m NSA and by our calculations that translated into a 2.6% m/m SAAR rise which was a bounce back from the prior month’s decline (chart 2). France and Italy release tomorrow morning when the EZ tally arrives.

- New Zealand’s budget was no worse than expected and that was good enough to drive a mild rally in shorter-dated bonds and a slight depreciation in the kiwi dollar. Bigger deficits and higher issuance were in line with expectations as deficit-financed tax cuts aimed at lower- to middle-income households were delivered. The cuts were in line with what PM Luxon had put forward as the centerpiece of his electoral platform back in October.

- South Africa’s central bank is expected to hold again this morning (~10.30amET), but the ANC’s apparently lost majority in overnight election results is driving the rand to be the worst performer to the USD among the majors and semis.

- Switzerland’s economy outperformed expectations with GDP up 0.5% q/q SA nonannualized in Q1 (0.3% consensus). That drove the CHF to be the strongest outperformer to the USD this morning and reduced pricing for the June SNB meeting by 3–4bps to just -9bps.

- Sweden’s economy embarrassed consensus by posting 0.7% q/q SA nonannualized growth in Q1 (consensus 0%) with a mild upward revision to 0% from -0.1% for the prior quarter. Details don’t look great, however, as higher inventories and less of an import leakage effect played significant roles. Still, the krona is outperforming most other crosses this morning.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.